CAPITAL-CENTERED MODELS OF CORPORATE OWNERSHIP

Berle and Means (1932) argued in The Modem Corporation and Private Property that with the rise of the large, diffusely held corporation and the dispersion of ownership to thousands of smaller shareholders, the relationship between shareholders and corporate managers has changed and de jure control vested in ownership has given way to de facto control exercised by professional managers. Much of the work on corporate control since then has attempted to address the Berle and Means thesis. Two more recent approaches to the corporation, agency theory and transactions costs theory, focus on the role of the "market for corporate control" in bridging the gap between ownership and control. Through

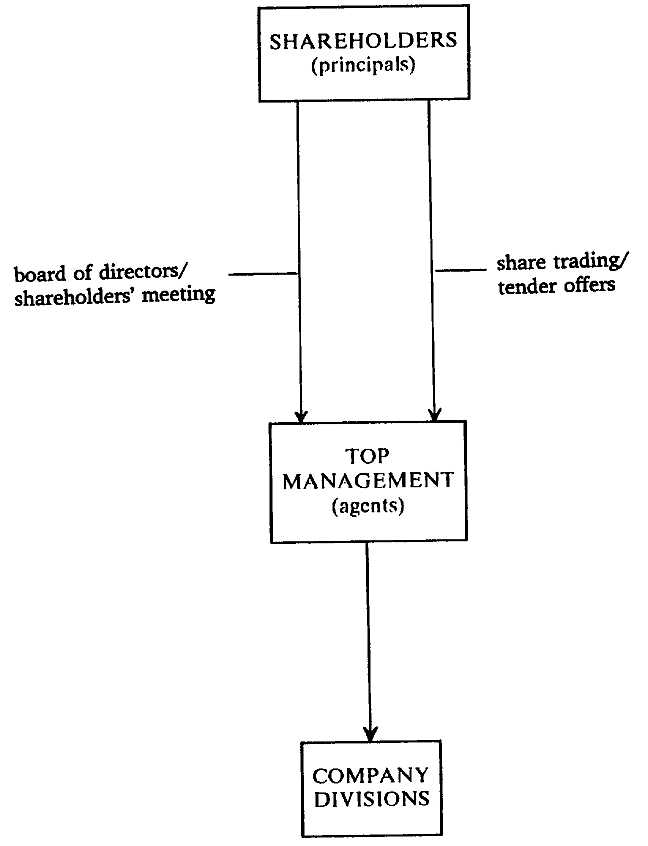

this market, the holders of capital in the capitalist economy-the shareholders of the firm-are granted the formal rights to control the corporation, and these rights are freely tradable in the stock market. Within both approaches, the joint stock corporation is conceived of as a system divided into shareholders, top managers, and internal operating units. Each of these positions is discrete but related through a linear chain of command defining the organizational hierarchy. This image is depicted in Figure 7.1.

The economic theory of agency (Jensen and Meckling, 1976; Fama and Jensen, 1983) focuses on the top half of Figure 7.1, wherein shareholders serve as "principals" who hire managers as their "agents" to actually run the business. Incumbent managers, agency theorists argue, are limited in their ability to exercise discretion at the expense of the organization because of the external discipline of the market for corporate control. Shareholders govern firms through the potential replacing of ineffective management by tender offer (Manne, 1965) or proxy contests. Competition is conceived of as taking place among different sets of managers, some within the firm and some outside. In the arena of the stock market, management teams compete for the right to control corporate resources.[2]

The transactions costs approach most closely associated with the work of Oliver Williamson shifts attention to the bottom half of Figure 7.1. Williamson emphasizes the abilities of internal organizational innovations to mitigate the control problems Berle and Means first identified. "In a general sense, the most severe limitation of the capital market is that it is an external control instrument. It has limited constitutional powers to conduct audits and has limited access to the firm's incentive and resource allocation machinery" (Williamson, 1975, p. 143). Foremost among these internal mechanisms is the multidivisional or M-form organizational structure: "The organization and operation of the large enterprise along the lines of the M-form favors goal pursuit and least-cost behavior more nearly associated with the neoclassical profit maximization hypothesis than does the U-form [functionally structured] organizational alternative" (Williamson, 1975, p. 150, italics deleted). The decomposition of firms into semi-autonomous profit centers, in this argument, introduces incentives within the firm's internal structure to generate division profit as a check on managerial discretion.

In capital-centered resolutions to the corporate control dilemma, then, agency theorists focus on discipline brought about through external market forces while transactions costs theorists emphasize discipline

Fig. 7.1. Capital-Centered Models of Corporate Governance: One-Way

Control Exercised by Independent Shareholders.

brought about through adaptations in internal organization. However, both views, along with Berle and Means', share an orientation toward corporate governance in which shareholders, managers, and firms are viewed as differentiated positions with control moving vertically downward along a linear pathway in which capital is the primary constituency of interest.