Chapter IV

The Basic Form and Structure of the Keiretsu

Chi wa mizu yori koi

Blood is thicker than water

Onaji kama no meshi o kutta nakama

The group that eats from the same pot

Sayings used to describe

relationships within

the keiretsu

The fundamental organizational problem facing the contemporary keiretsu is that of creating a degree of coherence among its members in the absence of formal structures defining the roles and responsibilities of its participants and dear-cut purposes around which activities are to be focused. It exists not in the legal world as a formal organization (in the classical or Weberian sense) but in the social world of the business community as a loosely organized alliance.

It has nevertheless been able to express itself as a significant form of organization because of the ways it has structured interaction among its members and created an ongoing symbolic framework within which this interaction takes place. This chapter describes in detail three processes by which Japan's business groupings are organized collectively: (1) the creation of high-level executive councils that symbolically identify group members and the boundaries of social unit, as well as providing a forum for interaction among group firms; (2) the structuring of exchange networks-specifically, debt, equity, directorship, and trade networks- that define the position of individual firms in the group and establish group-wide constraints on behavior; and (3) the promotion of group-wide industrial and public relations projects that affirm the existence of the keiretsu as a coherent organizational form.

Of special interest is empirical data across a large number of firms in a

broad spectrum of Japanese industry indicating systematic and continuing patterns of preferential business relationships based on keiretsu affiliation. For all six major groups, the identity of business partners is shown to be a fundamental determinant of actual patterns of exchange. We furthermore find little evidence for the decline of preferential patterns during the 1970s and 1980s in the three capital market measures studied (debt, equity, and steel transactions). Not that Japan's alliance structures have been static: a number of important changes since the postwar period are discussed, including the shift from debt to equity financing and the declining role played by group trading companies as mediators of trade where assembly-intensive products are involved. But these are seen here as largely evolutionary rather than revolutionary transformations.

DEFINING MEMBERSHIP AND REPRESENTING GROUP INTERESTS: THE ROLE OF SHACHO-KAI

Among the most prominent features of the keiretsu is a layered set of personnel connections that serve as a conduit for information between companies and, occasionally, as a source of external discipline. Employee transfers are common among business partners, particularly among banks and their client firms and large manufacturers and their subcontractors. Group projects, discussed later in this chapter, are also important in bringing together personnel from middle and technical levels of several or more firms.[1]

In addition, firms in intermarket and vertical groupings are linked through a variety of intercorporate executive councils that serve as a forum for managers from different levels of the companies involved. The Sumitomo group, for example, has more than half a dozen different councils, including not only the group presidents' council but also an informal OB-kai ("old-boy" get-together) for its chairmen, which is oriented primarily toward playing golf, as well as a variety of regular meetings for directors, vice presidents, and bucho (division managers) for the purposes of discussing corporate planning, public relations, and other group-wide activities. Recently, each of the big-six intermarket groups has started its own kenkyu-kai (research councils) to help develop collectively the emerging information technologies. In the case of the Sumitomo group, two separate councils have been created, one for bucho -level executives and the other for kacho -level (department) managers.

While group interaction takes place at many levels, undoubtedly the

most prominent of these meetings are the presidents' councils that bring together the chief executive officers from the group's nucleus companies.[2] In Japanese, these are known as the shacho -kai, combining the word for company president, shacho , with the suffix -kai, for meeting, gathering, or association. The shacho -kai is a kind of informal community council, with membership limited to a set of core members.[3]

While the shacho -kai is typically viewed as a postwar phenomenon, it actually traces its beginnings to the prewar period and is a long-standing and widespread feature of interfirm relationships in Japan. The shacho -kai falls under a broader category of associations called in their most general form kyoryoku-kai, or cooperative councils. The kyoryoku-kai format is now found within even vertical alliances, bringing together the parent firm (Toyota, Hitachi, etc.) and its first-line subcontractors. The origins of the shacho -kai in the contemporary keiretsu may he traced to councils started by their zaibatsu counterparts.[4] In 1938 the Mitsubishi zaibatsu formed the Mitsubishi Kyoryoku-kai, establishing a forum for executives from the extended Mitsubishi group-the honsha and its first-line subsidiaries. Sumitomo followed this in 1944 with the Sumitomo Wartime Cooperative Council, or Sumitomo Senji Kyoryoku-kaigi (Okumura, 1983, p. 93).

