INTERMEDIATE PRODUCT MARKETS

No doubt the most controversial issue in understanding the role of keiretsu organization in the Japanese economy is its impact on product market trade. Given the strong preferential patterns demonstrated ear-

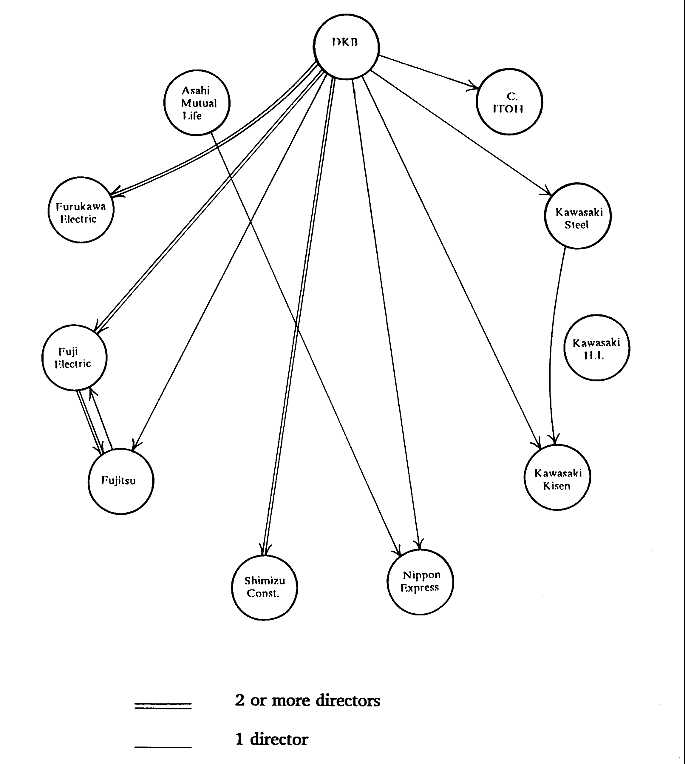

Fig. 4.7. Dispatched Directors of the Leading Companies in the Dai-Ichi Kangyo Bank Group.

Source: Data from Industrial Groupings in Japan (1982).

Note: DKB = Dai-Ichi Kangyo Bank; H.I. = Heavy Industries.

lier in networks of borrowed capital, corporate ownership, and directorships, it should not be surprising if the keiretsu are also involved in structuring linkages within intermediate product markets. As we see below, however, internalization tends to be lower in product trade than in other relationships and varies substantially according to the type of company involved. Nevertheless, the overall pattern is clearly not one of trading neutrality. In this section, we consider the extent of keiretsu structuring of product trade through direct purchases and sales (e.g., a

TABLE 4.4. TRANSACTION MATRIX FOR DISPATCHED DIRECTORS, 1980 | ||||||

Affiliation of Company Receiving Director(s) | ||||||

Affiliation | Mitsui | Mitsubishi (15) | Sumitomo | Fuji | Samoa | Dai-Ichi Kangyo Bank (16) |

Mitsui (15) | 48.0 | 0.0 | 0.0 | 7.7 | 0.0 | 0.0 |

Mitsubishi (15) | 0.0 | 60.4 | 0.0 | 0.0 | 0.0 | 3.6 |

Sumitomo (13) | 0.0 | 6.7 | 67.1 | 2.6 | 0.0 | 0.0 |

Fuji (17) | 0.0 | 0.0 | 0.0 | 25.9 | 0.0 | 0.0 |

Sanwa (19) | 0.0 | 0.0 | 0.0 | 7.7 | 36.2 | 0.8 |

Dai-Ichi Kangyo Bank (22) | 0.0 | 2.2 | 0.0 | 4.1 | 23.6 | 38.7 |

Other Cos. (137) | 52.0 | 30.7 | 11.5 | 46.4 | 40.3 | 53.7 |

Govt. Orgns. | 0.0 | 0.0 | 21.4 | 6.1 | 0.0 | 1.0 |

Total | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

SOURCE : See Appendix A. Note: Number of sample companies is given in parentheses. Owing m rounding, columns may not add up m 100%. | ||||||

steel company's purchase of a mining company's coal), and in the next section we expand the analysis to include collaborative group projects among affiliated companies.[24]

The main actor in the organization of product market relationships of both kinds has been the group trading companies. The sogo shosha are to the keiretsu trading network what banks are to its capital networks- the most centrally positioned firms, with direct linkages to most other companies in the group. For the majority of intermediate product manufacturers in a keiretsu, they are the leading overall supplier and customer. Moreover, they are important as an organizer of small- and large-scale group projects.

