Chapter VII

The Japanese Firm in Context

In all of the attention that the Japanese firm has received in recent years, surprisingly little has been paid to the firm's institutional environment, and in particular to its joint development with intercorporate alliance structures.[1] As the previous chapter pointed out, extensive cooperation across firm boundaries has enabled the Japanese company to limit its size and scope while maintaining some of the advantages of the integrated firm in promoting technological development. In addition, these relationships have been a precondition for other characteristics of the Japanese firm, including the development of its internal organizational systems. Accolades for Japanese-style management and prescriptions for Western adoption of permanent employment and other internal practices must, for this reason, consider the essential context-dependence of these policies.

Perhaps the most systematic attempt to date to understand this interconnectedness is found in the work of Masahiko Aoki. In a variety of papers and books over the past decade, Aoki (1984c; 1987; 1988) has developed a "corporative managerialist" model of the Japanese firm based on the view that employees of Japanese firms are a constituency of equal importance as shareholders, with management acting as mediator between their interests in the policymaking process. This dual structure stands in marked contrast to the predominant shareholder-oriented focus of the American firm, in which management is presumed to serve the interests of owners passively, and has freed the Japanese firm from the institutional setup of classical capitalist control:

I argue that labor market imperfections (the establishment of the internal labor market) and the relative illiquidity of corporate shareholdings (because of the formation of corporate groups) are twin prerequisites for, as well as twin consequences of, the kind of management that has developed in Japan. The imperfect labor and capital markets reinforce and complement each other. [1987, p. 264.]

This chapter considers in more detail the relationship between the Japanese firm's environment and its internal organization. Although I concur with Aoki's assessment regarding the importance of capital market structure, I place much greater emphasis than he does on attempts by managers to reduce or eliminate the role of independent shareholders in the firm's governance structure. Where investors do influence management, I argue, it is largely a result of their simultaneous roles as bankers and trading partners. Equity investments are not unimportant, for they help to reinforce firms' business interests, but it is their business rather than capital-market function that is of primary concern.

Alliance structures have in turn transformed the respective positions of the firm's key constituencies-owners, managers and other employees, and trading partners-and therefore who controls the firm itself. The result is a form of corporate economy in which the mechanisms of corporate governance operate significantly differently from those in the United States, both in the market for corporate assets and in the institutions of shareholder representation. The chapter concludes with a case study of the transformation of corporate governance in a Japanese firm, showing these processes at work in the Mitsubishi group's buyout of foreign shares in Mitsubishi Oil.

CAPITAL-CENTERED MODELS OF CORPORATE OWNERSHIP

Berle and Means (1932) argued in The Modem Corporation and Private Property that with the rise of the large, diffusely held corporation and the dispersion of ownership to thousands of smaller shareholders, the relationship between shareholders and corporate managers has changed and de jure control vested in ownership has given way to de facto control exercised by professional managers. Much of the work on corporate control since then has attempted to address the Berle and Means thesis. Two more recent approaches to the corporation, agency theory and transactions costs theory, focus on the role of the "market for corporate control" in bridging the gap between ownership and control. Through

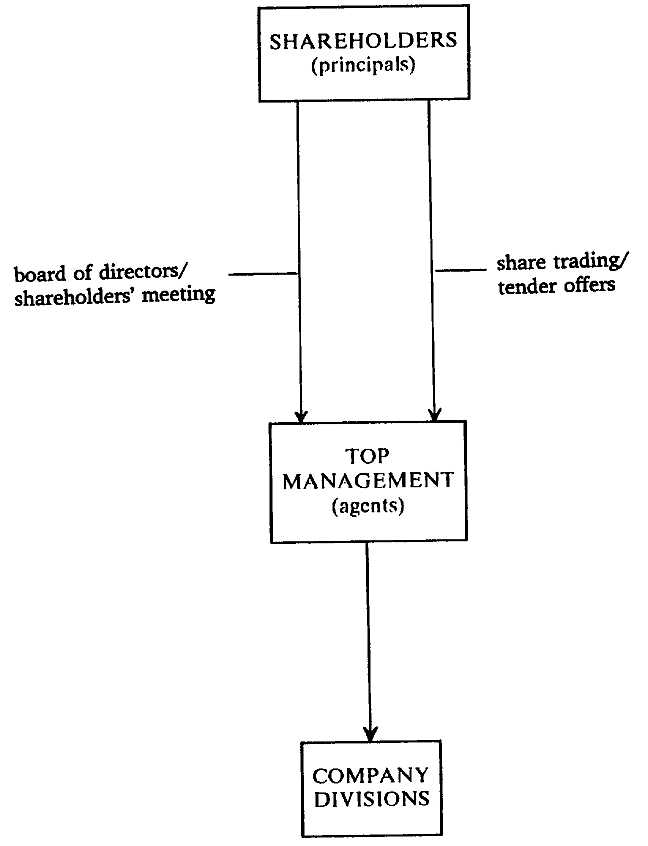

this market, the holders of capital in the capitalist economy-the shareholders of the firm-are granted the formal rights to control the corporation, and these rights are freely tradable in the stock market. Within both approaches, the joint stock corporation is conceived of as a system divided into shareholders, top managers, and internal operating units. Each of these positions is discrete but related through a linear chain of command defining the organizational hierarchy. This image is depicted in Figure 7.1.

The economic theory of agency (Jensen and Meckling, 1976; Fama and Jensen, 1983) focuses on the top half of Figure 7.1, wherein shareholders serve as "principals" who hire managers as their "agents" to actually run the business. Incumbent managers, agency theorists argue, are limited in their ability to exercise discretion at the expense of the organization because of the external discipline of the market for corporate control. Shareholders govern firms through the potential replacing of ineffective management by tender offer (Manne, 1965) or proxy contests. Competition is conceived of as taking place among different sets of managers, some within the firm and some outside. In the arena of the stock market, management teams compete for the right to control corporate resources.[2]

The transactions costs approach most closely associated with the work of Oliver Williamson shifts attention to the bottom half of Figure 7.1. Williamson emphasizes the abilities of internal organizational innovations to mitigate the control problems Berle and Means first identified. "In a general sense, the most severe limitation of the capital market is that it is an external control instrument. It has limited constitutional powers to conduct audits and has limited access to the firm's incentive and resource allocation machinery" (Williamson, 1975, p. 143). Foremost among these internal mechanisms is the multidivisional or M-form organizational structure: "The organization and operation of the large enterprise along the lines of the M-form favors goal pursuit and least-cost behavior more nearly associated with the neoclassical profit maximization hypothesis than does the U-form [functionally structured] organizational alternative" (Williamson, 1975, p. 150, italics deleted). The decomposition of firms into semi-autonomous profit centers, in this argument, introduces incentives within the firm's internal structure to generate division profit as a check on managerial discretion.

