JAPAN'S FINANCIAL SYSTEM

In studying the significance of the keiretsu in structuring Japanese capital markets, it is essential to consider the distinctive patterns of corporate finance as they have evolved over time in Japan. The central role during the prewar period in capital allocation among zaibatsu subsidiaries was played by the holding company. During the postwar period, with the dissolution of the holding companies, this role was largely taken over by financial institutions and especially by large city banks as major lenders of capital. This created the conditions in the critical wartime and early postwar period within which more extended alliances organized around lead banks emerged. More recently, as a result of capital market liberalization and a slowing in the overall growth of the Japanese economy, there has been a proportional shift in the sources of external capital among large Japanese companies away from long-term debt toward equity and bond financing.

Despite these changes, certain underlying characteristics of Japanese capital market relationships have continued since the postwar period into the present day in modified form. These include the fundamental importance of large financial institutions in mediating between household savers and corporate users of capital; capital allocation through closely administered ties between these financial institutions and their industrial clients, even where financing takes the form of securities-based capital; and strong preferential patterns of capital supply in both debt

and equity capital markets among affiliated enterprises. As a result, when the position of banking, insurance, and securities companies are considered as a whole, we find far less change in the capital allocation process than is often believed.

The Historical Role of Financial Institutions

The financial function was already well developed in the Tokugawa economy with the large merchants playing an especially important role. Modern banking and life insurance companies, however, were not introduced until the 1870s, as an import from the West. The Japanese government encouraged the banking system in various ways but left the actual role of financing Meiji development largely to private financial institutions. These banks, particularly the large-scale city banks, emerged in dose conjunction with the development of manufacturing operations and never achieved the independent status that they did in the United States. Each inchoate zaibatsu of the Meiji period started its own bank for the purpose of funding the activities of its group companies. As Lockwood (1968, p. 222) points out,

Big banks and trust companies were securely tied into each major combine by intercorporate stockholding, interlocking directorates, and the "interrelated solvency" of these institutions and their combine affiliates. They held the deposits of affiliated companies (as well as individual depositors) and were at the same time their chief source of capital.

Those banks that had begun independently, such as Dai-Ichi Kokuritsu Bank (the forerunner of the contemporary Dai-Ichi Kangyo Bank), found it necessary to develop close relationships with a subset of dependable client firms that relied on them for the bulk of their external capital needs. Even the smaller, specialized zaibatsu (e.g., Nissan) developed their own internal financial arms for the same purposes. This supporting role is evidenced in the term that described them- kikan ginko , or "organ banks." Less often, the reverse pattern occurred, with entrepreneurs focusing primarily on developing financial enterprises and later extending these to the building of industrial empires. The Yasuda zaibatsu was representative of this pattern.

In the 1930s, as the Japanese economy was rapidly expanding to meet Japan's wartime needs, banks increasingly replaced the honsha and the zaibatsu families as the main sources of working capital for the group companies. Since banks were not prohibited from holding equity, they

became significant shareholders in their client firms, increasing their share of all nongovernment securities from about one-fifth to about one-half between 1930 and 1945. Banks also provided, through loans, over half of Japanese companies' total external capital. In total, four-fifths of all debt financing and two-fifths of all external corporate funds came from banks during this period (Goldsmith, 1983).

The close connections between financial institutions and their clients that have dominated the Japanese postwar period were, therefore, already well in place by the end of the war. This was reinforced when banks managed to escape postwar dissolution and benefited further by the freezing of bank deposits held by the zaibatsu families, releasing the banks' deposit liabilities. Industrial firms themselves were growing rapidly and had extremely high external capital requirements that could not be met by the relatively undeveloped equity market, so they turned increasingly to the banks. The postwar period was marked by a dramatic increase in reliance on bank borrowing, with stock financing declining from two-fifths of total funds in 1934-36 to less than one-tenth in 1945-53, and loans and discounts increasing from less than one-tenth in 1934-36 to considerably over one-half in 1946-53 (Goldsmith, 1983, pp. 142-43).

During much of the postwar period, relationships among the government, banks, and large corporations have been maintained through a kind of administered interdependence (Suzuki, 1980). Since capital was in chronic short supply, the government was able to ration credit among preferred institutions. Government-bank ties were reinforced through the practice of "overloans," in which banks themselves borrowed heavily from the government Bank of Japan in order to gain access to capital, which was then lent to large firms. Out of this emerged "window guidance"-moral suasion over amounts loaned by the banks to the banks' customers resulting from the Bank of Japan's position of power. The capital shortage naturally shaped banks' relationships with their corporate clients, as firms interested in expanding were forced to maintain tight business relationships with their banks by "overborrowing"-that is, borrowing beyond the company's current needs and depositing the surplus in the banks as a kind of side payment known as "compensating balances." Although financial deregulation in the 1970s and 1980s has changed these relationships in certain respects, as discussed below, this long period of interaction has institutionalized a general pattern of cooperation among capital suppliers and large corporate capital users that has remained in modified form to the present day.

