Chapter II

Rethinking Market Capitalism

Anthropologists, sociologists, and historians have long pointed to the meshing of social and economic spheres in traditional and non-Western economies: in the village fairs, household production systems, family companies, and informal community networks that dominated much of the daily life. It is widely assumed, however, that this "embedding" was lost during the development of modern market capitalist economies, as economic transactions were disconnected from each other and from other ongoing relationships in the society. The contemporary industrial economy is viewed instead as being driven by the engine of impersonal exchange, the very anonymity of which is the source of its efficiency-or, alternatively, of the anomie that it engenders.

That present-day economies are themselves far from this impersonal ideal is a view gaining prominence within the field in which it has long been most forcefully argued. The new institutional economics (Williamson, 1985) now emphasizes that economic theory can and must face up to the limits of atomized, anonymous markets and has set about to explain the institutional forms that have developed in modem economies to overcome these limits. Of particular interest has been the role of long-term contracting and corporate organization as alternatives to competitive price-auction markets. Markets and capitalist enterprises are seen, therefore, not as isolated entities running on a logic of their own, but as complex institutional arrangements embedded in a society's legal order and the basic rules under which actors operate.

This chapter introduces some of the central themes in this debate with

the belief that a rapprochement among these perspectives is essential to developing a general theory of economic organization applicable not only to the West but to Japan as well. Even within the context of advanced market capitalist economies, we observe the emergence of significant nonmarket institutions that create efficiency-enhancing order in trading relationships. In this, the institutional economists' critique of perfect competition models is relevant. At the same time, the institutions that create this order extend well beyond formal corporate hierarchies and contractual arrangements defined in well-codified property rights to a wide variety of intermediate and informal forms of coordination and cooperation oftentimes more familiar to noneconomists. Understanding this complex and overlapping network of institutional arrangements is essential to an understanding of economies as faits sociaux totaux.

The term "market capitalism," oddly enough, is rarely defined in discussions of comparative economic systems. Indeed, its component words are often used as synonyms. Yet while it is perhaps acceptable to refer to market economies and capitalist economies interchangeably when contrasting systems based on decentralized decision making by private actors with those based on socialist planning, this should not obscure differences in the underlying emphases of each. As we see in this chapter, institutional variations in "market" and "capitalist" arrangements can and do exist, and each has its own independent significance.

Markets comprise the organized circulation of valued goods and services. They represent a form of institutionalized exchange process that, as Hodgson (1988, p. 174) suggests in his broad approach to the question, "help[s] to both regulate and establish a consensus over prices and, more generally, to communicate information regarding products, prices, quantities, potential buyers and potential sellers." Furthermore, because market transactions involve contractual agreement and the exchange of property rights, the market consists as well of "mechanisms to structure, organize, and legitimate these activities." Market institutions, for this reason, concern not only the precise terms of trade (i.e., prices) but also the general dynamics of interaction among the traders themselves and the legal and social context within which exchange takes place.

Discussion of the nature of capitalism shifts attention to one particularly important subset of markets. These markets are constituted, of course, by the flow of capital that represents the lifeblood of business operations. But at least as significant as capital per se are the rights to power and influence over how that capital is allocated and, ultimately, to

control over contemporary economies' primary decision makers, the corporations.

In the first section of this chapter, we consider the operation of markets as they actually function in Japan and other real-world economic systems, focusing on the limits to impersonal exchange and the separation of social and economic spheres of life that underlie perfect competition models. In the second section, discussion shifts to consideration of the nature of capitalism as a pattern of higher-level control over market assets, and most important, over an economy's capital-allocation and corporate decision-making processes. Linking these component parts, and a key area of difference between market capitalism in Japan and the United States, is the market for corporate control-the social structure of influence relationships between investors and companies.

THE SOCIAL STRUCTURE OF MARKETS

The problems of economic organization are in many ways universal: how to organize exchange effectively among disparate actors whose interests only partially overlap and where conditions are continually changing.[1] But the solutions vary widely across economic systems. In this section, we consider three perspectives on the role of market organization in economic systems. In the first view, represented by Karl Polanyi and his followers in the comparative and historical analysis of economies, impersonal markets are seen as widespread, but only in the context of modern, Western society. A second view, most fully developed by the French historian Fernand Braudel, questions the uniqueness of present-day Western markets and demonstrates that marketlike processes, as measured by the sensitivity of trading patterns to underlying conditions of supply and demand, have been prevalent throughout the world at many points in time. The third view, emerging from within institutional economics, emphasizes that even though market forces may represent an implicit and inevitable "state of nature" (as pointed out by Braudel), truly anonymous exchange even in modern economies is in practice rare and limited to a relatively narrow band of routine transactions.

Karl Polanyi's Comparative Study of Economic Systems

The competitive price-auction market takes as its starting point the assumption that economic relations have been and ought to be separated from other ongoing relationships in society. This perspective has come

under increasing criticism by a number of writers in recent years (e.g., Granovetter, 1985; Hodgson, 1988). But it was Karl Polanyi, writing several decades earlier, who argued most persistently against this position, both as a social ideal and as an empirical reality in most parts of the world and at most times in history. Since this influential interpretation relates directly to the issue of the comparative development of economic institutions, it is worth reviewing his basic arguments.

Polanyi's approach was broadly interdisciplinary, using a range of historical and anthropological data to create a system of comparative economics. The basic thesis of Polanyi and his followers was that economic theory applies only to the modern market economy and cannot be used to explain traditional or non-Western societies. Whereas the modern market economy operates under its own internal drive mechanisms through decisions by rationally calculating individuals, economic relationships in premodern societies have been marked by their "embedding" in a larger social system. For this reason, the comparative study of economic systems must begin from the substantive meaning of the term economic, not from its formal, or rationalistic, meaning (Polanyi, 1957, p. 243):

1. "The formal meaning of economic derives from the logical character of the means-end relationship, as apparent in such words as 'economical' or 'economizing.' It refers to a definite situation of choice, namely, that between the different uses of means induced by an insufficiency of those means."