In capital-centered resolutions to the corporate control dilemma, then, agency theorists focus on discipline brought about through external market forces while transactions costs theorists emphasize discipline

Fig. 7.1. Capital-Centered Models of Corporate Governance: One-Way

Control Exercised by Independent Shareholders.

brought about through adaptations in internal organization. However, both views, along with Berle and Means', share an orientation toward corporate governance in which shareholders, managers, and firms are viewed as differentiated positions with control moving vertically downward along a linear pathway in which capital is the primary constituency of interest.

A STRATEGIC (INTERORGANIZATIONAL) MODEL OF CORPORATE OWNERSHIP

For many investors, the capital-market-centered model accurately conveys how they see their relationship with the companies in which they hold shares. In the United States especially, the ideology of shareholding as corporate ownership is strong among both individual and institutional investors, leading to a wide range of shareholders' rights associations and advocates. Capital is seen as hiring managers who in turn hire workers.

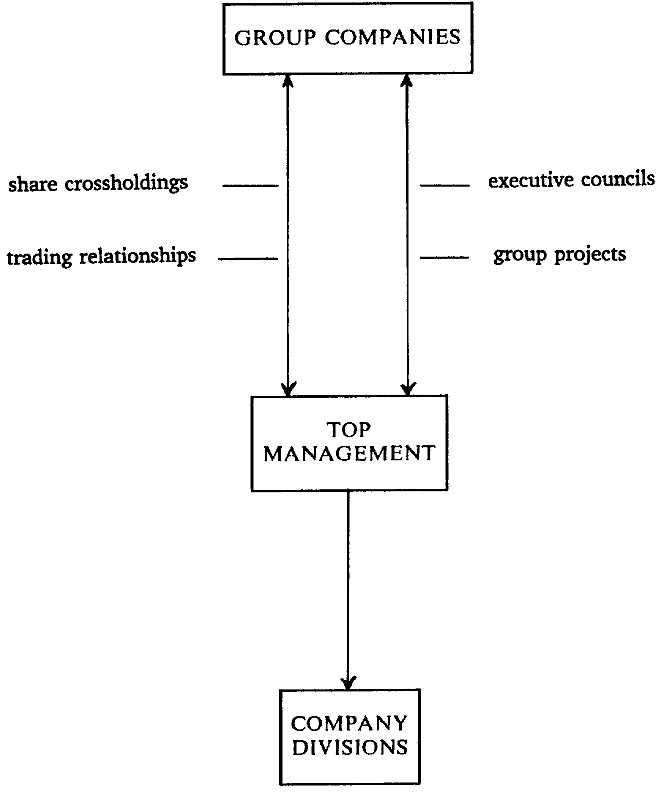

But stockholding can also be used to express a second set of strategic (interorganizational) interests-that is, as a means of consolidating business relationships rather than for direct returns on investment. This is a direction that recent work within the transactions costs perspective has started to move, by placing increased emphasis on intercorporate relationships and the means by which "credible commitments" can be created across organizational boundaries through the mechanism of partial equity investments (Williamson, 1985; Teece, 1986). When this pattern of relations is extended to the broader community, as it is in Japan, the result is a view of corporate ownership different from both capital-centered and purely managerial models: neither the exercise of clearly defined, vertical control by independent shareholders over managers (as suggested in capital-centered theories of the firm), nor the removal of managers from the competitive pressures of external interests (as managerial control theories suggest), but the merging of shareholder and managerial positions into complex networks of overlapping intercorporate interests. This image is depicted schematically in Figure 7.2.

Investors in Japan are embedded in social and business relationships among the top executives in affiliated companies (e.g., through the presidents' councils of the keiretsu and other collective activities) and are often tied together in mutually controlling relationships. The distinction between shareholders' roles as "principals" and managers' roles as "agents" blurs, as corporations become interlocked in complex sets of overlapping ownership and business relationships. Chapter 3 compared Japanese and American stock ownership patterns and found substantial empirical differences in the following areas:

1. Concentration of Ownership. Diversification of a portfolio of stocks for the purpose of risk diffusion is a more important goal for U.S. investors and the establishment of concrete intercorporate relationships a more important goal in Japan. This difference results in much larger

Fig. 7.2. An Interorganizational Model of Corporate Governance: Reciprocal

Control Exercised Through Business Networks.

average investments by major shareholders and more concentrated overall ownership in Japan than in the United States.

2. Stability. Ownership of corporate shares in Japan is carried out primarily not through anonymous securities markets of fluidly moving individual and institutional traders, but through networks of corporations whose identities are known and whose relationships are durable. Leading shareholders, therefore, take stable positions in other companies.

3. Reciprocation. The distinction between owners and owned in Japan breaks down as shareholders lose identity as a discrete constituency. Managers serving as agents of owners in their own firm become themselves "owners" over other firms by virtue of their firm's equity positions. This is seen most dearly in the prevalence of reciprocal share crossholdings.

4. Embeddedness. The position of capital, as defined through corporate ownership, furthermore loses meaning in Japan as investments are embedded in ongoing business transactions among firms and cannot be separated from other facets of the interfirm relationship. Ownership becomes part of a larger, multiplex set of business interests.