The importance of large financial institutions has come not only in providing capital but also in looking out for the wide range of business interests of their industrial clients. Japanese businessmen put great emphasis on the main bank relationship. Status as the number one lending institution for a company carries with it the expectation that the bank will not only provide a significant portion of the firm's capital but will also look after its interests in a variety of ways. The main bank sends a signal to other banks about the financial health of the company, a role that Horiuchi, Packer, and Fukuda (1988) have termed a "delegated monitor" function. The main bank also ensures that the company is able to gain loans from other banks as well-a process known as "pump priming," or yobi-mizu. In 1975, for example, the Sumitomo Bank and the Mitsubishi Bank agreed to extend loans of ¥2 billion (somewhat over $5 million at the time) to the largest manufacturing companies in the other's group, Mitsubishi Heavy Industries and Sumitomo Metal Industries, on a mutual basis. This was reported to be a way to circumvent regulations enacted by the Ministry of Finance the previous year placing limits on the amounts banks were able to lend to a single customer (Okumura, 1983).

Bank assistance extends as well to helping its clients find business customers. A Sumitomo Bank executive explained as follows: "Sumitomo Metal Industries does a lucrative business now selling sheet steel to the Matsushita companies, the Nissan companies, and Toyo Kogyo, among others. They enjoy this business because the bank provided a large part of the financing for these companies and acted as go-between to get this business for them. There are many, many arrangements such as this in the group" (quoted in Business Week, March 31, 1975).

Where the company does get involved in financial problems, the main bank is expected to come to its client's rescue. An example of this was provided by a manager formerly affiliated with Akai Electric, a major video and audio tape-deck manufacturer. Akai had during the early 1980s run into financial difficulties and was under financial reconstruction with bank support. It was Akai's main bank that took the lead in its reconstruction. This was Mitsubishi Bank, which owned 8 percent of Akai's shares and was the lender of 16 percent of its borrowed capital. As part of the assistance, Mitsubishi sent three people to Akai-the chief secretary to the president, the department manager in charge of international business operations, and the department manager for international finance-as well as extending additional loans to the company.[10]

In addition to their role as lenders, Japanese banks also maintain an additional source of influence over their client companies not enjoyed by U.S. commercial banks: the ability to take equity positions in other companies on their own account. Unlike banks in the United States, which are restricted by provisions of the Glass-Steagall Act, Japanese banks typically maintain holdings of several percent of most of their main client companies' stock.[11] The fact that banks have been able to both lend capital and hold equity positions has reinforced their central positions in Japanese capital markets, and they have aggressively expanded their client base while promoting internal coordination through joint councils and projects.

The capital market relationship is reciprocated from company to bank, as firms maintain a significant portion of their own capital in their banks in the form of deposits and equity shareholdings. Hamada and Horiuchi (1987) report that Japanese nonfinancial corporations held over 30 percent of their financial assets in the form of bank deposits during the period studied, 1954-83. Companies furthermore typically hold shares of the banks that lend to them, which they are able to use as collateral on their loans. The relationship between bank and client company extends even to employee accounts, as corporate customers often have employee wages automatically transferred to an account opened for each employee with the bank in lieu of cash payments. This practice has intensified recently with the emergence of firm banking- electronic data transmission systems between banks and their client firms.

As a result of these intertwined forces, there emerged during the postwar period what one set of observers aptly term a kind of "banking-industrial complex" in Japan, with transactions in capital taking place largely through close and longstanding business associations between banks and their clients rather than through impersonal capital markets: "At the risk of oversimplification, we may characterize the American financial system as a market-oriented system. The Japanese system had more administrative or organizational aspects to its capital allocation mechanism, and in some cases the line of demarcation between 'the company' and 'the market' was rather blurred" (Flaherty and Itami, 1984, p. 158).