2. In contrast, "the substantive meaning of economic derives from man's dependence for his living upon nature and his fellows. It refers to the interchange with his natural and social environment, in so far as this results in supplying him with the means of material want satisfaction."

The nineteenth century, Polanyi argued, was a unique period of history when the economy in Europe became separate from the social structure, economic motives were freed from social control, and a process was set in motion whereby economic concerns came to dominate society. "Once the economic system is organized in separate institutions, based on specific motives and conferring a special status, society must be shaped in such a manner as to allow that system to function according to its own laws" (1944, pp. 63-64). Only during this one period did the formal, rationalistic definition of the economy match up with the substantive definition. Polanyi's methodology for getting at these social

structures was through observing the concrete flows of actors and resources:

In the whole range of economic disciplines, the point of common interest is set by the process through which material want satisfaction is provided. Locating this process and examining its operation can only be achieved by shifting the emphasis from a type of rational action to the configuration of goods and person movements which actually make up the economy. This is the task of what we will here call institutional analysis. [Polanyi et al., 1957, pp. 241-42]

Recurrent patterns of flows that defined the fundamental institutional forms of integration in a society gave it unity and stability. While different institutional patterns might coexist in a single economic system, the societies Polanyi observed were presented as dominated by one type of economic organization. Three fundamental patterns were observed in traditional societies: reciprocity, or "movements between correlative points of symmetrical groupings in society"; redistribution, or "movements towards an allocative center and out of it again"; and exchange, or "vice-versa movements taking place as between 'hands' under a market system" (Polanyi, 1957, p. 250).[2]

Polanyi left no doubt that his sympathies lay with the first two, reciprocity and redistribution, but not with market exchange. He was a utopian who saw no place in utopia for the "higgling-haggling" of the market or the "obsolete market mentality" (1944). Market trade was viewed as a marginal activity in most societies, largely incompatible with the dominant pattern of reciprocity or redistribution. Nonmarket societies sheltered themselves from the divisiveness of market exchange in various ways. The institution that interested him most was the "port of trade." This was Polanyi's term for a settlement that acted as a control point in trade between two societies. These served the function, Polanyi believed, of isolating market relationships with outsiders from the remainder of society-that is, of creating a buffer between two different social systems.

Despite the originality of his ideas, Polanyi's Rousseauistic vision of harmonious, integrated primitive societies (not uncommon among functionalist writers at the time) prevented him from seeing significant elements of market exchange in the societies he was studying and led him to ignore elements of reciprocity and role-ordered exchange in modem market economies.[3] It would be just as easy, for example, to interpret the port of trade quite differently: as an institutional framework for defining the rules and ordering exchange among strangers and for creating sanctions where those of the community do not operate. A significant feature

of ports of trade, Polanyi noted, was that they operated under an administration that regulated features within them, confining trade to official channels and restricting access, requiring that transactions be made in an approved place and form, and subjecting them to a judicial authority able to settle disputes on the spot. We find these same features in modern societies within the quintessential market institutions, stocks and commodities exchanges (Telser, 1980; Leblebici and Salancik, 1982). One might better argue, therefore, that the first goal of most institutionalized markets, including stocks and commodities exchanges, village bazaars, and perhaps even the port of trade, is to facilitate exchange rather than to buffer the society.

The Great Transformation? Braudel's Critique

Polanyi's study of the embedding of economic relations in preexisting social structures was an important contribution to the theory of the organization of economies. He was able to make compelling the notion of the economy as an instituted process and to develop a comparative framework for classifying patterns. Still, his position concerning "the great transformation" in the development of the nineteenth-century market capitalism-in which an embedded economy existing in a presumed pristine state in an earlier period gave way to a rationalized economy dominated by self-contained markets-merits critical review, particularly as we try to understand the conditions necessary for the rise of market institutions in the West and as we apply this analysis to the rise of the institutions of Japanese market capitalism. This critique may be approached from two directions: first, by questioning the absence of market exchange in traditional and non-Western societies; and second, by challenging the predominance of impersonal exchange in modern market economies.

From the first direction, Fernand Braudel's epic trilogy on the development of Western market capitalism, Civilization and Capitalism, 15th-18th Century, has much to say. Braudel offers what in many ways is an extended argument refuting the Polanyian position on the uniqueness of modern-period market institutions. This is most explicit in the second volume, The Wheels of Commerce (1979), in which Braudel directly challenges Polanyi on the issues of methodology, data, and interpretation (though perhaps not granting him sufficient credit for his theoretical insights).

In Braudel's view, Polanyi's historical analysis is subject to methodo-

logical criticism in that, rather than follow a single economy through time to observe the persistence and transformation of institutional relationships, Polanyi tries to draw single-point-in-time comparisons across heterogeneous samples.

There is no law against introducing into a discussion of the "great transformation" of the nineteenth century such phenomena as the potlatch or kula (rather than, say, the very diversified trading organization of the seventeenth and eighteenth centuries). But it is rather like drawing on Levi-Strauss's explanation of kinship ties to elucidate the rules governing marriage in Victorian England. Not the slightest effort has been made to tackle the concrete and diverse reality of history and use that as a starting point. [Braudel, 1979, p. 227]

As a result, Polanyi on the one hand fails to see inchoate forms of markets in centuries prior to the nineteenth and in places other than Europe:[4] "alongside the 'non-markets' beloved of Polanyi, there always have been exchanges exclusively in return for money, however little. In rather minimal form perhaps, markets nevertheless existed in very ancient times within a single village or group of villages-the market being a sort of itinerant village, as the fair was a sort of travelling town" (p. 228). And on the other, Polanyi ignores the fundamental social element intertwined with the workings of even market economies.