While distinct interests are dearly observed in the Japanese business community (e.g., in conflicts between securities houses and banks, and between export- and domestic-oriented companies), the kind of fundamental and pervasive tension that exists between management and shareholders in the United States (Coffee, Lowenstein, and Rose-Ackerman, 1988) is largely absent in Japan. But the Japanese resolution to the shareholder-management problem is not so much to make managers act more like shareholders, as Berle and Means and many others have proposed for the United States. Rather, it is the opposite: to make shareholders act more like managers. The Japanese firm's leading share holders are themselves other business firms run by career managers who have had to work their way up competitive internal corporate hierarchies. Corporate financial officers use their companies' shares to promote their company's business interests and are constrained by the fact that their company's own shares are often held reciprocally. The result is an economy in which the role of professional managers is great, both in running their own companies and in influencing the decisions of others, and the role of professional investors correspondingly small.

THE RISE OF JAPAN'S MANAGERIAL ECONOMY

Japanese alliance structures developed hand-in-hand with changes in the Japanese corporation itself. The postwar period witnessed the removal of top executives from the leading zaibatsu subsidiaries, leaving salaried managers to run what was left. These managers saw their role primarily as professionals, a fact reinforced by changes in Japanese corporate law in 1950 that eliminated the requirement that managers must be share-

holders in order to sit on boards of their own companies. This put in place a new generation of managers who rapidly pushed Japan's reconstruction:

Freed from the control of the holding company and from stringent government regulations that had constricted Japanese industry for almost a decade and a half, the long-pent-up energies of these young men found fresh outlets. Despite the generally conservative character that Zaibatsu had acquired toward the end of the prewar era, many of these younger executives were endowed with an entrepreneurial spirit. Thus, within two or three years after their ascendancy, these men had established a firm control over the enterprises they managed. [Yoshino, 1968, p. 87]

It was in this context that the contemporary permanent employment system developed. While managers of large firms during the prewar period had enjoyed a relatively high degree of job security, it was not until after the war that this security became more broadly institutionalized and extended to factory workers (Taira, 1970; Koike, 1983). Yet, by turning companies' personnel from a variable cost in production to a fixed cost, internal labor markets forced firms to stabilize their external relationships by gaining reliable access to critical resources-capital, raw materials, component supplies, and distribution channels-in order to ensure steady employment.

Alliance structures promoted close ties to banks, the main source of capital in the postwar economy, as well as to the large trading firms. They also internalized shareholder relationships, protecting firms' employees from hostile outside interests, something that became increasingly important with the gradual but inevitable liberalization of Japanese capital markets. As internal labor markets were becoming an institutionalized feature of Japanese business, share crossholdings within the groups rose substantially.

Thus, with the dissolution of the zaibatsu during the postwar period and the democratization of the Japanese economy came the belief that it was not the zaibatsu families but the firm's employees and other key constituencies whose interests should be served by the company. The late 1940s and early 1950s saw the increasing extension of permanent employment privileges to all core employees, and this was facilitated by the simultaneous consolidation of the groups, which created a stable institutional environment for these developments to take place. Alliance development in Japan was therefore set in the context of the special characteristics of the Japanese firm, and vice versa.

ADMINISTERED MARKETS FOR CORPORATE CONTROL

While the intercorporate alliance has become the key link between the Japanese firm and key external constituencies, it has done so in ways that alter the nature of each. In the market for corporate control, anonymous or arm's-length shareholders-notably large institutional investment trusts seeking portfolio returns-are replaced by a closely connected community of mutually positioned, long-term financiers and trading partners. As a result, it is largely an administered market in which mergers and acquisitions take place among parties closely familiar with one another and hostile takeovers are virtually nonexistent.

Mergers and Acquisitions

Among the striking features of the merger and acquisition market in Japan is the great emphasis placed on gaining the approval of key constituencies. The process of merger is a long, time-consuming one that resembles an extended courtship. A Japanese consultant who had arranged several acquisitions by foreign firms of Japanese companies described it as follows: "Price is only the last item of discussion, in contrast with the U.S. approach. Instead, we emphasize the advantages of the company itself. In particular, we show them how the acquiring firm can help their company expand into international markets and gain new access to new technologies." Another consultant said: "At first the Japanese owner can't accept the fact that he is selling his company, and so we talk about the foreign company taking a percentage of equity. . .. Most important, the sellers want guarantees that they and their people are not going to be dismissed."

The most important and most difficult constituency to appease is the company's employees, and particularly its enterprise union. A number of important mergers have been postponed or canceled because this approval could not be obtained. One early postwar case involved the Asahi and Sapporo breweries. Although they had been split up after the war, the chief executives in each company wanted to remerge. However, the employees of Sapporo objected, since the head of Asahi was widely known as a "despotic leader," and the merger talks were abandoned only two days after the plan for the merger was announced to the press (Nakane, 1972, p. 59).

The firm's external affiliates-its trading partners-are also important. They were, for example, a major source of problems in the merger proposed in the late 1960s between Dai-Ichi Bank and the Mitsubishi Bank. Dai-Ichi's customers were worried that the larger Mitsubishi Bank would favor its own customers, particularly Mitsubishi group members, after the merger and that Dai-Ichi's customers would be overlooked. They pressured Dai-Ichi to cancel merger plans, and Dai-Ichi later merged with a bank of its own size, Nippon Kangyo. Similarly, in the ill-fated merger attempt between Sumitomo Bank and Kansai Sogo Bank in the mid-1970s, both employees and affiliated firms joined forces to oppose the merger. Together, the employees, branch offices, and customers of the much smaller Kansai Sogo bank formed the Kansai Bank Preservation Association (Kansai Sogo Ginko o Mamoru-kai) with the intention of frustrating merger plans, again over concerns that they would be relegated to second-class status. This group carried out a campaign widely picked up by the Japanese media, which played on themes of Sumitomo's social responsibility, on the importance of the preservation of smaller companies, and even on the necessity of maintaining the employees' ikigai (their purpose or meaning in life). Sumitomo eventually abandoned its merger efforts.