The sogo shosha have been critical in the historical development of the Japanese economy. By 1900 Mitsui Bussan alone handled about one-third of Japan's foreign trade. As was the case with banks, the emergence of trading companies was closely tied to that of the zaibatsu themselves:

The general trading companies developed best when they were part of a zaibatsu. Those that were started independently of the zaibatsu either did not succeed or remained small. The zaibatsu was a system that provided them with ample capital and security as well as with room for initiative. And the name of the zaibatsu assured them also of qualified personnel because of the prestige and power the zaibatsu name involved. [Hirschmeier and Yui, 1975, p. 192.]

A more recent example of this interdependent development can be seen in the case of a postwar start-up, Sumitomo Corporation. This general trading company was begun in the mid-1950s by the Sumitomo group from the fragments of a small prewar trading company in order to provide an alternative to the dominant position in international trade held by the huge trading houses of Mitsui and Mitsubishi. It grew dramatically thereafter through the advantages it enjoyed in the Sumitomo group, including large loans from Sumitomo Bank and preferential trade with other group companies. In a thirty-year period, it moved from an insignificant position in the economy to the fifth-largest firm in Japan as measured by sales (and sixteenth-largest when measured by assets).

Even today, the sogo shosha are Japan's sekai kigyo , or "world corporations." They handle a significant portion of domestic trade[25] and are the leading intermediary in international trade. In the mid-1970s they exported over 70 percent of all Japanese iron and steel products and 70 percent of machinery products and handled nearly half of machinery imports (Wall Street Journal, July 18, 1983).

There have been periodic reports of the impending decline of the sogo shosha since the early 1960s, when Misono Hitoshi published an influ-

ential article, "Is the Sun Setting on the Sogo Shosha?" ("Sogo shosha wa shayo de aru-ka," Mainichi Economist, May 1961). More recent concerns were expressed in the early 1980s when the Japanese business community began talking about "the era of winter," after the title of a bestseller at the time which predicted severe difficulties in the years ahead for the trading companies. As evidence of this, percentages of sales handled by the sogo shosha had declined by 10 to 20 percent in a number of major industries. But a revival seemed well under way by 1985, when sales of ail major trading companies were up and four of the six leading sogo shosha reported record profits (Japan Times, May 25, 1985).

Nevertheless, while reports of its demise appear exaggerated, the role of the trading firm is changing with the ongoing restructuring of Japan's economy away from heavy, industrial, and capital-intensive products toward lighter, consumer, and knowledge-intensive industries. The proportion of group trade conducted by the sogo shosha and group companies involved in heavy and industrial versus light and consumer product markets is shown for the Mitsubishi and Mitsui groups in Table 4.5. The companies that are involved in newer fields (particularly Toshiba, Toyota, Mitsubishi Electric, and Kirin) have gained on their own the overseas experience and networks that have been the trading company's advantage. Moreover, these products depend less on another of the historical strengths of the sogo shosha: trading in large volumes and capitalizing on small price differentials across markets.

Instead of moving into newer industries as trading agents, the sogo shosha are increasingly shifting their attention toward global information acquisition, representing client firms in multiparty negotiations, and arranging projects among group companies. The information-center role was outlined by an executive in the Sumitomo Corporation as follows: "Ultimately, the sogo shosha should become a sort of multinational corporation with its subsidiaries and affiliates operating in widely diversified industries throughout the world. It should play the role of a satellite: gathering, relaying and transmitting necessary information on economic and human activities, as well as money, goods and resources." The satellite metaphor is a good one, as the sogo shosha have recently been taking a leading role in arranging projects involving telecommunications and satellite technology. Two of the leading sogo shosha, Mitsubishi Corporation and Mitsui and Co., have teamed up with other companies in their respective groups to enter NASA's space program (Japan Times, October 11, 1983) and have been leading organizers of intragroup communications networks and information systems.