These councils were dominated by the zaibatsu holding company as representative of zaibatsu family interests. The end of the second world war saw the dissolution of the honsha and the removal of its key executives, but not the abolition of personal connections among the executives in the former subsidiaries. As one chief executive in the Sumitomo group put it: "It was natural for me to feel kinship with [other group presidents]. We were all in the old Sumitomo zaibatsu together. After the war, after the zaibatsu was dissolved, we rose together in our separate corporations. But we kept in close touch. We have played baseball together, we've gone swimming together" (quoted in Business Week, March 31, 1975).

Informal meetings among these executives continued during the late 1940s (Okumura, 1983). Sometime in 1951, the meetings became organized on a more systematic basis among Sumitomo companies, resulting in formation of the Hakusui-kai, or White Water Club.[5] In its first meeting, all eleven first-line companies in the old Sumitomo zaibatsu participated. Several years later, companies related to the former Mitsubishi zaibatsu formed their own council. Its chairmen and presidents met on the second Friday of the month, leading to the title of Kinyo-kai, or Friday Club.

The other four groups all began their own shacho -kai in the 1960s,

taking their lead from the example set by Sumitomo and Mitsubishi. Mitsui, which had been slower than the Sumitomo or Mitsubishi zaibatsu to reform after the war, began a council in 1961 that met on the second Thursday of every month, calling it the Nimoku-kai, or Second Thursday Club. The inchoate bank groups also adopted the shacho -kai format and two followed the Mitsubishi and Mitsui idea of naming it after the day on which the executives met. In the mid-1960s the Fuji and Sanwa groups announced the formation of, respectively, Fuyo-kai (taken from an old group name) and Sansui-kai (Third Wednesday Club). The last group to formalize a council was Dai-Ichi Kangyo, which in 1978 formed the Sankin-kai (Third Friday Club), seven years after the merger of the Dai-Ichi and Nippon Kangyo Banks. The Sankin-kai brought together three councils that had existed under the old banks: the Kawa-saki Mutsumi-kai and Furukawa Sansui-kai, both dating from the mid-1950s under the umbrella of the old Dai-Ichi Bank, and the Jugosha Shacho -kai, begun in 1970 under the old Nippon Kangyo Bank.

From the informality of the early postwar period-a necessity, perhaps, given the strong anti-zaibatsu feelings among economic reformers at the time-the shacho -kai has become an institutionalized feature of the keiretsu. The roster of their participants is released to the public, and some groups now even permit the registration of alternate representatives from member companies if a company's president is unable to attend. As we see below, and later in Chapter 7, the shacho -kai in some ways serves as a functional equivalent for a U.S.-style board of directors by bringing together key external constituencies through regular meetings, though with several distinctive features.

The Basic Format of the Shacho -kai

Presidents' council meetings are held on a monthly basis (or, in the case of the Dai-Ichi Kangyo group, once every three months). In addition to a chairman-a position that rotates every meeting in some groups and is fixed in others-the meetings typically also assign a secretary, whose function is to record the proceedings. These records are not, however, made available to the public, nor are they transmitted formally within the firms. For this reason, information about the internal contents of the meetings and their dynamics is by necessity second-hand and inferential. What follows comes from interviews with a number of executives involved in group councils, both at the shacho -kai and at lower levels. I have also used accounts gleaned from various press reports.[6]

It appears that the shacho -kai in practice is less a command center to determine the policies and practices of individual companies than a forum for the discussion of matters of mutual concern. It simultaneously (1) establishes an identity for the group and its participants, signifying relationships among firms, and instilling a sense of coherence; (2) creates a setting in which issues of group-wide concern may be negotiated, including protecting and promoting the group name and, less often, arranging for assistance for companies in trouble, resolving conflicts among members, or disciplining deviant group companies; and (3) enhances the group's position in the larger business community by presenting the image of a powerful and historically prestigious collective.

More often than not, the executives remarked, nothing of particular note is discussed and the meeting is merely an opportunity to exchange views with other chief executives and to socialize. (Even in Japan, it appears, it is lonely at the top.) Often the meetings revolve around a theme-say, "Information in the Twenty-first Century"-and a guest speaker is invited to address the assembly, providing a basic focus for discussion. Companies often report on new products and technologies that they are developing, decisions to open new subsidiaries in foreign markets, and general conditions in their own industry. Periodically, special matters of group-wide interest come up, including projects that the group is engaged in as well as various charitable activities. Infrequently, topics arise that require special attention-intramural conflicts or group companies that are having financial difficulties. The atmosphere, as it was described to me, is one of camaraderie rather than of a formal meeting with a defined agenda. Nevertheless, the shacho -kai is considerably more than a quaint business custom, for it serves both to signify membership in the group and to provide a common arena for the expression of the strategic interests group firms have in one another. As such, it is significant both for its symbolism and for what it reveals about the dynamics of keiretsu membership.