Capital Markets and the Keiretsu

The maintenance of the central position of the group banks was ensured by the postwar economic reforms pushed by the U.S. occupation, which

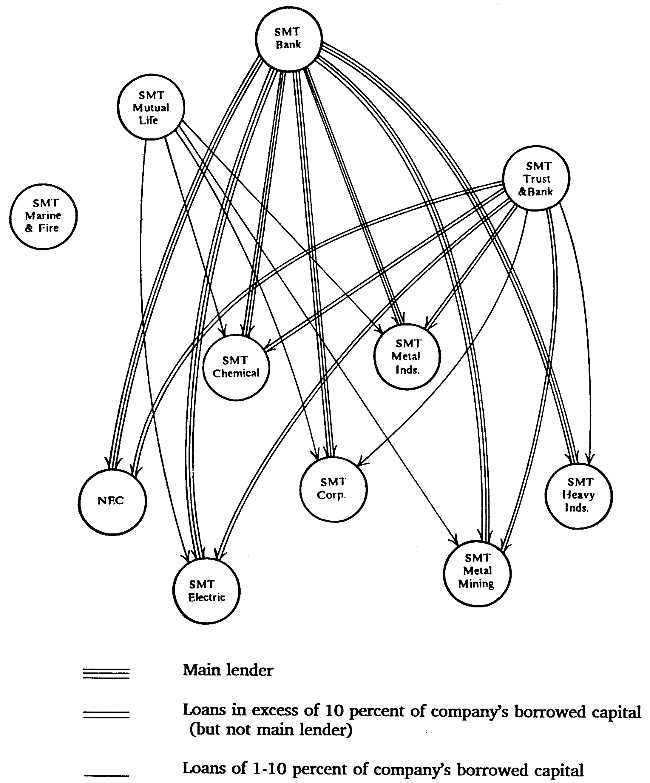

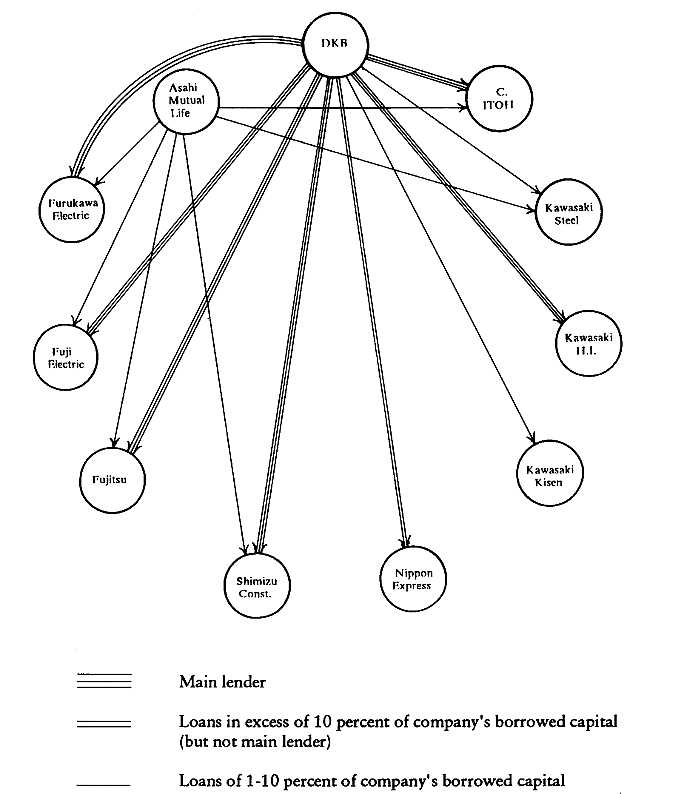

broke up the zaibatsu holding companies but not the zaibatsu banks. As a result and in conjunction with the Japanese government's policy of allocating scarce capital to the city banks through its own financial organs, these city banks reinforced their importance as the leading sources of capital for group companies and were in a position to give preference to their own long-standing clients. Groupings formed around these banks as companies were willing to forego a degree of independence in order to gain access to scarce-but-needed capital, particularly during the economic resurgence in the mid-1950s. Today we find that the large city banks associated with the six big intermarket keiretsu are the main banks for virtually all of their group companies, while other group financial institutions play an important secondary position. Figures 4.1 and 4.2 depict these relationships for the leading companies in two groups, Sumitomo and Dai-Ichi Kangyo Bank.

While the existence of close banking relationships is readily apparent in these figures, it is possible that strong banking ties exist among keiretsu firms and financial institutions in other groups as well. In order to evaluate this possibility, a transaction matrix was created for the two hundred industrial firms in our sample, based on the percentage of capital coming from firms' top-ten lenders broken down by group affiliation. These results are reported in Table 4.1 for the year 1986.