[The] notion of the "self-regulating market" proposed in this research-which "is" this or that, "is not" the other, "cannot accommodate" such and such a deformation-seems to be the product of an almost theological taste for definition. This market, in which the only elements are "demand, the cost of supply and prices, which result from a reciprocal agreement" is a figment of the imagination. It is too easy to call one form of exchange economic and another social. In real life, all types are both economic and social. [Braudel, p. 227]

This is not merely an idle issue, for it relates to the entire issue of how one interprets the social organization of market economies. If Braudel and not Polanyi is correct, then patterns of economic organization found in nineteenth-century Europe are likely to have made their appearance long before, as well as in other parts of the world. We find in Braudel's longue durée not radical discontinuities but slowly evolving mixtures of institutional forms, some of them a kind of primitive market capitalism. In defense of this position, Braudel devotes considerable energy toward presenting statistical and other data to buttress his argument that market forces defined by underlying conditions of supply and demand were in operation centuries before the nineteenth in ways that marked Europe as a market-influenced regional system. He concludes:

Historically, one can speak of a market economy, in my view, when prices in the markets of a given area fluctuate in unison, a phenomenon the more characteristic since it may occur over a number of different jurisdictions or sovereignties. In this sense, there was a market economy well before the nineteenth and twentieth centuries. . .. Prices have fluctuated since ancient times; by the twelfth century they were fluctuating in unison throughout Europe. Later on, this concord became more precise within ever stricter limits. [Pp. 227-28]

Are Contemporary Industrial Economies Really Dominated by Impersonal Markets? The Institutional Economists' Critique

Braudel points to ways in which price-based market processes are observable in pre-nineteenth-century, traditional economies. A different critique of market theory has emerged recently within economics itself, arguing that modern economies, even if sensitive to underlying market conditions, need not be and often are not based on ideal-type, impersonal exchange. A central theme in the new institutional economics is that economic organization varies around a continuum defined at each end by markets and firms. Perfectly competitive markets-impersonal, atomized, arm's length-may actually be quite rare, since various formal and informal arrangements have arisen that bring parties together into relationships that are enduring or governed by other, nonmarket mechanisms. "Much of economic activity takes place within long-term, complex, perhaps multiparty contractual (or contract-like) relationships: behavior is, in various degrees, sheltered from market forces" (Goldberg, 1980, p. 338, emphasis added).

The most fully realized development of an economic approach to organization is found in the work of Oliver Williamson (1975, 1985). Key concepts in Williamson's analysis of the limits to markets are (1) transactions costs, or the "comparative costs of planning, adapting, and monitoring task completion" (Williamson, 1985, p. 2) and (2) governance structures, or the institutional arrangements designed to govern transactions and thereby reduce transactions costs. Transactions costs and the search for ways to minimize them are inevitable, Williamson argues, because economic life is inherently complex and because actors can be opportunistic in pursuing their own interests.

Following from Ronald Coase's (1937) original study of the nature of the firm and the business historian Alfred Chandler's (1962) pioneering work on the rise of the modern corporation, Williamson points to the ways in which various forms of internal organization emerge in order to

economize on transactions costs prevalent in market exchange. Receiving special attention is the M-form, or multidivisional, firm, in which operating business decisions are decentralized to independent profit centers that are connected through a central strategic capital allocation system. Williamson argues that this form improves on arm's-length capital markets in three important respects. First, it is better able to provide salaries and bonuses that are geared toward cooperative behavior among the profit centers. Second, the records of division managers are subject to review, again ensuring incentives for internal cooperation. And third, the M-form creates a greater depth of information, as opposed to the market's breadth, which allows for efficient cash flow allocation: "This assignment of cash flows to high yield uses is the most fundamental attribute of the M-form enterprise" (1975, p. 148).

With the rise of the modern corporation came changes in the basic character of economic exchange as much of it has moved from the anonymous world of the invisible hand into concrete spheres of planning and coordination. By the 1970s, the largest one hundred firms in Britain constituted approximately 42 percent of manufacturing output in Britain, 33 percent in the United States, and about 28 percent in West Germany.[5] As a result of this shift, Cable and Dirrheimer (1983, pp. 43-44) note, "a significant proportion of western economic activity now takes place within the quasi-autonomous operating divisions of giant enterprises, under strategic direction from a network of central head-offices." This represents, as they point out, "a major departure from the structural conditions of production contemplated by competitive equilibrium."

Coase's original formulation of the firm-as a realm of exchange in which the price mechanism is suppressed-might have proved profoundly disturbing within economics given the empirical importance of firm-based trading in contemporary economies. His article nevertheless received sympathetic treatment, perhaps because, by sharply differentiating between firm and market, it left the latter intact for standard economic analysis.

This pattern of clear differentiation continued in earlier transactions costs formulations as well. But more recent work has increasingly challenged the belief that even nominally market transactions are organized through impersonal exchange. Williamson (1979, 1985) argues that a variety of nonmarket relationships between companies are much more widespread than is commonly recognized. Where trading partners make investments in specialized assets that depend on the actions of others,

they require some form of guarantee, or credible commitment, from their partner that goes beyond the protections that market discipline can offer. Because the costs of writing and enforcing contracts that cover every possible contingency can be extraordinarily expensive, partners often choose instead to negotiate private ordering arrangements that bind the partners more completely than impersonal market transactions, but in more open-ended arrangements than contracts allow. Although the forms of these arrangements can vary widely, among the most important from the point of view of studying alliance structures are hostage exchanges, which include one-way and reciprocal equity investments that companies make in their business partners to ensure continued access to important resources.