One of the consequences of the importance of external constituencies is that mergers across alliances are quite rare. One of the few large intergroup mergers took place in 1964 and involved Mitsui Senpaku and Osaka Shosen (of the Sumitomo Group), forming Mitsui-OSK Lines. At the time, this led to a belief among some in the business community that outside mergers (keiretsu o koeta gappei ) would become more common. However, this has not happened. Okumura (1983, pp. 68-69) provides data on large-scale mergers (post-merger size of greater than ¥ 1 billion) from 1953-81. Of the ninety-nine mergers listed, fifty-three were between group firms, thirty-one between independent firms, and only fifteen between group firms and outside firms. Certainly the most important within-group merger was that of Shin-Mitsubishi Heavy Industries, Mitsubishi-Nippon Heavy Industries, and Mitsubishi Shipbuilding in 1964, re-creating the old Mitsubishi Heavy Industries concern that had dominated heavy industry in the prewar and wartime period and had been broken up by Occupation authorities following the war. Also important was the merger in 1969 of Kawasaki Heavy Industries, Kawasaki Airplane, and Kawasaki Heavy Vehicles into a reunited Kawasaki Heavy Industries. In both cases, longstanding informal ties among managers had been maintained before the remerger.

Why would top management bother to consider the opinions of employees and trading partners if they had decided a merger makes rational economic sense? In large part, this is because core employees of large firms come packaged with the companies involved. This is the case both in the stricter sense that Japanese firms make strong commitments in their internal labor markets with informal employment guarantees, and in the looser sense that firm and employee share a kind of social co-destiny. A large part of business activity in Japan is carried out through relationships among people based on social frameworks developed over long periods of interaction, rather than through formal definitions of roles and responsibilities. These frameworks are not easily meshed, as suggested in the following observation:

In Japan the use of financial power to take over what other corporations have laboriously created is considered to run counter to good business morality. But perhaps the more pragmatic reason is the virtually insurmountable difficulty of merging two close exclusive communities into an efficient business organization. [Hattori, 1984]

Problems in trying to mesh different social systems have arisen in a number of recent mergers and acquisitions in the United States as well, but these are if anything even more severe in Japan. The predominance of relationally based interaction means that it is difficult to place a money value on the worth of the company since it depends so much on the successful completion of intangible, informal, person-dependent routines. Moreover, potential efficiencies or synergies are more difficult to capture. As a consequence of permanent employment, merged firms cannot eliminate overlapping positions easily. Company directors and others must be guaranteed of their position until they retire. In addition, under nenko joretsu employees are assigned positions and compensation based heavily on their seniority status within the firm.[3] There are also social considerations based on the respective statuses of the two firms. It is often thought within the Japanese business community that mergers among similarly sized companies, a "marriage of equals" (taito gappei ), are most likely to succeed. In the words of one executive who had been involved in several mergers, "As in marriage, if one partner is too beautiful, it won't last."

The importance of relational statuses in these marriages has resulted in the widespread use of a nakodo, or go-between. As in the o-miai (arranged) marriages still prevalent in Japan, one firm approaches its main bank or a business leader who knows both parties well, who then

quietly contacts the other party. This is no guarantee, however, that negotiations will flow smoothly, as revealed in the bank-arranged marriage in 1976 of the Ataka and C. Itoh trading firms. At the time C. Itoh was thriving while Ataka was nearly bankrupt owing to various bad deals it had made and to general mismanagement. The merger arrangements were unexpectedly delayed for nearly one year over a deadlock in the negotiations on the merger terms between C. Itoh and Co., on the one hand, and Sumitomo Bank and Kyowa Bank, the two main correspondent banks of Ataka, on the other. Issues dividing the parties included which company would take responsibility for Ataka's bad debts (Sumitomo eventually took the bulk of the responsibility) and what the status would be of Ataka's unprofitable divisions (they were excluded from the agreement). The go-between may facilitate the process of merger, but it remains a complex and difficult process in Japan because of the intertwining of firm and alliance interests.

Hostile Takeovers

Easily the most dramatic event in the market for corporate control is the hostile takeover, a microcosm of the multiple forces that define the firm and its key constituencies. The tender offer has achieved the status in economic theory of guardian over the modem corporation. Since Manne's (1965) pioneering article, the threat of takeover has been considered an important means of disciplining management, even in problematic situations where ownership and management are separated. The fundamental idea is that discipline is achieved through competition among management teams within the area of the stock market, and incumbent management is thereby driven to operate the firm efficiently.

However, hostile takeovers of the kind prevalent in the United States are virtually nonexistent in Japan, and this fact reveals as dearly as any the degree to which the "market" for corporate control takes place not among arm's-length traders in impersonal capital markets but among firms that maintain longstanding relationships with each other. The factors affecting the merger and acquisition market in Japan, described above, apply a fortiori to takeovers.

In the mid-1970s, for example, an investment group made up of Japanese doctors (and therefore independent of the conventions of the Japanese business community) had acquired about 30 percent of the shares of Asahi Breweries. Asahi's share of sales in the beer industry was declining and its overall performance had been poor. Asahi's main bank

was Sumitomo, which arranged for Asahi Chemical (no relation) to pick up part of Asahi Breweries' operations. In addition, the bank sent down a number of its own executives to serve as officers in the company, including the new president of the company. Most important, it negotiated with the investment consortium to sell out its shares to the bank and to other "friendly" companies, including other Sumitomo group members (Okumura, 1983, p. 214).

Japanese firms view the intentions of foreign firms with particular suspicion. Foreign ownership of Japanese stock has increased substantially over the past two decades and accounted for about 5 percent of total shareholding in the mid-1980s, up from only 1.4 percent in 1961. Because of the tendency of Japanese institutional investors to hold onto their shares, foreigners, although holding only 5 percent of total shares, account for about 20 percent of all trading on the Tokyo Stock Exchange (Business Week, October 15, 1984). In 1969 Isuzu and General Motors announced that the latter would buy shares of the former. MITI, under pressure, at this point raised the limit of foreign capital participation to 35 percent (from 25 percent) on the condition that a substantial portion of the shares be held by stable shareholders. An executive of Fuji Heavy Industries was reported to say at the time of Fuji's break with Isuzu Motors: "I think it is advisable for our company and Isuzu Motors to continue holding each other's shares in spite of their liquidation of ties, so that we can remain each other's stabilized shareholders. Also it is desirable that the automobile firms as a whole hold one another's shares regardless of group affiliations, in order to defend native capital" (quoted in Ballon, Tomita, and Usami, 1976, p. 22). Since this time, Toyota and Nissan have been particularly aggressive in buying shares of their supplier parts companies to preempt foreign corporations.