The boldface figures along the diagonal show the extent of internalization of borrowed capital to financial institutions in the same group. As we see here, intra-group capital proportions range from a low of 23.3 percent for Dai-Ichi Kangyo industrial firms to a high of 42.8 percent for Mitsubishi firms and 42.4 percent for Sumitomo firms. Most of the remaining debt capital for each group firm comes from "independent" financial institutions-an amalgamation of smaller commercial banks and insurance companies, as well as long-term credit banks. Capital linkages to financial institutions in other keiretsu account for a much smaller share of the total in each group. No single group is the source of more than 10 percent of the total capital borrowed by any other group, and in the case of Sumitomo group borrowing, the figure is zero in three cells (i.e., none of these ten companies count a Fuji-, Sanwa-, or Dai-Ichi Kangyo-affiliated financial institution among its top-ten creditors). It becomes quickly apparent from the transaction matrix that the hypothesis of substantial across-group ties in the loaned capital market does not hold for the shacho -kai firms in the sample.

The extent of bias toward affiliated financial institutions can be understood through a simple derivative measure, the preferential transaction ratio. This is calculated by dividing the share of same-group transactions

Fig. 4.1. Intragroup Borrowing Dependency of the Leading Companies in the

Sumitomo Group. Source: Data from Industrial Groupings in Japan (1982). Note: SMT = Sumitomo.

by the average for those in each of the other five groups. While internalization points to the absolute proportion of borrowing coming from one's own group, the preferential transaction ratio looks specifically at intra- versus intergroup relationships and the possibility not only that firms prefer to borrow from their own group but also that they prefer to use banks outside the other keiretsu (e.g., the Industrial Bank of Japan)

Fig. 4.2. Intragroup Borrowing Dependency of the Leading Companies in the Dai-Ichi

Kangyo Bank Group. Source: Data from Industrial Groupings in Japan (1982).

Note: DKB = Dai-Ichi Kangyo Bank; H.I. = Heavy Industries.

for their nongroup capital. In total, firms in the six big keiretsu are about 15.1 times more likely to borrow capital from financial institutions in their own group than from those in another group. What this ratio makes clear is that the identity of keiretsu affiliation is itself important in defining patterns of transactions.

Next we consider the role of the keiretsu in organizing Japanese

TABLE 4.1. TRANSACTION MATRIX FOR | ||||||

Affiliation of Industrial Borrower | ||||||

Affiliation | Mitsui | Mitsubishi | Sumitomo | Fuji | Sanwa | Dai-Ichi Kangyo Bank |

Mitsui (3) | 39.5 | 1.9 | 1.0 | 1.8 | 2.5 | 7.1 |

Mitsubishi (3) | 1.0 | 42.8 | 2.9 | 4.3 | 4.8 | 4.5 |

Sumitomo (3) | 3.0 | 3.5 | 42.4 | 5.3 | 1.6 | 4.2 |

Fuji (4) | 0.5 | 0.7 | 0.0 | 26.6 | 8.9 | 3.2 |

Sanwa (2) | 1.0 | 0.5 | 0.0 | 30.0 | 32.2 | 6.8 |

Dai-Ichi Kangyo Bank (2) | 5.8 | 4.0 | 0.0 | 8.1 | 4.9 | 23.3 |

Other Banks (29) | 49.2 | 46.5 | 53.8 | 51.0 | 45.0 | 50.9 |

Total | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

SOURCE : See Appendix A. Note: Figures represent percentages among the top-ten lenders only. Number of sample companies is given in parentheses. Owing to rounding, columns may not add up to 100%. | ||||||