Externally, the shacho -kai serves as a signal to the larger business community that a relationship exists. This confers on the member company a degree of status resulting from being associated with the name of Mitsubishi, Sumitomo, and so on. How much status depends on the position of the group itself, leading to various forms of intergroup competition for prestige. From the 1950s until the 1970s, Mitsubishi was held as probably the most prestigious group with which to be affiliated, as it was perceived as the most powerful, progressive, and cohesive. More recently, the Sumitomo group has taken the lead in the

prestige rankings, leading to talk in the Japanese business press of a "Sumitomo Boom" (Shukan asahi, April 5, 1985). Though smaller than Mitsubishi, Sumitomo has been growing faster and has several members at the leading edge of high technology-particularly NEC in computers and telecommunications and Sumitomo Electric in optical fibers and compound semiconductors. Council membership also sends signals that get picked up by managers in the purchasing and finance departments of their respective companies, tilting decisions in favor of other group firms when there are no compelling reasons to go elsewhere. As we shall see below, membership is closely associated with patterns of banking, trade, and other business relationships involving group companies.

The Shacho -kai as Political Arena

Behind the shacho-kai's passive and harmonious external surface, companies and their representatives compete with one another on a subtly curtained stage. The Japanese are fond of pointing out the duality of social relationships residing in the tatemae, the pleasant exterior constructed to maintain ongoing social relationships, and the honne , the darker, emotion-laden reality that lurks inside. That the honne is so rarely openly expressed in the shacho -kai is a reflection of the effectiveness of the structures of constraint on individual firm action, as well as the importance to the group of maintaining a useful front of coherence with which to compete with other groups. The power the council maintains is implicit rather than formalized into statutes governable by laws and stems to an important degree from the embeddedness of firms in group-wide exchange networks, discussed below. Because of the high degree of ambiguity in the precise roles and functions of the shacho -kai, influence is a continually negotiated process, determined through the interaction of the characteristics of the individuals attending and of the positions of their firms in the group.

Among the characteristics of powerful leaders, the two that stand out are seniority and personality. Several informants mentioned that presidents who had been in their positions longer were likely to have more influence over group decisions. This seems to reflect the senpai-kohai relationship that pervades social relationships in Japan-that those who have been in a position longer are deferred to by virtue of this fact.[7] Personality is also a factor that was mentioned frequently. Charismatic leadership by the long-standing president of Sumitomo Bank in the 1950s and 1960s was widely credited for bringing the Sumitomo group

together at that time, while a change in leadership at Sanwa Bank in the 1960s also led to a new strategy of group consolidation. Similarly, the lack of this kind of leadership in the Mitsui group was cited in explaining the slower process of Mitsui consolidation.

Power derived from personal attributes, however, is set within the context of the company's position in the group. The tenure of companies is a factor, particularly in the older ex-zaibatsu where associations with the group's past confer an honored position on some firms. In the Sumitomo group, this is particularly true of Sumitomo Metal Mining, the descendant of a three-hundred-year-old copper mining operation that was for two centuries the life-blood of Sumitomo operations. Several managers from other Sumitomo companies talked about the "special feeling" they had for Metal Mining, a feeling born from its historical significance. Sumitomo Corporation, in contrast, although the largest nonfinancial company in the group when measured by sales, was formed after the war through the efforts of other core companies in the group and has not fully risen above its image of a company formed out of (and therefore under) another.

However, most important in determining power within the group is position in its constituent exchange networks. The two firms most likely to have significant linkages with all keiretsu companies are the group bank and the group trading company. These constitute the network "bridges" (Granovetter, 1973), with common connections to all group members through their control over capital and intermediate product markets. These same two firms, and particularly the bank, have been the most active in reorganizing the keiretsu during the postwar period and are widely considered to be the most central group members. Manufacturing concerns, in contrast, have been more likely to try to maintain a degree of independence. The resulting internal dynamics of the group reflect a balancing of the competing interests for group-level control and company-level independence. In the words of one executive, "The keiretsu have to move both centripetally and centrifugally. While holding together, they have to expand their outside ties (gaibu to no kankei ). Too strong a push for control by the group bank and the delicate balance of power in the group is threatened."