In 1971 the Finance Ministry revised the securities exchange to allow foreign takeovers of Japanese companies. However, despite this liberalization, there have been almost no major transactions in corporate assets involving foreign firms in Japan. In 1985, for example, a British-U.S. investment group attempted a hostile takeover of the Japanese company Minebea. This attempt was defeated, however, when the investors found Japanese corporate shareholders unwilling to sell their shares. The market is in principle open but in reality internally regulated by the parties involved.

In addition to structural ownership barriers, the business community has established informal sanctions against threats to the internally determined promotion system of the firm (Ramseyer, 1987). Corporate man-

agements and unions work together to expel outsiders in the philosophy of jibun no shiro wa jibun de mareore, "protect your own castle." The colloquial term for takeover, nottori, is the same word used to refer to an airline hijacking, and the obvious image has been one of illegitimately attempting to control somebody else's property. Similarly, kaisbime, or buying shares in a company confidentially with the intention of reselling it to management at a substantial premium, retains an image of questionable business practice perhaps even more dubious than the American practice of "greenmail." In an effort to appear more progressive, imported words such as TOB (takeover bid) and M & A (mergers and acquisitions) have gained greater currency in recent years. These activities have gradually become more widely accepted, at least where Japanese acquisitions of foreign firms are involved and where the acquisition is friendly. But under other circumstances, the image to the vast majority of the Japanese business community remains a negative one.

THE REDEFINITION OF CORPORATE GOVERNANCE

With the transformation in the market for corporate control has gone a symbolic redefinition of the nature of corporate governance itself. Although the legal trappings of the joint stock corporation are maintained, they have been transformed into pro forma rituals intended primarily to satisfy the requirements of procedural legitimacy but largely devoid of real substance. This is most strikingly evident in the operation of two traditional institutions of shareholder control-the general shareholders' meeting and the board of directors.

Shareholders' Meetings

The general shareholders' meeting (sokai ) is, along with the board of directors, the primary institution within which owners can, in principle, pass on the performance of the management they have "hired." The Japanese Commercial Code establishes an ambitious agenda for the meeting: the election of directors, approval of the balance sheet and income statement, as well as determination of dividends. The reality, however, is that it is a legal formality-a ceremony, the significance of which lies not in what gets communicated between shareholders and managers but in what it indicates about control over the firm and in the ways it satisfies demands for legitimacy in the larger business commu-

nity. Large, stable shareholders do not typically bother to show up. In nearly 80 percent of the firms, those attending meetings account for less than 20 percent of the company's shares (Heftel, 1983, pp. 169-70).

The ceremonial character of the sokai reached perhaps its extreme expression in the first shareholders' meeting ever of Nippon Telephone and Telegraph (NTT) in September 1986. As part of its privatization, NTT must now operate under the formal practices of a public stock corporation rather than as an arm of the Ministry of Posts and Telecommunications. During its first meeting, its only shareholder was the Ministry of Finance, which still held all of NTT's stock. However, dutifully keeping with its new status, NTT went through the motions of a shareholders' meeting, rented a meeting room, and lined up its key executives on one side. At the other end of the room was a single individual-the representative from the Ministry of Finance-who approved everything that was offered at the brief meeting.

Since the sokai is the company's face to the outside world, Japanese executives are particularly sensitive to the image they convey during the meeting. A group of racketeers, the sokai-ya, have emerged to take advantage of this situation. These investors are in some ways caricatures of those management gadflies in the United States, such as the Gilbert brothers, who advocate increased shareholder democracy. Many sokai-ya establish "economic research centers" or similar establishments as a front for their blackmail operations. For the price of a small block of shares, they are allowed to attend companies' shareholders' meetings. Sometime before the meeting, the sokai-ya visit the responsible executives and threaten to divulge to the public at the meeting company problems or scandals involving its officials-in the early 1970s, pollution issues were common-unless they are paid off. Management, fearful of bad publicity, has typically acquiesced. While expensive, this practice has had the advantage for executives of turning the sokai-ya into advocates of management. The paid-off sokai-ya attend the meetings and keep dissident shareholders in line through intimidation. In this way, sensitive proxy contests and other forms of shareholder protest are avoided.

The annual meeting has been dubbed sban-sban sokai, after the onomatopoeic term for the unison clapping that closes festive occasions like weddings and companies' year-end parties. Management makes several brief opening remarks, offers a teisboku kosu (set menu) of decisions and policies to be approved, then seeks the approval of those attending in what used to be known as a "Soviet-style election." If all goes well and

the sokai-ya have been mollified in advance or do not show up, the meeting should last about ten to twenty minutes.[4] Well over half of all listed companies have their meetings on the same day of the year-the final Friday of June-and this has increased significantly in the past several years. This appears to be a way for companies to minimize sokai-ya impact-by all having meetings on the same day and at the same time, it makes it more difficult for the sokai-ya to attend more than one meeting.

In October 1982 the government passed new laws designed to alter the management-shareholder relationship.[5] These were intended to make it more difficult for sokai-ya to buy one or a few shares in a company and use them to strong-arm either management or other shareholders, their effects are still uncertain. In the first year after enactment, a number of companies faced what the Japanese media termed "marathon sokai." Sapporo Beer's sokai lasted for 7 hours, Isuzu Motor's for 6, Komatsu's and Kirin Beer's for over 5, and Kajima Construction's, Nippon Carbon's, and Mitsubishi Oil's for better than 4. The longest of all was Sony, consuming an embarrassing 131/2 hours. Overall, the average length of meetings increased from 15 to 50 minutes. In the marathon sokai, shareholders asked pointed questions about company social-expense accounts, the independence of the company's auditors, directors' compensation, and other potentially controversial issues that had formerly been suppressed.