In this sense, firms are, as Richardson (1972, p. 883) notes, not simply "islands of planned coordination in a sea of market relations." Interfirm transactions are themselves often structured in repetitive, informal, and socially significant relationships. The reality of contemporary market organization, for this reason, is not a strict disjuncture between markets and firms but a continuum of relationships, with many constituting a middle sphere defined by various forms of interfirm cooperation.

In a somewhat different formulation, also relevant to this discussion, A. O. Hirschman (1970) points to ways in which atomized markets and arm's-length exchange can suffer from an impoverished repertoire of governance structures. Sanctions based in the market exit option, where traders disband immediately after completing transactions, fail to convey key information that might be transmitted were the relationship to be continued. Within the nonmarket, voice option, in contrast, a portion of customers remain loyal to the products or services of the seller-even where quality is deteriorating. These traders become, in a sense, business partners, actively participating in quality improvement.

The importance of loyalty and other forms of relational contracting is particularly evident where exchange is idiosyncratic, complex, or dynamic. In these situations, prices as simplifying heuristics often do not capture proper values, and exchange is governed instead by an "immense variety of institutional supports to market processes-such as trust, friendship, law, and reciprocity" (Teece and Winter, 1984, p. 119). In the operation of real-world markets, truly impersonal transactions are limited to a small set of routine trades that take place in narrowly circumscribed and highly institutionalized settings, such as stock and commodity exchanges.[6]

And in Japan? Here as well, the firm has become a central locus of

exchange, with the largest one hundred nonfinancial firms constituting just over one-quarter of the total assets in nonfinancial sectors in the late 1960s and about 21 percent in 1980 (Uekusa, 1987). These firms have taken the additional step of organizing themselves into coherent and enduring alliance structures, resulting in a highly institutionalized arena of intercorporate cooperation, discussed below. As the share of total economic activity accounted for by Japan's largest firms has gradually declined, the number of companies with identifiable keiretsu affiliations has increased, suggesting an ongoing expansion in the proportion of total economic activity accounted for by interfirm cooperation as opposed to intrafirm control.[7]

Understanding Markets as Concrete Institutions

It becomes apparent from the above that overall economies and specific markets are organized around a wide range of institutional forms of order. Approaches to these forms vary considerably, of course. Institutional economics has focused primarily on the organization of exchange under legal institutions defined in a dearly delineated property rights structure, particularly the formal contract and the modern corporation. Polanyi, Braudel, and other historical and comparative observers, on the other hand, have emphasized the embedding of exchange in the social institutions and structures of traditional societies. The latter viewpoint is useful to keep in mind, for the existence of firms implies not only that markets have failed, but that alternative forms of social governance have too.

Differences also exist in the purposes that forms of nonmarket organization are seen as serving. Institutional economics has been concerned with the ways in which institutions arise to create order in exchange relationships where markets fail, the purpose being to improve economic efficiency.[8] Polanyi and his followers, in contrast, have been more interested in social cohesion and taming the conflict they perceive as inherent in unrestricted market exchange.

These differences, however, should not be overstated. Just as anthropologists have shown that traders in traditional economies personalize or particularize exchange relations (Belshaw, 1965; Geertz, 1978), so too are social considerations rarely absent from even the most rationally calculated business decisions in contemporary economies. A variety of studies over the past several decades have emphasized the long-term, relational character of contemporary industrial markets (e.g., Macau-

lay, 1963; Richardson, 1972; Macneil, 1974, 1978; Williamson, 1979; Okun, 1981; Granovetter, 1985; and Carlton, 1986). Carlton (1986) finds that the average length of purchasing relationships among industrial firms in his survey was between seven and eleven years. And Macaulay observes that these relationships are frequently mediated informally rather than through reliance on detailed contracts: "Businessmen often prefer to rely on 'a man's word' in a brief letter, a handshake, or 'common honesty and decency'-even when the transaction involves exposure to serious risks" (1963, p. 58). At a theoretical level, Williamson (1975) has introduced into his transactions costs framework the idea of "atmosphere" to account for the fact that people incorporate in their economic decisions information not just about the outcomes of a transaction but also about the process of exchange and the quality of their relationships with their trading partners. To the extent this is the case, characteristics of the overall social order may themselves become important in determining the efficiency of alternative modes of exchange.

When organized within alliance forms, informal relationships are taken a step further and in so doing a context for cooperation is created that is both structurally coherent and socially significant to its participants. In the view of Japanese managers, stable, symbolically identified intercorporate relationships lead to a variety of intangible benefits, among them: increased feelings of trust among the participants; a more personalized and less formal mode of interaction; improved access to the interpersonal relationships that ultimately determine how much of organizational activities in Japanese business are actually carried out; and the ability to conduct long-term decision making among interdependent companies.

The embedding of economic interests in a social context (Granovetter, 1985) does not eliminate rational considerations, however. Certainly Japanese managers tend to explain business behavior in relational rather than instrumental terms, with words like "trust" and "loyalty" appearing repeatedly in accounts of the Japanese company and intercompany cooperation.[9] But trust is a tenuous thing, even in a "high trust culture" like Japan's and even where relationships among partners have continued over decades (Gerlach, 1990; Ramseyer, 1991).

Indeed, the ubiquity of trust as a cultural characteristic of Japanese society is itself by no means universally accepted. In one influential analysis of this issue, John Haley questions the widespread belief that there is "an unusual and deeply rooted cultural preference for informal, mediated settlement of private disputes and a corollary aversion to the

formal mechanism of judicial adjudication" (1978, p. 359). Haley claims instead that low litigation rates in contemporary Japan are the product of a range of institutional barriers, among them a substantial shortage of practicing lawyers resulting from sharp restrictions on certification, long delays in obtaining court trials, and the lack of appropriate remedies for litigants.[10] In addition to a discussion of these barriers, Haley also notes two statistical facts awkward to the culturalist argument: data indicating that litigation rates in Japan have declined since the end of the second world war rather than increased, as might be expected with the modernization of Japan; and data showing that, while litigation rates in Japan are much lower than they are in the United States, they are actually higher than those found in several other Western countries.