The sogo shosha are now involved in a wide range of functions that

TABLE 4.5. PERCENTAGE OF GROUP TRADE | ||

Sales | Purchases | |

Heavy Industries | ||

Mitsubishi Heavy Industries | 55 | 27 |

Mitsubishi Oil | 25 | 35 |

Mitsubishi Metals | 22 | 38 |

Mitsubishi Chemicals | 26 | 41 |

Mitsubishi Aluminum | 75 | 100 |

Mitsui Shipbuilding | 75 | 18 |

Mitsui Petrochemicals | 65 | 50 |

Hokkaido Colliery | 68 | 55 |

Mitsui Metal Mining | 33 | 31 |

Component-Assembly | ||

Mitsubishi Electric | 20 | 15 |

Nippon Kogaku (Nikon cameras) | 7 | 11 |

Kirin Beer | 0 | 23 |

Toshiba | 15 | 5 |

Sanki Electric | 9 | 4 |

Nippon Flour Milling | 28 | 1 |

Toyota Motors | 1 | 1 |

SOURCE : Data from Okumura (1983, p. 138). | ||

facilitate interfirm trade: searches for and negotiations with trading and joint venture partners, equity participation in resulting projects, ongoing import, export, and other sales business, and post-import financing for final sellers. For example, C. Itoh, which served in the late 1960s as mediator in negotiations for the partial acquisition of Isuzu Motors by General Motors, then teamed up with these two firms through an equity investment to form a new company for the manufacture of automobile speed variators and gas turbines. Within the keiretsu, the sogo shosha are the leading organizer of intragroup cooperative projects. As part of an extended annual review of the activities of each group, Keiretsu no kenkyu provides a summary of major projects involving two or more

firms from the same group. Considering only the Sumitomo group, we find that of twenty-five projects involving Sumitomo group companies in the years 1982-84, the group's trading company, Sumitomo Corporation, was a major participant in seventeen.

Intermediate Product Trade in the Keiretsu

Determination of the role of the keiretsu in intermediate product trade is more complicated than for the other business relationships studied here. Accurate statistics on overall intragroup patterns of trade are difficult to obtain because companies often consider this information to be sensitive or proprietary. In addition, the extent of internalization varies substantially among firms, with vertical keiretsu or other relationships of far greater importance for many companies than the intermarket keiretsu, particularly for those firms involved in complex-assembly industries.

There is certainly abundant anecdotal evidence that preferential trading does take place. One early source, the Oriental Economist (July 1959), reported that in the late 1950s Sumitomo Metal Mining (the direct descendant of Sumitomo's main Besshi mine) sold 60 percent of its copper output to Sumitomo Electric Industries and Sumitomo Metal Industries, while Sumitomo Electric filled 80 percent of its copper requirements with supplies originating from Sumitomo Metal Mining. In the 1970s, an article in Business Week (March 31, 1975) said that Sumitomo Metal Industries continued to rely on Sumitomo Corporation to sell 47 percent of its output and quoted Sumitomo Metal Mining's president as saying that 39 percent of his companies' products were going to other Sumitomo group companies that year.

The preference group companies give to others in their group has sometimes been a source of problems in joint ventures with foreign partners. One case where this came up, which was related by a consul-rant who had been part of the negotiations, involved a foreign manufacturer and a partner in the Mitsubishi group in a dispute over the pricing policy for supplies in their automobile parts joint venture. The Japanese managers in the venture wanted to use Mitsubishi group companies wherever possible to supply steel, plastics, and other materials, whereas the U.S. manager wanted to buy on the open market. A resolution was finally effected through the intervention and personal influence of the Japanese head of the joint venture-a distinguished retiree from another Mitsubishi group firm-who went directly to the Mitsubishi companies and was able to influence them to come down to competitive rates. The

TABLE 4.6. TRADE | |||

Zaibatsu | Bank | Total | |

Internalization | 12% | 6% | 10% |

11% (a) | |||

16% (b) | |||

Preferential transaction ratio | 7 | 1.7 | 3 |

3 (a) | |||

SOURCES : Figures are calculated from data provided in Imai (1982, p. 59), using percentages of tie-up contracts. Other figures are calculated from data provided by (a) Rotwein (1964, p. 66), for trade measured by principal transaction partners, and (b) Sakamoto (1983, p. 153), for trade measured by estimated total sales and purchases. | |||

purchases would still come through the same affiliated firms, only they would reflect something closer to the prevailing market price.

A number of studies have tried to utilize more rigorous measures of intragroup trade, as reported in Table 4.6. Estimates of the overall internalization of trade using data from the three sources cited here vary between 10 percent and 16 percent. Preferential transaction ratios can be calculated from data provided in two of these studies; both show that group companies are about three times more likely to engage in trade with companies in their own group than with those in other groups. Similar results are arrived at by using the data in this study on the identity of leading trading partners. These are derived from information on companies that serve as major suppliers and customers to other companies. Information on these companies is provided in Kaisha nenkan, based on firms' annual reports and other records. From these data, we are able to create a transactions matrix of major business relationships, as shown in Table 4.7. Overall internalization is again low in comparison with the earlier network relationships analyzed, ranging from 6.4 to 15.2 percent. Preferential transaction ratios are about 2.8 times, close to those found in other studies.