Yet despite these attempted changes, the special shareholder-management relationship found in Japan largely remains. The corporate investors that predominate as shareholders of large Japanese firms still leave management to determine firms' internal operations and external strategies. Influence, where exerted, takes place through other means, such as the presidents' council. While this leaves the door open for opportunistic individual shareholders like the sokai-ya to dominate the shareholders' meetings, the goals of the sokai-ya are not to maximize returns on investment, as one would expect from traditional investors in the U.S. model, but to receive compensation in other forms (i.e., hush money). They may be a nuisance, but the sokai-ya exercise little influence over how managers actually run their companies.

The Board of Directors

In Chapter 4, we discussed the peculiar characteristics of the boards of directors of large Japanese firms in comparison with their U.S. counter-

parts. These boards almost entirely comprise full-time managers in the firms they "direct." Some of these managers have been dispatched by other companies in the group to take up full-time positions in the receiving firm, but most are career employees. Thus, despite the close connections that alliance partners share with one another, interlocking directorships are relatively scarce among major corporations.

The U.S. conception of corporate officers is largely absent in Japan, and as a result, the board of directors' meeting has the flavor of a top-level executive meeting. The jomu-kai (meeting of top executives) has replaced the torishimariyaku-kai (board meetings) as the de facto locus of control. As one indication of this, we can look at the function of the company's auditor, who is in charge of supervising the management track record set by the directors. The shareholders of the company are granted the legal authority to appoint this position. However, these positions are almost universally filled by career employees rather than by outsiders, and the job serves primarily as a rubber stamp for the board (which is itself largely internal). The job is often so insignificant that the term for auditor, kansayaku, is sometimes facetiously referred to as kansanyaku, "officer of leisure" (Heftel, 1983).

This is not to say that the Japanese firm is undisciplined by its external constituencies, however, for the shacho -kai, main bank relationships, and other external monitoring arrangements are indeed capable of constraining firm management. Among these, the case of the shacho -kai is perhaps most interesting. It has little power of direct control over its companies (a fact that clearly distinguishes the postwar councils from their prewar counterparts). Budget and personnel decisions are considered in all but exceptional circumstances (e.g., when a group company is undergoing bank-organized restructuring) to be under the jurisdiction of the firms themselves and their management. Companies' new products and technologies may be discussed at meetings but are not dictated by the group. Even were the shacho -kai to be considered a legitimate forum for the exercise of control over individual companies, it is extremely unlikely that this could be accomplished within the short time in which the group meets or within its highly informal structure. In the words of one Sumitomo executive, "We are a big company now and cannot be run even from the president's office. How could the Hakusui-kai or some other Sumitomo grouping do it?"

Rather, the shacho -kai serves as a forum for the representation of a complex nexus of interests among a coalition of affiliated financial lenders and trading partners. In some ways, it serves as a substitute for

the corporate board in a system where outside directors representing nonmanagerial interests are lacking. However, the shacho -kai represents these interests in a way that is different for the board of directors in at least two respects.

First, unlike members of a board, who retire, die, or leave for other reasons, members of a presidents' council participate in an ongoing social collective that outlasts the tenure of any one individual. The apparently ad hoc manner in which board directors who exit are replaced in the U.S. (e.g., Palmer, 1983) suggests that board participation in the United States is a sporadic process, and perhaps one that serves to link firms not to any specific set of external constituents but to the broader community of corporate leaders (Useem, 1984). The shacho -kai, in contrast, consists of a predefined set of highly visible actors with which the firms have historically carried on a variety of lines of business.

Second, the shacho -kai is an informal institution in which the monitoring function is diffused. There is no defined or legally binding governance relationship between the council and its firms, and as a result, influence is negotiated between relatively equally sized firms based on internal group relations rather than on formal authority vested in law. Associated with this is the fact that governance within the shacho -kai occurs within a known and controllable set of actors. Membership in the group is carefully defined, and control inside takes place among mutually positioned firms in a kind of community-based form of governance-as both governor and governed.

CONCLUSION

The redefinition of the firm in Japan raises what appears to be a paradox: managers have largely removed themselves from competitive markets for corporate control and in the process have reidentified the interests of the firm as their own. Yet at the same time, they have given up a considerable degree of autonomy in the embedding of their firms in external networks of other firms. It is in the resolution of this apparent paradox that the role of the contemporary Japanese manager is given meaning. For just as managers have become agents of other firms on which their own companies depend, so too have they become principals whose interests are to be served in those firms. The two roles have merged into a broader constituency that includes both financial institutions and their customers, shareholders and their managers. Unidirec-

tional relationships based on simple flows of equity capital have been replaced by reciprocal relationships based on complex flows of trade in capital, goods, and personnel. The pressures they face from external constituencies come from those over whom they, in turn, have influence. The seemingly crisp categories of principal and agent become fuzzy as the managers of one firm become the owners of another, and in turn are held by managers of that firm. It is less that management has been separated from control, therefore, than that control has been merged into management. These relationships are then embedded in other business relationships, and ownership ceases to be a separate constituency.

As a result, the nature of ownership and corporate control is transformed. Transactions in corporate assets through mergers and acquisitions among large firms are greatly reduced and require the approval of employees and trading partners, while hostile takeovers are all but nonexistent. Moreover, the institutions of shareholder representation-the board of directors and general shareholders' meetings-lose importance except to satisfy legal and normative requirements in the business community. Ownership is important as much for symbolic as for legal reasons. One manager described an equity position as "working like a kind of engagement ring"-once engaged, influence takes place through the dynamics of the relationship as it develops over time rather than through formal shareholder positions.

CASE STUDY: CORPORATE CONTROL AND THE MITSUBISHI OIL BUYOUT

News hit Japan in the spring of 1989 that T. Boone Pickens, a well-known Texas oilman and player in the American takeover movement, had acquired a substantial block of shares in Koito Manufacturing Co., an auto parts supplier affiliated with the Toyota group. In conjunction with the 21 percent of Koito's shares that he had reportedly acquired, Pickens claimed the right to three board seats, a figure equal to those of Toyota Motors with 19 percent of Koito's stock. Koito rejected Pickens' claim, arguing that Pickens was merely a short-term shareholder and knew nothing about the automobile industry. For two years the two sides attacked and counterattacked in a full-scale public relations war.[6] Finally, in the spring of 1991, Pickens dropped his claims and abandoned

the offensive, asserting exhaustion in trying to deal with "exclusionary" relationships in the Japanese economy.