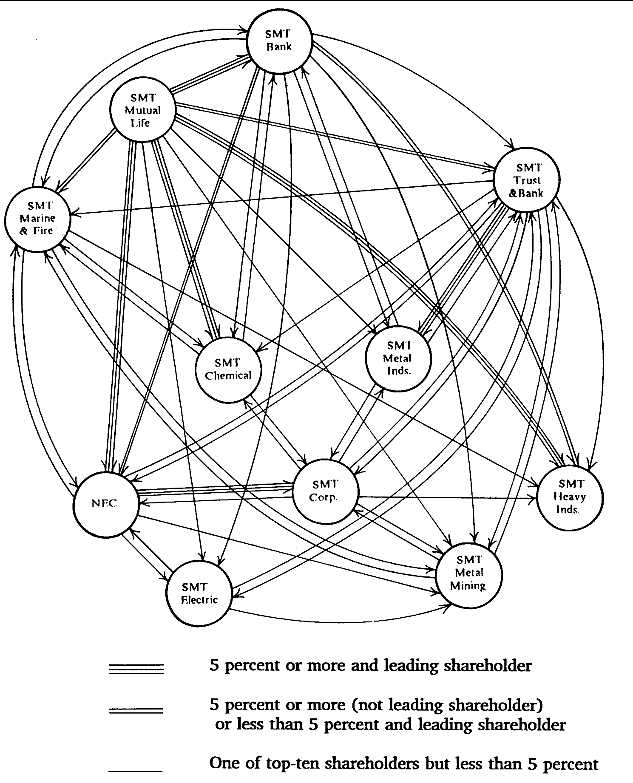

Fig. 4.3. Stuck Crossholdings of the Leading Companies in the Sumitomo Group

(Top-Ten Shareholdings Only). Source: Data from Industrial Groupings in Japan (1982). Note: SMT = Sumitomo.

equity markets. Specific patterns of share crossholdings are shown in Figures 4.3 and 4.4 for the leading companies in the Sumitomo and Dai-Ichi Bank groups. The network of crossholdings among the eleven Sumitomo firms shown here is extremely dense, with 71 percent of the possible connections actually constituted.[12] At least four of the top-ten shareholders among each of these firms are other companies in the

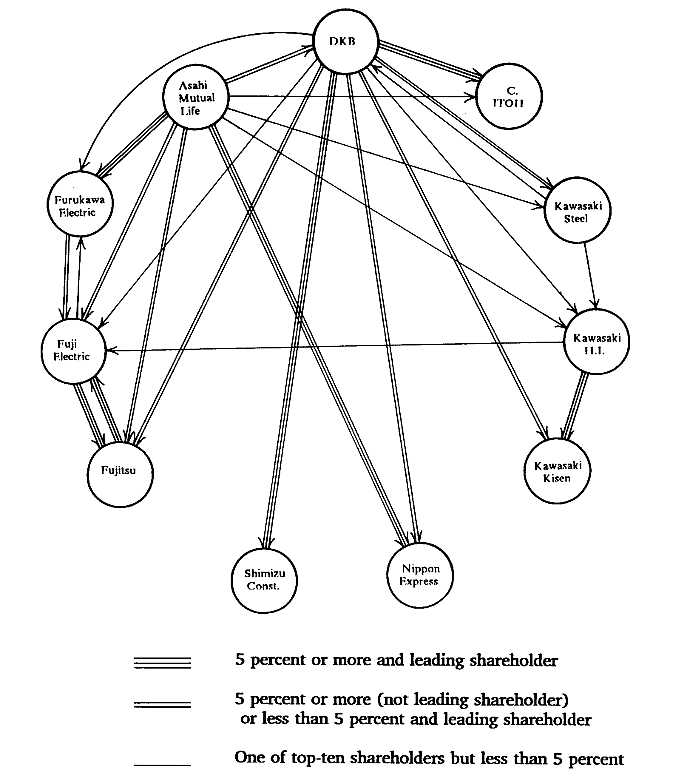

Fig. 4.4. Stock Crossholdings of the Leading Companies in the Dai-Ichi Kangyo

Bank Group. Source: Data from Industrial Groupings in Japan (1982).

Note: DKB = Dai-Ichi Kangyo Bank; H.I. = Heavy Industries.

group. The pattern that emerges for the Dai-Ichi Kangyo group is substantially different. Historical connections across the group as a whole have been largely through a single firm, Dai-Ichi Kangyo Bank. The current group is the amalgamation of several smaller groups that had associations with the former Dai-Ichi and Nippon Kangyo banks. Asahi Mutual Life, Furukawa Electric, Fuji Electric, and Fujitsu were all part of the smaller prewar Furukawa zaibatsu and maintain within the larger Dai-Ichi Kangyo group a subset of close relationships, with five of the six

possible connections completed. Among the three firms associated with the Kawasaki zaibatsu-Kawasaki Steel, Kawasaki Heavy Industries, and Kawasaki Shipping-two of the three possible connections are completed. Overall density of the group is 40 percent.[13]

The leading eleven companies[14] within the other two zaibatsu groups, Mitsubishi and Mitsui, have densities of 69 percent and 58 percent, respectively, while the density in the Fuji group is 49 percent and that in Sanwa 45 percent. These findings conform to popular accounts of the cohesion of the various groups. Sumitomo is widely viewed to be, along with Mitsubishi, the most cohesive of the groups. Conversely, the three bank groups are all viewed as more loosely organized than their zaibatsu counterparts.