There has been some discussion in recent years of the waning power in the group of banks and trading companies, as industrial companies have developed their own sources of capital and trading networks. In part, this reflects the increasing size of the groups and the dispersal of share-holdings across a larger number of companies-though the network

analyses below raise doubts that these changes are as striking as they are sometimes presented. More important in the shifting balance of power, however, has been the changing positions of companies in the larger business community. The restructuring of Japanese industry away from heavy industries toward high technology industries has also altered roles within the groups. Several informants noted, for example, the rising status of NEC (involved in the computers and communications industries) within Sumitomo.

The interaction of personalities and company positions over time has led to some variation in the dynamics of the different councils. Mitsubishi's Kinyo-kai is perhaps the most formalized and centralized of the councils. Its chairmanship has traditionally rotated among Mitsubishi's leading firms, which constitute the core group's inner circle, known as the Sewanin-kai (mediator's club). First among equals, however, has been the group bank. In a nice quote that simultaneously captures his leadership position and its symbolic manifestation, a president of Mitsubishi Bank in the 1970s, Wataru Tajitsu, described his position as the Kinyo-kai chief as follows: "My role is akin to that of a Shinto priest. I take on any and all squabbles and problems within the group and pronounce a benediction. If that does not do the trick, I draw my sword . . . unfortunately with a blade of bamboo and not steel" (Oriental Economist, May 1974).

If Mitsubishi is the most centralized council, then Sumitomo's Hakusui-kai is perhaps the most decentralized. There is no formal position of leadership. Rather, the chairmanship of each meeting rotates regularly among the presidents of all twenty companies. Since there is no assigned seating arrangement, attendees try to come early to get the best seats. It is also the most restrictive of the councils, as attendance is limited to the company presidents, and neither company chairmen (a largely honorary position in Japan) nor proxy representatives are allowed.[8] The president of Sumitomo Bank, Isoda Ichiro , reported on the internal dynamics of the Hakusui-kai a number of years ago as follows:

There are no specific representatives to the Hakusui-kai, it is true. At the beginning, I used to sit at the center of the table but I stopped this practice after six months or so. As seats start to fill from the comers, you have to sit in the center when you join the group late. So I make it a practice to go to the meetings rather early and take a corner seat. . .. In times of real crisis, leadership will naturally emerge on its own on the basis of the ages of the presidents represented and the history, real prowess, and social positions, etc. of the corporations involved. [Oriental Economist, May 1981.]

The Mitsukoshi Incident

The vaguely defined but widely acknowledged role of enterprise groupings and their leadership councils is evident in the "Mitsukoshi Incident," an event that took place in 1982 and received extensive publicity within the Japanese business community. Mitsukoshi is a venerable institution-the largest, oldest (founded in the seventeenth century), and most prestigious of Japan's remarkable department stores. But from the late 1970s until the incident reached its finale, Mitsukoshi was rocked by a series of scandals, including an investigation by the Japan Federal Trade Commission into allegations of illegal sales pressure exerted by Mitsukoshi on its suppliers.

These problems became more serious in the early 1980s when inventories of unsold items began to pile up in Mitsukoshi's warehouses, and it turned out that much of this excess inventory had been sold to the department store through companies with questionable ties to its president, Okada Shigeru. Okada had long been romantically involved with Takehisa Michi, the proprietress of a group of firms that imported and distributed foreign-made products. This special relationship had helped Takehisa to expand sales to the department store, and her companies were enjoying large profits even at a time when the department store's sales and profits were weak. Takehisa's influence within Mitsukoshi through her association with Okada reached a point where she was sometimes referred to as the empress (jotei ) of Mitsukoshi. Her "reign" resulted in bad press for Mitsukoshi and substantial disruption in the ranks. It was widely believed that the directors had not reported to Okada the extent of the inventory problem for fear of the consequences if they crossed Takehisa.

The final stage in Okada's undoing came in August, 1982, when Mitsukoshi put on an exhibition of Persian antiques in its gallery, selling a number of them at very high prices to wealthy customers. This is a common practice among leading department stores, but it was discovered shortly thereafter that some of these "antiques" were in fact fakes that had been manufactured no further away than the suburbs of Tokyo. Exacerbating the problem was Okada's refusal to resign to take blame for this problem. Under normal circumstances, a blossoming scandal of this magnitude is dealt with under Japanese business etiquette by the resignation of the CEO and by a round of public apologies by various company officials to those affected and to the general public.[9] But Okada denied any association with wrongdoing and continued in his

position as president. This presented the board of directors of Mitsukoshi with a delicate problem, since nearly all members were full-time employees of Mitsukoshi who worked under Okada, the very man they were in a position to have to remove.