Extensive media attention and the fame (or notoriety) of its chief protagonist, together with the suspense of the annual shareholders' meetings where Pickens and Koito's top management faced off, lent a certain soap-opera quality to this affair. Despite the drama, the reality is that very little of substance actually happened in the relationships among the principals during the time period involved. The reason is that the script had already been written well before Pickens stepped in, and there was little to be done to change it. Koito's relationship with Toyota and its other leading shareholders had been consolidated many years earlier. Koito's strategy, which ultimately prevailed, was simply to wait out an impatient (and possibly politically motivated) American shareholder activist while trying to win the public relations war. It was, in short, a trench war with the battle lines drawn.

This raises the issue of just how those battle lines are formed in the first place. More specifically, how are large-block stable shareholdings in Japan established; how do they evolve over time; and what does this tell us about the nature of corporate control in Japan?

In order to understand these considerations, it would be useful to observe relationships at work in a dynamic setting. A good candidate for this task is the case of Mitsubishi Oil, which was partially consolidated within the Mitsubishi group in 1984. Analysis of the specifics of this case makes evident the strategic character of major shareholding relationships in Japan, both in gaining control over flows of critical resources and in overcoming the unwanted solicitations of foreign firms. In addition, it demonstrates in some detail the ways in which closely affiliated companies interact to determine corporate ownership structures in Japan. In the buyout of Mitsubishi Oil's shares, it was its own corporate group, and especially its lead bank and trading company, working through the group presidents' council, that was central.

The Mitsubishi Oil affair began in January 1984 when it appeared that Texaco was going to acquire Getty Oil, which for many years had held 50 percent of Mitsubishi Oil stock. If Texaco succeeded in buying Getty, there was a high probability that the stock held by Getty would be released. Texaco itself had reasons to make a quick sale in order to help finance its purchase of Getty Oil. In addition, the leadership of Texaco had not shown interest in the past in the low-profit refining and sales divisions that constituted Mitsubishi Oil's main business activities. Should Texaco choose to unload these shares, bidding was expected to

be competitive because Texaco, cash-strapped with its recent purchase, would seek a high price.

Mitsubishi Oil executives became concerned that, unlike Getty Oil, which had exercised little influence on Mitsubishi Oil, a new owner might be tempted to be more involved in internal management. These concerns were shared by the Mitsubishi group as a whole. According to a managing director in Mitsubishi Bank at the time, the group's chief worry was that any Getty stock in Mitsubishi Oil that might be released would wind up in what was described as hen na tokoro, or a "strange place" (Nihon keizai shinbun, January 25, 1984). Important negotiations between Texaco and the Mitsubishi group began in April and agreement was reached in May of that year that the group would buy the Texaco-Getty interest in the company. As a result of this transaction, Mitsubishi Oil's ownership structure became dominated by other Mitsubishi group firms.

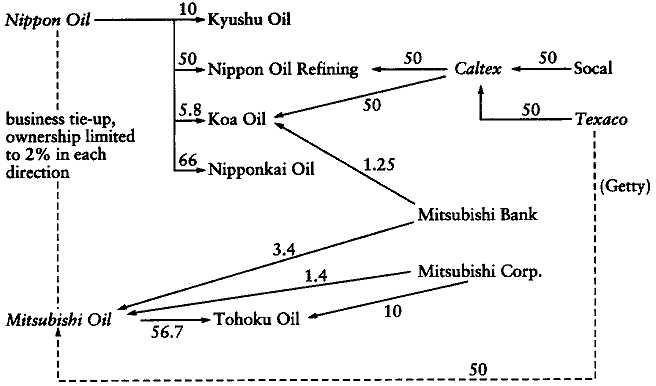

Before the Mitsubishi group stepped in, Texaco had considered selling its shares either to Caltex (a joint venture of Texaco and Standard Oil of California) or to a third party from Kuwait. The acquisition by Texaco of Getty's position in Mitsubishi Oil came right at the time of the restructuring of the oil industry in Japan, which involved several tie-ups and mergers brought on by a crisis in the oil industry resulting from overcompetition, high costs, inefficiency, and red ink. Mitsubishi Oil was a key player and whoever they tied up with would become the leader in the oil industry.

A sale to Caltex represented an unappealing option in the context of the intricate network of linkages that existed among the oil companies themselves at the time. The most pertinent of these are depicted in Figure 7.3. The danger was that Nippon Oil and Texaco, which had close business ties with each other, would gain the upper hand at a time when negotiations for a Nippon Oil-Mitsubishi Oil sales tie-up were being put forth as part of a government-sponsored restructuring of the petroleum industry in Japan. Nippon Oil was linked with Texaco's affiliate, Caltex, through Nippon Oil Refining, a refining operation that was 50 percent financed by Caltex. In addition, Nippon Oil received its crude oil supply from Caltex.

With Texaco's purchase of Getty Oil came a problem of the handling of the Mitsubishi Oil stock held by Getty. If left as is, it was inevitable that the influence by Texaco on Mitsubishi Oil would increase dramatically. According to one industry source at the time, "Nippon Oil, borrowing strength from Texaco, may set about on a takeover [kyushu

Fig. 7.3. Relationships Between the Nippon Oil and Mitsubishi Oil Groups.

Source: Nihon keizai shinbun, May 29, 1984. Note: Arrows show direction

of investment and numbers show percentages of ownership.

gappei ] of Mitsubishi Oil, which is what Nippon Oil is said to have in mind" (Ekonornisuto, February 7, 1984).[7]

The sale of shares to an independent party was also a possibility. Early in 1984, the Kuwait Petroleum Corporation probed MITI for approval to obtain Texaco's 50 percent stake in Mitsubishi Oil. On the basis of price, there was a strong likelihood that Texaco would sell to these investors. Texaco told executives in the Mitsubishi group that, with concrete offers in hand, it wanted the final answer on what Mitsubishi was willing to pay no later than May 7. However, MITI intervened in this process by announcing that it would not allow sale of Mitsubishi Oil stock from Texaco to Kuwaiti interests, prohibiting the transaction by means of the Foreign Exchange Act (Nihon keizai shinbun, April 25 and 29, 1984).