Table 4.2 shows the transaction matrix for shareholding among the financial and industrial firms in our sample in 1986. Internalization to own-group firms among companies' top-ten shareholders is over 25 percent for all six keiretsu and over 50 percent in the three zaibatsu groups. Shareholdings across keiretsu, in contrast, are generally small or nonexistent. Among shares issued by Sumitomo group companies, for example, less than 3 percent are held by Mitsui, Mitsubishi, Fuji, or Dai-Ichi Kangyo group firms. Equity control is, to a large extent, located among shareholders in the same group. Not surprisingly, preferential transaction ratios are also high. In total, companies in the six groups are 12.8 times more likely to have their shares held by other firms in the same group, a figure nearly as high as for bank borrowings.

It appears from these results that the keiretsu continue to be a major source of both debt and equity capital for their affiliated firms. As recently as 1986, these data demonstrate, shacho -kai member firms and particularly those in the ex-zaibatsu rarely cross boundaries to establish major equity or borrowing positions with firms in other groupings.

Continuity and Change in Japanese Corporate Finance

Over the past two decades, capital market liberalization in Japan has made available financial instruments not previously available to corporate borrowers. Firms are now free to raise investment funds through a variety of equity, bond, and hybrid mechanisms, and in both domestic and overseas markets. Many large Japanese companies have taken advantage of these opportunities, and the result has been a substantial decline in the proportion of external corporate capital coming from traditional sources such as long-term debt.

Observers now talk about the "dis-intermediation" of Japanese capi-

TABLE 4.2. TRANSACTION MATRIX FOR | ||||||

Affiliation of Company Issuing Shares | ||||||

Affiliation | Mitsui | Mitsubishi (15) | Sumitomo (13) | Fuji | Sanwa | Dai-Ichi Kangyo Bank (22) |

Mitsui (15) | 51.4 | 2.3 | 2.1 | 0.7 | 4.4 | 5.3 |

Mitsubishi (15) | 1.6 | 63.4 | 0.9 | 4.0 | 4.7 | 4.4 |

Sumitomo (13) | 1.6 | 2.2 | 63.9 | 3.7 | 3.9 | 2.8 |

Fuji (17) | 0.0 | 1.5 | 2.2 | 38.1 | 4.8 | 4.4 |

Sanwa (19) | 10.1 | 8.8 | 9.1 | 11.1 | 28.0 | 10.2 |

Dai-Ichi Kangyo Bank (22) | 1.3 | 3.1 | 0.9 | 10.4 | 12.8 | 31.6 |

Other Cos. (137) | 33.7 | 19.0 | 21.0 | 34.7 | 42.4 | 42.0 |

Total | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

SOURCE: See Appendix A. Note: Figures represent percentages among the top-ten shareholders only. Number of sample companies is given in parentheses. Owing to rounding, columns may not add up to 100%. | ||||||

tal markets with the rise of "direct" (securities-based) financing. More colloquially, the phrase ginko banare is sometimes heard, implying the weaning of companies from their banks. The assumption is that these changes represent the elimination of the traditional role of financial institutions as conduits through which capital flows from household savers to corporate borrowers and the rise of more marketlike patterns of corporate finance. Just how extensive are these changes? And to what extent do they represent fundamental and long-term shifts in the underlying character of relationships between financial and nonfinancial corporations in Japan?