The lack of reliance on contractual modes of exchange in Japan, therefore, is not simply the product of a deep-rooted cooperative ethic. Haley points in one alternative direction by arguing that noncontractual arrangements are the product of the weakness of the "sheath of justice" in Japan (Haley, 1982) and the resulting inability of individuals and companies to rely on legal recourse in resolving contractual disputes. The result, he continues, has been the widespread adoption of a variety of private-ordering arrangements, including promissory notes, informal mediators, and letters of guarantee.

A different direction to the issue of noncontractual arrangements among businesses is suggested by the fact that these relations are common across market economies. In explaining the prevalence of non-contractual relations among the American businessmen he studied, Macaulay (1963) notes a variety of "counterbalancing sanctions" to which sellers have access, including demanding downpayments before delivery, possession of proprietary skills that limit the ability of buyers to switch sources, and the existence of "blacklists" that hurt a company's business reputation. Macaulay's work points out that reputation is not an abstract quality, but a tangible discipline exercised both through formal channels (e.g., the risk of a bad report from credit-rating agencies such as Dun and Bradstreet when buyers fail to pay their bills on time) and through informal networks (e.g., discussions among purchasing and sales agents at trade meetings, country clubs, and social gatherings).

Contractual arrangements, therefore, are often not the preferred mode of coordinating economic activity even where the legal system and court ordering do operate effectively. The theory of incomplete contracting (e.g., Williamson, 1985) has pointed to the impossibility, as a practical matter, of including all contingencies in private contracts. Future

states of the world are difficult to predict and the substantive and procedural requirements necessary to enforce agreements in public courts are far greater than for private arrangements. Moreover, economic action requires extensive tacit knowledge that promotes smooth functioning among business partners but is difficult to codify in precise blueprints of action (Nelson and Winter, 1982).

Alliance structures deal with these problems in two ways. First, a basic set of governance mechanisms is established, with shareholding playing an especially prominent role in the process. Grossman and Hart (1986) suggest that equity ownership has the advantage of assigning control over the use of an asset in all contingencies not explicitly contracted upon. Whereas full-scale vertical integration is the usual application of this principle, an alternative is mutual shareholding among legally separate companies. Second, this basic structure of rights and responsibilities serves as the backdrop before which a wide variety of more specific informal and social ties among specific actors develop. As Zucker (1988, p. 33) notes, organizations help to resolve conflicts in self-interest that would exist without formal structures, and in this sense, they "provide frameworks within which joint action is smoothed by arriving at and retaining solutions to social dilemmas." Alliance structures create a similar framework, which in turn allows for the emergence of task-oriented routines at the interorganizational level.

In conclusion, we may point to a linking theme among the various writers considered here: a common appreciation of economic organizations as complex institutions to be understood through the observation of concrete exchange relationships. Polanyi and his followers follow "the configuration of goods and person movements which actually make up the economy" (Polanyi et al., 1957, pp. 241-42). Braudel traces the contours of everyday, material life, "guided by concrete observation and comparative history" (1979, p. 25). And transactions costs economics studies the transaction as the basic unit of analysis, which "occurs when a good or service is transferred across a technologically separable interface" (Williamson, 1985, p. 1) and explores the ways transactions become organized into the complex variety of institutional arrangements that make up contemporary economies. Markets, therefore, are best seen less as the reification of an abstract ideal-self-sustaining, self-regulating, self-functioning mechanisms running on an internal logic apart from the remainder of society-and more as social inventions that are embedded in larger institutional structures, both legal and social.

THE SOCIAL STRUCTURE OF CAPITALISM

The analysis of market organization points to a broad range of ongoing trading activities that constitute the economy as a whole. The analysis of capitalism, in contrast, focuses directly on the economy's most central actors: those who control its basic assets, especially its capital and corporations.[11] Among the significant innovations within the capitalist system, two stand out: the joint-stock corporation and the stock exchange. The corporate form, by establishing a division of labor between holders of capital and management and limiting the liability of the first, simultaneously opened up new sources of capital for faster growth, allowed for the specialization of the management function, and diffused risk across a broader set of investors. Development of the corporation also established arrangements whereby ownership interests would be represented, including the board of directors and the general shareholders' meeting. Within the corporation, the invisible hand of anonymous traders was replaced by the quite-visible hand of corporate managers (Chandler, 1977), but the firm itself was to be disciplined externally through these shareholder institutions.

Emerging in conjunction with joint stock corporations were large-scale, regulated stock exchanges. The stock market provided a highly ordered central locus for the trading of shares that corporations issued. Access to the actual trading process was limited to a specific group of exchange members. These traders in turn made their services available to a general investing public, who were granted protection through liability limits (which restricted investor risk to the amount of their investment). Linking these two institutions, the corporation and the stock market, was what is perhaps the quintessential market in capitalist economies: the market for corporate control.

Japan's opening to the West during the Meiji Restoration led to the introduction of both the corporate form and stock markets (Clark, 1979). But Japan has also crafted a distinctive institutional arrangement to mediate between the corporation and the stock market: the intercorporate alliance. Alliance structures retain the advantages of the corporate form of organization, as each of its firms operate as a legally independent entity. Outside capital can therefore be raised, a division of labor maintained, and risk diffused. But the sources of external discipline are changed dramatically, for affiliated financial institutions become an important source of capital, while stockholdings

are organized through long-term positions among companies' business partners.