This left the Mitsubishi group itself as the most promising large-block purchaser of the Mitsubishi Oil shares. Mitsubishi group interests in the purchase reflected in part a desire to protect the group name and logo. As an executive in Mitsubishi Corporation, the group trading company, put it, "We wanted to keep the three diamonds on gasoline stands throughout Japan" (Business Week, September 24, 1990). In addition, group companies were seeking to protect the business relationships they had in each other. Negotiations were under way at the time, for example, to use 4,500 Mitsubishi Oil gasoline stations around Japan as a point of sale

TABLE 7.1. BREAKDOWN OF THE PURCHASERS | |

Purchaser | % of Total |

Kinyo-kai members (27 companies, | about 30% |

Major agents (20+ companies | about 7% |

Companies with customer relationships | about 13% |

SOURCE:Nihon keizai shinbun, July 6, 1984. | |

for automobiles produced by Mitsubishi Motors, with the aim of selling 50,000 cars per year this way (Nihon keizai shinbun, May 31, 1984).

Among all Mitsubishi group firms, the company with the largest business interests at stake (other than Mitsubishi Oil itself) was Mitsubishi Corporation. This trading firm was the leading importer of overseas energy products in Japan and about 40 percent of this business was connected with Mitsubishi Oil. Mitsubishi Corporation came out aggressively for groupwide acquisition of Mitsubishi Oil stock in order to avoid being placed at a strategic disadvantage. According to one Mitsubishi executive at the time, "It's because Mitsubishi Corporation was fearful of the loss of commercial rights. This was a case where, if Texaco were to continue to retain indefinitely its 50 percent share of Mitsubishi Oil, it would have to buy just Texaco Oil. With that, Mitsubishi Corporation's oil business would be dealt a serious blow" (Zaikai, September 4, 1984).

Still, given the large amounts of money likely to be involved, it was not expected to be an easy transaction and had to be carefully coordinated. This job fell to the leadership of the Kinyo-kai, the Mitsubishi group presidents' council. The primary figures involved in organizing the deal were Otsuki Bunpei, chairman of Mitsubishi Mining and Cement, who was concurrently chief executive (sewanin daihyo ) of the Kinyo-kai, Nakamura Toshio, chairman of Mitsubishi Bank and assistant chief executive of the Kinyo-kai, Yamada Keizaburo , vice chairman of Mitsubishi Corporation, and Ishikawa Kiyoshi, president of Mitsubishi Oil. In addition to his role as chief negotiator, Nakamura of

TABLE 7.2. LEADING SHAREHOLDERS | ||

Company | Equity % | Major Business Relationships |

Mitsubishi Corp. * | 20.0 (1.4) | Holder of commercial rights to Mitsubishi Oil's output |

Tokio Fire & Marine Ins.* | 5.0 (3.5) | Leading casualty insurance under-writer for Mitsubishi Oil |

Mitsubishi Bank * | 5.0 (3.4) | Main bank and lender of 30.7% of Mitsubishi Oil's loans |

Mitsubishi Trust * | 3.2 (2.8) | Manager of Mitsubishi Oil's marketable securities and lender of 8.7% of its loans |

Meiji Mutual Life* | 2.8 | Leading life insurance underwriter for Mitsubishi Oil |

Nihon Shoken Kessai | 2.7 | - |

Chiyoda Engineering* | 2.7 | Major contractor for Mitsubishi Oil |

Mitsubishi Heavy Ind.* | 2.0 | Major supplier of equipment to Mitsubishi Oil |

NYK* | 2.0 | Leading shipper for Mitsubishi Oil |

Industrial Bank of Japan | 2.0 | - |

SOURCES:Kaisba nenkan (1986), Japan Company Handbook (1986), and journal sources. Notes: Equity percentages in parentheses refer to pre-buyout figures. Firms marked by a "*" are members in the Mitsubishi Kinyo-kai. | ||

Mitsubishi Bank also took charge of obtaining the necessary financing of the stock purchase. Later, after the buyout was completed, Otsuki retired from his leadership position at the Kinyo-kai and Nakamura replaced him.

The negotiations were complicated by speculation in the Tokyo Stock Exchange which raised the price of Mitsubishi Oil stock from just over ¥300 per share in mid-December to an all-time high of ¥550 per share on January 24, 1984. As a result of this increase, price became a sticking point between the two parties. Texaco demanded ¥90 billion for the 150 million shares that it owned, based on the current market price of the shares plus a small premium for its large-block interest. The Mitsubishi Group countered with an initial offer of ¥40 billion, based on the per share price just before the turn-of-the-year appreciation began. Even-

tually, the two sides settled on a price of ¥77 billion ($335 million at ¥230 yen to the dollar), or about ¥513 per share. The actual transaction took place in July 1984 (Nihon keizai shinbun, May 2 and 12, 1984).

The ownership structure of Mitsubishi Oil was changed dramatically after the buyout. The majority of the Texaco-Getty shares were purchased by Kinyo-kai members, as shown in Table 7.1. The remaining shares were sold to other investors with business interests in Mitsubishi Oil, primarily leading sales agents and large customers not formally associated with the Mitsubishi group.

Among Kinyo-kai-member firms, Mitsubishi Corporation, with the most to gain or lose, was the largest buyer of shares, increasing its equity stake from 1.4 percent to 20 percent and moving from the number six to principal shareholder. In return for its investment, it placed one of its own energy specialists, Matsuda Tadao, in a specially created position of vice chairman in Mitsubishi Oil's top management. As Table 7.2 indicates, other Mitsubishi firms with business interests in Mitsubishi Oil also became major shareholders. With an increase from 3.4 percent to 5.0 percent of the shares, Mitsubishi Bank not only helped to finance the share acquisition; it also lent nearly one-third of the company's total borrowed capital. Serving as leading shareholders were Mitsubishi Oil's main insurance underwriters, while leading contractors, equipment suppliers, and shippers-all within the Mitsubishi group-also bought major positions. As a result of this ownership change, total shares held by closely affiliated companies increased from about 20 percent to about 50 percent, consolidating Mitsubishi Oil's role as an intimate part of the group.