These results can be misleading, however, when we are trying to understand the overall importance of intercorporate affiliations in Japanese product markets. This is for two reasons. First, major companies in assembly- and service-intensive industries, such as motor vehicles and electrical appliances, rely on their own network of smaller upstream

TABLE 4.7. TRANSACTION MATRIX FOR | ||||||

Affiliation of Industrial Company | ||||||

Affiliation | Mitsui | Mitsubishi (10) | Sumitomo (10) | Fuji | Sanwa | Dai-Ichi Kangyo Bank (20) |

Mitsui (15) | 14.3 | 3.2 | 2.8 | 2.7 | 3.9 | 5.3 |

Mitsubishi (15) | 3.5 | 15.2 | 5.4 | 7.1 | 4.7 | 5.7 |

Sumitomo (13) | 1.5 | 2.2 | 12.8 | 1.9 | 2.9 | 2.6 |

Fuji (17) | 4.4 | 2.5 | 4.6 | 8.4 | 6.6 | 3.4 |

Sanwa (19) | 4.0 | 1.7 | 2.2 | 3.2 | 6.4 | 4.3 |

Dai-Ichi Kangyo Bank (22) | 6.2 | 10.3 | 6.5 | 9.0 | 8.2 | 13.2 |

Other (137) | 66.1 | 64.9 | 65.7 | 67.7 | 67.4 | 65.5 |

Total | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

SOURCE : See Appendix A. Note: Number of sample companies is given in parentheses. Owing to rounding, columns may not add up to 100%. | ||||||

suppliers and downstream distributors for the bulk of their product market transactions. Affiliated firms are typically organized within vertical rather than intermarket keiretsu and are classified as "independent" companies in the studies cited above. Second, the figures reported here refer to direct trade among companies and exclude the role of the sogo shosha.

Kotabe (1989) presents detailed data on the sales and purchasing activities of a major electronics firm, disguised in his study as "Takeshita Kogyo." Kotabe finds that this firm relied on shacho -kai firms in its own intermarket group for only 1.6 percent of its total purchases, most of these from the group trading company and several raw material and heavy equipment producers. Total sales to these firms were 1.9 percent, the majority to the group financial institutions and steel company. In contrast, about 40 percent of its total purchases came from affiliated supplier firms and fully 90 percent of its semiconductor sales passed through two captive distributors in its vertical keiretsu. As we see in Chapter 6, high levels of internalization within vertical keiretsu relationships are also typical in the automobile industry.

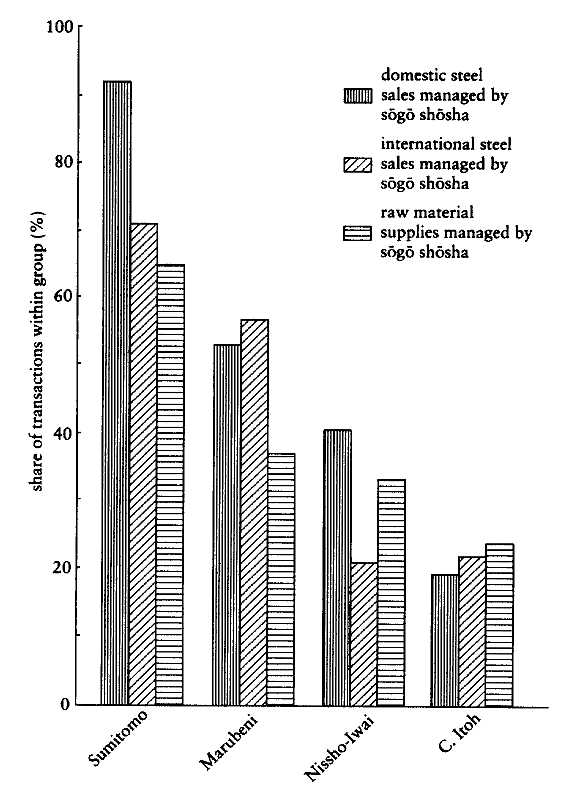

Preferential trading within the major groupings is far more prevalent among sogo shosha and other types of companies, especially those in intermediate product markets. Estimates of the overall share of sales among the zaibatsu successor companies that is channeled through the group trading firm range somewhere between 20 and 30 percent.[26] More precise information can be obtained for relationships between the sogo shosha and major steel companies from a series of volumes, entitled Sogo shosha nenkan, published annually between 1972 and 1985. The results of a series of analyses utilizing these data are reported in Figures 4.8 through 4.10.