The Managerial Revolution

In discussions of the relationship between the corporate form and the stock exchange, probably no book has had the impact of Berle and Means's The Modern Corporation and Private Property (1932). Berle and Means argued that the rise of the large, diffusely held, professionally managed corporation fundamentally altered the nature of the relationship between ownership and control over the firm. They worried that in separating these two functions, organizational behemoths were created that were largely unaccountable to traditional property holders and would pursue their own interests at society's expense. Much of the work in organizational economics and business history over the past two decades has, implicitly or explicitly, been an attempt to address the Berle and Means thesis by providing an efficiency rationale for the managerial bureaucracy (e.g., Chandler, 1962, 1977; Williamson, 1975, 1985; Fama and Jensen, 1983). The reality of the management-ownership separation in the United States, however, is not itself in dispute among these writers.

And in Japan? On the one hand, there are far fewer publicly traded companies in Japan than in the United States and far more privately held firms. These private companies are very often smaller and owner-managed (Patrick and Rohlen, 1987), suggesting the kind of traditional capitalist enterprise that Berle and Means admired. As of 1987, there were more than 24,000 public corporations in the United States, in comparison with less than 2,000 in Japan. Since the number of firms listed on the New York and Tokyo stock exchanges was nearly identical (at 1,647 and 1,634, respectively), the big difference is in the prevalence of smaller, public U.S. firms traded over-the-counter and on smaller exchanges, and their near absence in Japan. Public listing in Japan is limited almost entirely to the oldest, most prestigious corporations. According to one study, nearly half of all public corporations in the United States went public within the first ten years of establishment, in comparison with under 1 percent in Japan.[12]

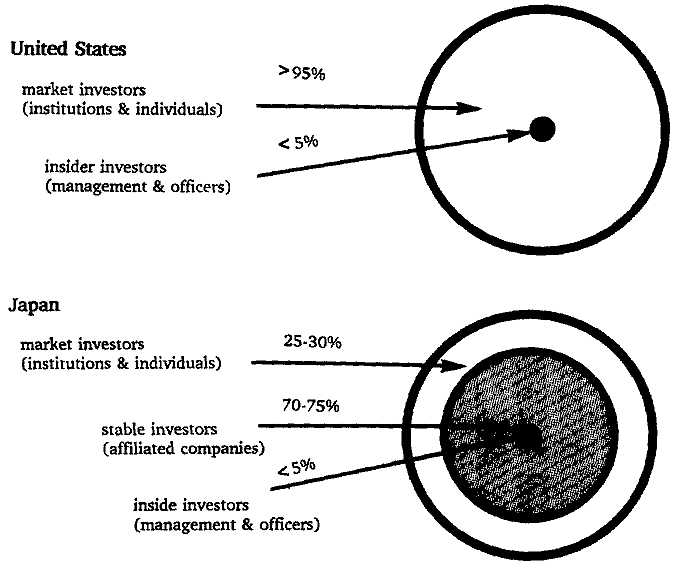

Among its largest corporations, on the other hand, Japan, like the United States, has progressed far down the road toward managerial capitalism. As of at least the mid-1970s, the ownership of shares in large corporations by their officers in both countries was negligible. Herman

Fig. 2.1. Investor Composition in Large U.S. and Japanese Companies.

(1981) finds that in nearly two-thirds of the two hundred largest non-financial firms in the United States, directors owned less than 1 percent of the voting stock. Similarly, Okumura (1983) presents statistics showing that the holdings of corporate officials (directors and auditors) in Japanese firms of over ¥ 10 billion in assets (around $400 million at 1983 rates) averaged under 1 percent in 1976. In the United States, nearly all the remainder is controlled by independent individual and institutional investors, most often in small, fractional holdings. In Japan, in contrast, a substantial portion of the remainder is controlled by alliance partners, existing in a gray area somewhere between the polarities of Berle and Means's management-shareholder dichotomy. The differences between these two systems of corporate control are depicted schematically in Figure 2.1.

What does the existence of these distinctive capital relations mean for the interaction between ownership and management in Japan? One perspective that has been taken in financial monitoring models is that it improves the capability of shareholders to learn about and to discipline

management in otherwise diffusely held corporations (Jensen, 1989). As relatively coherent shareholder bodies, this argument goes, corporate alliances are able to mobilize collectively in cases of severe managerial malfeasance in order to protect shareholder interests. This is more difficult when shareholders are poorly organized, as in the United States. It should be pointed out, however, that shareholders in diffusely held U.S. corporations enjoy control mechanisms never anticipated by Berle and Means-and largely unused in Japan-including hostile takeovers and proxy contests.[13]

Two other implications are less obvious, but at least as significant. The improved managerial discipline function of corporate alliances noted in the previous paragraph continues to view the interests of affiliate-share-holders as identical to those of other shareholders-albeit, perhaps, with greater means of enforcement and better information. But affiliate-share-holders actually have plural interests. As companies' bank lenders and business partners, these investors are interested in a more complex set of goals than capital market returns. As two observers have pointed out:

Unlike Western institutional shareholders, which invest largely for dividends and capital appreciation, Japanese institutional shareholders tend to be the company's business partners and associates; shareholding is the mere expression of their relationship, not the relationship itself. [Clark, 1979, p. 86.]

In most listed companies in Japan, a sizable portion of the stock remains permanently in "safe" hands, thus assuring continued control by management. Shareholdings are fragmented between "insiders" and "outsiders." Insiders are small circles of executives and financiers often connected with the issuer's enterprise group. . .. The insiders are in charge, not by virtue of their positions, but as a product of the multiplicity of their roles in the firm; they are creditors, shareholders, lifetime employees, management and business partners. [Heftel, 1983, p. 165.]

Moreover, they often have their own shares held reciprocally and in complex networks of shareholding among other affiliated enterprises. Companies whose shareholding bodies are dominated by affiliate-shareholders will, quite rationally, consider the interests of alliance partners first before those of independent shareholders when making investment decisions.