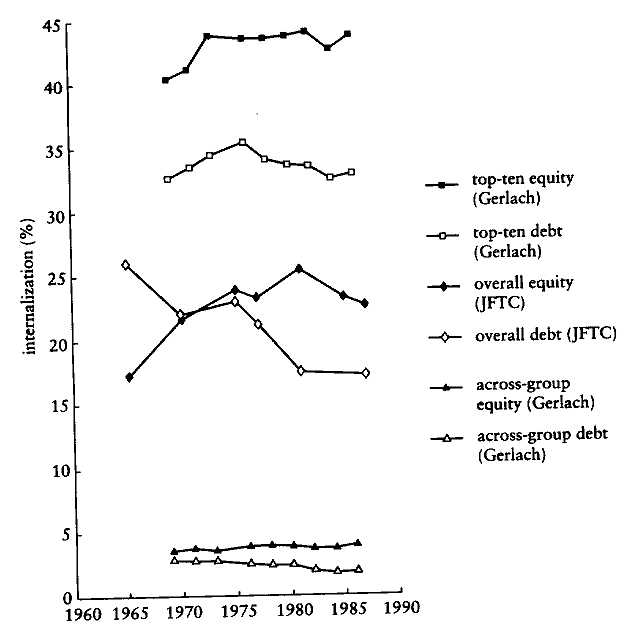

One way of measuring the effects of these changes is by looking at the relative share of external capital being provided by own-group financial institutions. Figure 4.5 shows time-lines for capital internalization among shacho -kai members based on data compiled by the Japan Federal Trade Commission and the data used in the present study. The JFTC studies have measured the extent of borrowing and shareholding since the late 1960s and show keiretsu relationships based on overall percentages of capital sourced within groups. The database used to compile the above figures is based on leading (top-ten) lenders and shareholders, and covers data from 1969 to 1986. Each of these sources, therefore, emphasizes somewhat different characteristics of the network. The JFTC data put financial sourcing in the context of firms' aggregate positions, and therefore include a large number of smaller lenders and shareholders. The database used for this study focuses only on major lending and shareholding positions (presumably those investors best able to form effective voting coalitions to influence corporate management) and has the advantage of including data on relationships across groupings.

Both measurement methods indicate that equity internalization is now substantially higher than debt internalization. The JFTC data report that this is part of a trend dating back at least to the mid-1960s. Since that time, firms have borrowed a declining share of their capital from financial institutions in their own group but relied on firms in their own group for an increasing proportion of equity capital. The two curves appear to have crossed sometime around 1970, the period at which our own sample data begin. The much higher internalization figures for both debt and equity in our sample when compared with the JFTC results reinforce the point that affiliated firms constitute a disproportionate share of leading capital positions. The percentages found in this sample also do not show a significant decline when compared with the 1970 period, nor do they indicate any increase in across-group

Fig. 4.5. Internalization of Debt and Equity over Time. Sources: Kosei Torihiki Iinkai survey data (various years);

for information on other data, see Appendix A. Note: Across-group figures are taken as a weighted average.

holdings during this period. Although the JFTC data suggest some decline in equity internalization since the early 1980s, the figures for 1988 are still higher than those fifteen years earlier.

These findings indicate that keiretsu affiliates continue to be an important source of external capital for Japanese firms. They also suggest that financial liberalization in Japan has not had the effect of increasing the proportion of external capital coming from financial institutions affiliated with other groups. What, then, is one to make of the changes occurring in Japan's financial structure?

The widespread view that Japanese corporate finance has moved from "indirect" to "direct" financing is based on the traditional perspective within financial economics that household savers channel capital to

corporations either directly, by entering the stock or bond market, or indirectly, by depositing it in banks that lend to companies. The reality in contemporary Japan is that even securities markets are mediated by large institutions linked through a complex set of strategic relationships with corporate users of capital. An actual revolution from indirect financing to direct financing would involve the discontinuation of the historically configured flow of money through indirect financing that tightly links corporations and financial institutions, and the advent of direct supply of savings (personal capital) to industry without passing through financial institutions.

That this has not been the case is evident in analyzing the actual pattern of the flow of funds rather than the mechanisms through which those funds travel. The ratio of individual shareholding in Japan has continued to decline and less than one-quarter of all shares in Japan are now held by individuals. Banks and insurance companies, in contrast, have continued to be net purchasers of securities (buying about 18 trillion shares and 16 trillion shares during the 1980s, respectively) and together now control nearly one-half of all publicly traded shares in Japan.[15] For this reason, when we examine the flow of capital through the Japanese economy, the vast majority continues to be mediated by financial institutions, as shown in Table 4.3. Although securities-based financing accounted for 44.2 percent of the total flow of funds through the corporate sector in 1987, all but a small fraction of this passed through financial institutions rather than being channeled directly from household savers or investment trusts into stocks and bonds. Together with credit-based financing that accounts for most of the remaining flow of funds, over 90 percent of total capital flows continue to be mediated by financial institutions into the late 1980s.

This gradual change in financing methods might have great significance if these financial institutions as purchasers of securities behaved quite differently than they do as financial lenders-for example, by becoming unstable stock market investors rather than stable lead banks. However, as empirical results in Chapter 3 demonstrated, equity ties among financial and nonfinancial companies continue to be structured in long-term relationships that reflect a complex set of strategic interests among the parties involved. These, therefore, continue to be administered rather than impersonal market transactions. Further indicating the continued role of keiretsu capital is the finding, reported in Figure 4.5, that the internalization of equity capital within the same group is now actually higher than for bank capital. Shifts toward equity capital

TABLE 4.3. "INDIRECT" FINANCING | |||

Flow of Funds | |||

"Indirect" Financing | |||

Year | Total | Securities | "Direct" |

1975 | 93.1% | 22.3% | 7.1% |

1980 | 86.1% | 25.9% | 8.5% |

1985 | 87.0% | 29.0% | 6.5% |

1987 | 90.7% | 37.5% | 6.7% |

SOURCE : Securities Market in Japan 1990, p. 3. Notes: "Indirect" financing refers to funds raised through financial institutions. "Direct" financing refers to funds raised through non-mediated securities investments, including those raised through invest-merit trusts. Foreign capital markets account for the remaining flow of funds in each year. These figures were -0.2% in 1975, 5.4% in 1980, 6.5% in 1985, and 2.6% in 1987. | |||

would therefore seem actually to be working toward one of the strengths of the intermarket groups.