Figure 4.8 shows the extent to which trading companies manage the transactions of the steel companies with which they are most closely affiliated. As these figures demonstrate, the extent to which supply and sales representation is identified with affiliated companies varies greatly. At one extreme, over 90 percent of the steel involved in domestic transactions managed by Sumitomo Corporation is supplied by Sumitomo Metal Industries, and over 70 percent in overseas transactions. At the other extreme, C. Itoh relies on Kawasaki Steel to supply only 20 percent of the steel that it sells in both markets. This appears to reflect, once again, the relatively weak coherence of firms affiliated with the Dai-Ichi Kangyo Bank group. Preferential transaction ratios (calculated from transaction matrices not reported here) also vary, but in most cases are

Fig. 4.8. Sogo Shosha Sales and Purchases from Affiliated Steel Companies, 1983.

Source: Sogo shosha nenkan (1985).

over 3: 1. On average, the trading companies are about five times more likely to handle raw materials for their affiliated steel companies and about fifteen times more likely to manage the steel output of those companies.

These figures also indicate two other points of significance. First, the sogo shosha/steel company relationship is of nearly equal importance in both domestic and international transactions. This reflects an important consideration in understanding the internationalization of the Japanese

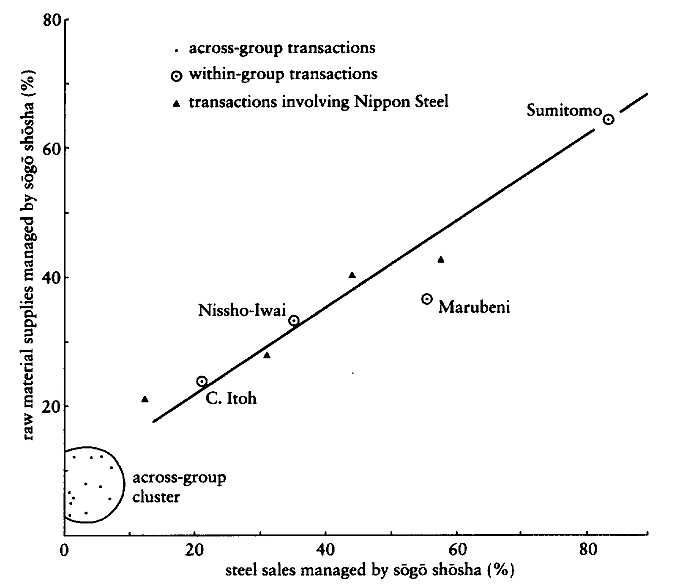

Fig. 4.9. Business Reciprocity Between sogo Shosha and Steel Companies, 1983.

Source: Sogo shosha nenkan (1985).

firm: overseas business relationships follow patterns of domestic relationships. Second, supply and sales representation relationships move together, with close ties in upstream markets associated with close ties in downstream markets. That is, business transactions are based on clear patterns of reciprocal trading.

Further evidence that supply and sales representation relationships are reciprocally linked is provided in Figure 4.9. These data report trading patterns among all five of Japan's major steel companies and the same four trading companies. In the far upper right-hand corner, Sumitomo Corporation relies on Sumitomo Metal Industries as a customer for about 65 percent of its raw material (iron ore and coking coal) sales and as a supplier for over 80 percent of its steel. Figures for the other three trading companies and their affiliated steel companies are, respectively, 37 percent and 55 percent for Marubeni and NKK, 34 percent and

31 percent for Nissho-Iwai and Kobe, and 24 percent and 21 percent for C. Itoh and Kawasaki. In contrast, both supply and sales representation relationships are minimal across groups, as indicated in the cluster in the lower left-hand corner. That this pattern of reciprocal trading also takes place among "non-keiretsu" firms is evident in the business relationships of Nippon Steel, Japan's largest and most independent steel company. As with other steel manufacturers, when Nippon Steel's purchases of raw materials for a trading company increase, so too does its use of the same company in managing its domestic and overseas sales.

Figure 4.10 shows how keiretsu-based trading relationships among these companies have evolved over the period in which the Sogo shosha nenkan volumes provide data. With the exception of a proportional drop in sales representation of Kawasaki Steel by C. Itoh in the late 1970s, the share of sales has proven strikingly stable. Throughout this period, the average share of across-group transactions (the dotted line at the bottom) has remained quite low. Once again, the results indicate that long-term, preferential relationships represent a durable and continuing characteristic of Japan's intercorporate network structures.