In addition to redefining the constraints placed on the Japanese firm, the predominance of affiliate-shareholders also shapes the character of Japanese stock markets. This is not so much through modifications in the basic regulations and rules of operation, for these are similar in most formal respects to those in the United States and elsewhere (although

actual functioning differs in several important respects, discussed later). Rather, it is through changes in the dominant players in the market. In both the United States and Japan, an "investor revolution" marked by the rise of large-scale investors has taken place that in many ways is as important to the understanding of twentieth-century capitalist enterprise as the managerial revolution identified by Befit and Means. But whereas the managerial revolution has followed relatively similar trajectories across all advanced economies in the broad sense that corporate decision making moved into the hands of nonowning managers, the investor revolution has not.

The Investor Revolution

The main concern of Berle and Means was the increasing diffusion of ownership in public corporations and the consequent loss of shareholder control, with the result that large corporations were run by professional managers rather than by firms' owners. But this trend has also had an economic rationale. To the extent that large, bureaucratic organizations were able to accomplish the objectives of reducing coordination and transactions costs for complex and capital-intensive economic tasks and smaller firms were not (Chandler, 1962, 1977; Williamson, 1975, 1985), it made sense to establish a division of labor in talent and expertise. Professional managers were to specialize in running corporations while investors specialized in the capital provision and risk-bearing function.[14] This division of labor and the corresponding managerial revolution has appeared in all advanced capitalist economies, and generally in similar industries (Chandler, 1984).

The rise of the large-scale investor represents a second but less well appreciated trend apparent in the United States and in other countries. Traditional owner-founders had interests in their companies over and above the extent of their capital investments. They were members in their business communities, linked their personal interests with those of their companies, and typically passed their companies on to family heirs. The institutional investors of the late twentieth century are instead large organizations run by specialist money managers who are linked to the investment rather than the business community and whose interests in companies are limited to the extent of their (often short-term) capital involvement. They are, in short, professional investors.[15]

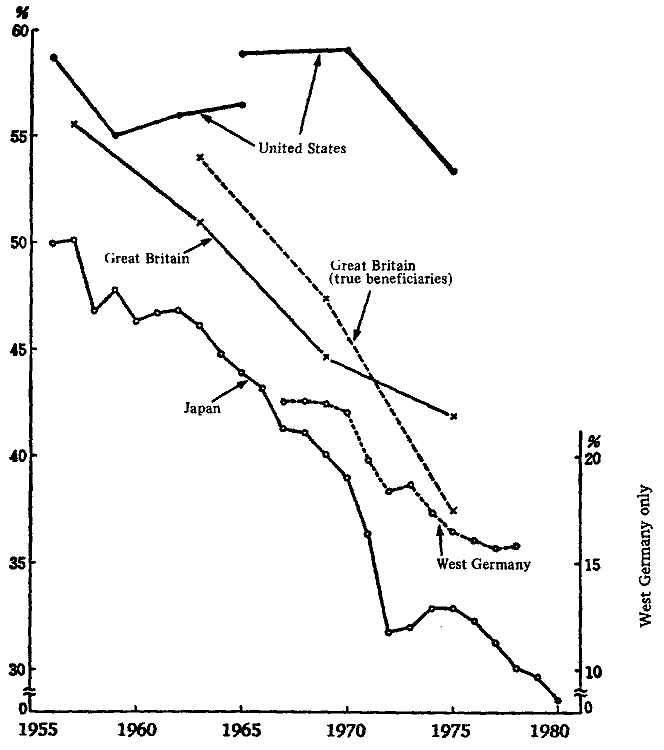

The decline in individual investment over time across capitalist economies is shown in Figure 2.2. Focusing solely on this aggregate trend,

Fig. 2.2. Decline in Individual Investors in Advanced Industrial Economies. Source: Futatsugi (1982).

however, obscures important differences in the nature of the trend. First, countries vary in the extent to which individual investors have been replaced by other investors. While individual investors still owned over one-half of the shares in publicly traded U.S. companies in the 1970s, this figure was under 25 percent in Japan and under 20 percent in West Germany.[16] The extent of decline in individual investment has proceeded even further in these two later-developing economies.

Second, and more important, the nature of the investors that have

arisen to replace these individuals varies considerably. In the United States, investors are in significant proportion managers of pension, trust, and other forms of investment funds-that is, true institutional investors. In a 1975 New York Stock Exchange survey, trust and nominee accounts constituted about 40 percent of total market value, and this figure has risen to about two-thirds since then (Aoki, 1984a; Business Week, February 4, 1985). These investors are constrained by a set of fiduciary obligations such as the "prudent man rule" and laws that stress safety and the duty to pursue the interests of the pension or trust, creating strong pressures toward acting as arm's-length market investors. As a result, the primary source of institutional investor control over corporations comes not in direct voting control but in indirect effects on share price through stock trading (Herman, 1981). By the mid-1980s, institutional investors accounted for roughly 90 percent of share turnover in American stock markets.[17]