This is not to say that the shift in the nature of capital financing is unimportant. With the decreasing proportion of total capital allocation channeled through the traditional prime rate system, the Ministry of Finance and the Bank of Japan are no longer able to exercise the same degree of control over financial markets that they once could. It is also true that, with the new reliance on securities-based finance, Japan's major securities companies are now more important in financial markets than in the past. Furthermore, even as banks and other financial institutions account for an increasing share of securities-based capital, the ability of highly profitable industrial firms to fund their investments through retained earnings has reduced their overall external capital dependency and shifted the balance of bargaining power with lending firms in their direction.

However, the overall effects of these changes on the internal cohesion of Japan's intermarket groups are not nearly as dramatic as they might at first appear. Even as they retire their own debt, large firms continue to rely on banks to provide loans for their affiliates. For example, Mit-

subishi Motors, which was spun off from Mitsubishi Heavy Industries in 1970 with the equity participation of Chrysler Motors, continues twenty years later to use the same financial institutions as its parent company. Among the top-ten lenders to Mitsubishi Heavy Industries, eight are also among Mitsubishi Motors' top-ten lenders, and both firms use the same main bank, Mitsubishi. Even for smaller companies, parent companies serve as an important source of bank capital by introducing and guaranteeing their bank borrowings. In an analysis of satellite firms affiliated with major electronics producers, for example, I found that 68 percent used the same main bank as their parent company (Gerlach, 1992b).

Japanese securities companies are themselves linked through long-term relationships with their industrial clients. Although not generally as closely identified with well-defined keiretsu as the city banks or as widely recognized, these affiliations are not unimportant. Among the Sumitomo group's twenty core companies, for example, all but four rely on Daiwa Securities as their lead underwriter as of 1989, and all but one of these companies has done so for the past two decades. Daiwa Securities is linked in turn into the Sumitomo group by virtue of the fact that its two leading shareholders and reference banks are Sumitomo Bank and Sumitomo Trust and Banking.[16]

In addition, the "securitization" of Japanese capital markets has actually been in the interests of Japan's commercial banks in at least one important respect. Since the mid-1980s, Japanese banks have been under new regulatory pressures, especially in order to meet BIS requirements for minimum capital ratios.[17] These requirements have forced the banks to raise new equity capital, and they have been among the most active participants in stock issues. During the six years from 1984 to 1990, Japan's twenty-three largest banks raised ¥13.5 trillion in equity capital, an amount that represented a substantial fraction of all new equity capital raised in Japan during this period (Wall Street Journal, March 18, 1991).[18] Moreover, the basic pattern of interlocking shareholding has continued, with nonfinancial firms utilizing approximately 30-40 percent of their own new capital to purchase bank equity issues and maintain their stable crossholdings (Nihon keizai shinbun, October 24, 1989). In this way, the demands for equity-based financing have served both nonfinancial and financial interests while limiting disruption to traditional ownership relationships.

In short, because of their central role as providers of both loan-based and securities-based capital, Japanese banks remain the main source of external capital for most major Japanese corporations. Even those firms

that have retired their debt and rely heavily on internal profits to fund investment activities continue to have these financial institutions as leading shareholders, granting them the attendant rights to vote shares and monitor management. Moreover, insofar as debt continues to be channeled to the affiliates of these corporations, the total dependency of vertical keiretsu chains of suppliers and distributors on these banks in most cases is still very high. Indeed, Japan's banks actually increased their loans in the 1980s at a rate that was higher than the growth rate of the economy as a whole, and by the end of the 1980s, most of the world's largest banks were Japanese.[19] This suggests a different interpretation of the changing nature of the keiretsu: what may be happening is not a breaking down of bank-led groupings so much as an expansion of these groupings across a broader spectrum of Japanese industry; their increasing organization within elaborate hierarchical structures around local centers of power (the parent companies); and their linking through securities-related instruments of finance and control.