As a member of the Mitsui group, however, Mitsukoshi had longstanding associations with other group companies, and particularly with Mitsui's financial institutions, a number of which were among Mitsukoshi's leading shareholders. While Mitsukoshi continued to decline in the public eye, the latent power of the group became increasingly apparent. Rumors began to circulate that group companies would refuse to buy gifts during the year-end gift-giving season in Japan, a major source of revenue for Japanese department stores. A senior member of the group, Edo Hideo, who was also chairman of Mitsui Real Estate, was quoted at the time as saying, "We can no longer stay clear of the situation. . .. [T]his is smearing mud on the history of Mitsui" (Shukan asahi, September 24, 1982). The scandal was coming to affect Mitsui's own good name (as well, not incidentally, as its companies' financial positions in Mitsukoshi).

The Mitsui group's interests were expressed through Koyama Goro, a retired chief executive of Mitsui Bank who sat on Mitsukoshi's board. As a former leader in Mitsui's presidents' council, the Nimoku-kai, and as an advisor to the bank, Koyama's support was considered critical because of his high position and influence within the Mitsui group. Several top executives and corporate auditors approached Koyama to see whether he would provide external support for the removal of Okada at a forthcoming board meeting. Before the meeting, Koyama arranged to meet with Okada to confront him directly with Mitsukoshi's problems. On September 7, Koyama arrived at Okada's office. According to several accounts, the meeting was a disaster, as Okada accused Koyama of meddling in affairs that were none of his business (Shukan asahi, October 8, 1982; Yomiuri nenkan, 1983).

At this point, there was no turning back. Okada's behavior entered the agenda of the group's Nimoku-kai, where it was decided that Okada would have to be eased from power. Mitsukoshi's board meeting took place on the morning of September 22. After other items of business were completed, a senior executive on the board took the floor and proposed the dismissal of Okada as president. With the exception of Okada, all directors on the board, each of whom had been carefully solicited before the meeting, stood up in support of the proposal. Okada cried out, "What for!", to which Koyama responded, "Since you're the one on the agenda, you have no right to speak." Even after the board

meeting was finished, Okada remained in the conference room beseeching other directors to reconsider. But Koyama had the last word, coolly informing Okada, "The meeting's over. . .." (Shukan asahi, October 8, 1982; Yomiuri nenkan, 1983). Thus ended what was reported in the Japanese press to be the first time a chief executive had been forced out of office by his own board of directors.

THE STRUCTURE OF INTERCORPORATE NETWORKS

If the shacho -kai serves to define membership and express group interests, then flows of resources are the concrete manifestations of these interests in the ongoing life of each firm's interactions with its affiliated enterprises. In the structure of these flows we find clear indications of the significance of the keiretsu in organizing intercorporate exchange in Japan. Ostensibly bilateral linkages are themselves organized into alliance networks of varying densities. These represent collective structures, both in the ways in which transactions signify relationships (e.g., establishing trading relationships by taking an equity position), and in the creation of exchange networks whose overall structures become important determinants of relationships within the keiretsu.

In the following sections, we look at the patterns of interfirm exchange networks established through (1) loans from group financial institution, (2) share crossholdings, (3) outside directorships, and (4) trade in intermediate products. Within the group, these exchanges are closely intertwined with other ongoing relationships among group members. Each apparently discrete transaction (e.g., one firm's equity position in another) is itself embedded in a joint social construction-the group.

The analyses below rely on the following measures of network structure. The first is density, defined by Mitchell (1969) as the proportion of linkages completed in a network as against the number of total potential linkages. More useful for determining the extent of preferential trading is the transaction matrix. This matrix provides a detailed breakdown of the share of ties by both sending and receiving firms according to alliance affiliation. Through the device of the transaction matrix and a set of related network measures, we are able to demonstrate relatively precisely the extent to which nominal classifications of groupings determine concrete patterns of intercorporate linkages. In so doing, we also demonstrate just how far Japanese business networks deviate from hypothetical market anonymity.