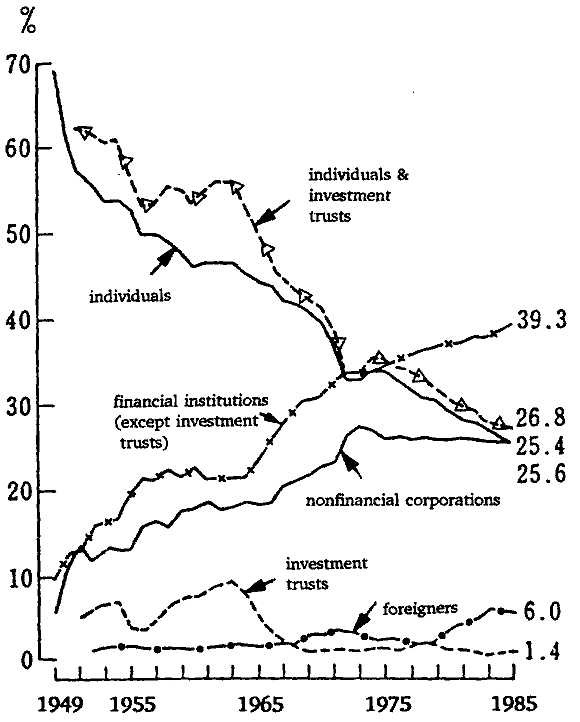

Individual investors in Japan, in contrast, have largely been replaced by other corporations (Okumura, 1975). Figure 2.3 shows how financial firms (banks and insurance companies) and business enterprises (industrial and commercial firms) make up the vast majority of share ownership in Japan. Financial firms controlled nearly two-fifths of all shares by 1985, and business enterprises another one-quarter. Investment trusts, however, controlled only 6 percent of all shares.[18] This difference is important because, as indicated above, Japanese financial and industrial investors use their shareholdings primarily in order to consolidate business relationships for strategic purposes and only secondarily for the kinds of direct (capital market) returns that are essential to investment trusts. In addition, Japanese law grants corporate investors substantial latitude in influencing management on the basis of the investor's own business interests in the company.

Despite their small numbers, however, individuals are not irrelevant to Japanese stock markets. Individual shareholders serve as the speculators that help to "make" markets in the absence of a large number of floating shares, in order for stock prices to be determined-a function similar to that of speculators in commodities markets who fill in the transactional interstices to create flexible markets among the traders that are commodity users. In this capacity, these investors have done quite well overall, at least until recently. Abegglen and Stalk (1985) calculate that among leading firms in twenty-one different industries, the stock market performance of sixteen Japanese firms was superior to that of their U.S. counterparts during the ten-year period 1973-83. Their re-

Fig. 2.3. Composition of Shareholding in Japan. Source: Nihon Keizai Shinbun (1987, p. 53).

turns in much of the latter half of the 1980s, with the rapid appreciation of share prices on the Tokyo stock market, were at least as impressive.

Stockholders, Stakeholders, and Alliance Structures

Immediately after publication of The Modern Corporation, Berle and Means became embroiled in a debate over whether they had ignored the importance of constituencies other than shareholders. Perhaps it is not stockholders alone, this argument went, but firms' collective "stake-holders" that are important. Dodd (1932) took the lead in this attack,

claiming that corporate directors had an obligation to serve as trustees for all constituencies of the companies on whose boards they sat. Others disagree. Oliver Williamson's influential contemporary analysis of the corporation (1985, chapter 12) argues that the unsecured position of equity shareholders' investments puts them logically first in the queue for corporate control, with management granted a secondary position. Constituencies other than these two are better off, Williamson asserts, protecting their business interests by direct contractual guarantees rather than through board representation.

Japan's distinctive capital relations reveal yet another approach. The interests of external constituencies get represented in Japan, as advocated by Dodd and others. But boards of directors are not the primary mechanisms for ensuring this. Rather, these constituents take equity positions in other firms in which they have business interests, creating economic stakes in those companies that serve as legitimate bases for influence, as advocated in the models of Berle and Means and Williamson. In this way, key external constituencies (banks, suppliers, customers, etc.) get represented by becoming legally empowered stake-holders of the firm. These constituents may also sit on the company's board, but Japan has crafted an alternative to the outsider director as well: the multicompany presidents' council, which brings together the top executives of affiliated crossheld companies in periodic meetings to address matters of group-wide concern. (The workings of these councils are discussed in Chapter 4.)

The interests of internal constituencies (primarily, management) are represented in two ways. Managers dominate the boards of their own companies, ensuring a substantial voice in internal decision making. Since corporate shareholding is often reciprocal, at least among large firms, managers are also able to exercise influence over the very external shareholding companies that constrain them. Mutual shareholdings represent an "exchange of hostages" (Williamson, 1985) in which attempts at control in one direction are balanced against reciprocal holdings in the opposite direction.

Perhaps what is most interesting from a comparative institutional perspective about Japanese capitalism, therefore, is the nature of investors themselves. In the United States, these investors have become largely differentiated from the activities of the firms themselves-that is, from their employees, lenders, and trading partners. We find therefore a large constituency of institutional investors that have common interests but little ongoing interest in the firms in which they hold shares. In Japan, in

contrast, corporate involvement equity shareholding is so pervasive that, without risking great exaggeration, we can say that Japanese stock markets have been transformed largely into instruments of corporate rather than purely financial interests.

CONCLUSION

Economic systems vary in the social structure of both their market systems and their corporate enterprise in ways that are complexly inter-related. Much of the market activity in advanced industrial societies has been removed from the forces of impersonal competition by organization within firms, leading to internal labor markets, internal transfer pricing policies, and other forms of exchange that have a substantial administered component. Intercorporate alliance forms in Japan have furthermore merged these organization-level interests with a broader nexus of interests companies have in each other.

In working at a level between that of isolated firms and that of extended markets, these alliances have redefined both. Japanese markets have become organized through close relationships among affiliated firms, creating a finely spun web of business networks in which preference is given to long-term trading partners over market newcomers. At the same time, these relationships have transformed the business environment surrounding Japanese managers by ensuring that the company's shareholders are its major customers, suppliers, and financial institutions rather than an anonymous body of stock market traders. The constraints Japanese companies face, therefore, are primarily those arising from their ongoing business interests rather than those of independent capital markets. It is this complex linkage of market relationships and the basic capitalist definition of the economy's core players that has given Japanese alliance capitalism its distinctive character and form.