The transaction matrix yields two derivative measures of substantive

interest. One of these is internalization, defined here as the proportion of alliance firms' total (or top-ten) interfirm linkages that take place with firms in their own keiretsu. The other is the preferential transaction ratio, an index of the exclusiveness of each group. The preferential transaction ratio is calculated as the proportion of ties that take place among firms within the same keiretsu divided by the average number of ties these firms have with other major keiretsu. Where internalization puts the group in the perspective of the entire business network (including independent and subsidiary firms that maintain no formal group affiliation), the preferential transaction ratio assesses the importance of each alliance only against other keiretsu. Complete neutrality in dealings with other companies results in ratios of 1 : 1, while deviations from this are interpreted as preferential patterns in the network. The stronger the patterns, the farther these intercorporate relations are deviating from pure market anonymity.

JAPAN'S FINANCIAL SYSTEM

In studying the significance of the keiretsu in structuring Japanese capital markets, it is essential to consider the distinctive patterns of corporate finance as they have evolved over time in Japan. The central role during the prewar period in capital allocation among zaibatsu subsidiaries was played by the holding company. During the postwar period, with the dissolution of the holding companies, this role was largely taken over by financial institutions and especially by large city banks as major lenders of capital. This created the conditions in the critical wartime and early postwar period within which more extended alliances organized around lead banks emerged. More recently, as a result of capital market liberalization and a slowing in the overall growth of the Japanese economy, there has been a proportional shift in the sources of external capital among large Japanese companies away from long-term debt toward equity and bond financing.

Despite these changes, certain underlying characteristics of Japanese capital market relationships have continued since the postwar period into the present day in modified form. These include the fundamental importance of large financial institutions in mediating between household savers and corporate users of capital; capital allocation through closely administered ties between these financial institutions and their industrial clients, even where financing takes the form of securities-based capital; and strong preferential patterns of capital supply in both debt

and equity capital markets among affiliated enterprises. As a result, when the position of banking, insurance, and securities companies are considered as a whole, we find far less change in the capital allocation process than is often believed.

The Historical Role of Financial Institutions

The financial function was already well developed in the Tokugawa economy with the large merchants playing an especially important role. Modern banking and life insurance companies, however, were not introduced until the 1870s, as an import from the West. The Japanese government encouraged the banking system in various ways but left the actual role of financing Meiji development largely to private financial institutions. These banks, particularly the large-scale city banks, emerged in dose conjunction with the development of manufacturing operations and never achieved the independent status that they did in the United States. Each inchoate zaibatsu of the Meiji period started its own bank for the purpose of funding the activities of its group companies. As Lockwood (1968, p. 222) points out,

Big banks and trust companies were securely tied into each major combine by intercorporate stockholding, interlocking directorates, and the "interrelated solvency" of these institutions and their combine affiliates. They held the deposits of affiliated companies (as well as individual depositors) and were at the same time their chief source of capital.

Those banks that had begun independently, such as Dai-Ichi Kokuritsu Bank (the forerunner of the contemporary Dai-Ichi Kangyo Bank), found it necessary to develop close relationships with a subset of dependable client firms that relied on them for the bulk of their external capital needs. Even the smaller, specialized zaibatsu (e.g., Nissan) developed their own internal financial arms for the same purposes. This supporting role is evidenced in the term that described them- kikan ginko , or "organ banks." Less often, the reverse pattern occurred, with entrepreneurs focusing primarily on developing financial enterprises and later extending these to the building of industrial empires. The Yasuda zaibatsu was representative of this pattern.

In the 1930s, as the Japanese economy was rapidly expanding to meet Japan's wartime needs, banks increasingly replaced the honsha and the zaibatsu families as the main sources of working capital for the group companies. Since banks were not prohibited from holding equity, they

became significant shareholders in their client firms, increasing their share of all nongovernment securities from about one-fifth to about one-half between 1930 and 1945. Banks also provided, through loans, over half of Japanese companies' total external capital. In total, four-fifths of all debt financing and two-fifths of all external corporate funds came from banks during this period (Goldsmith, 1983).

The close connections between financial institutions and their clients that have dominated the Japanese postwar period were, therefore, already well in place by the end of the war. This was reinforced when banks managed to escape postwar dissolution and benefited further by the freezing of bank deposits held by the zaibatsu families, releasing the banks' deposit liabilities. Industrial firms themselves were growing rapidly and had extremely high external capital requirements that could not be met by the relatively undeveloped equity market, so they turned increasingly to the banks. The postwar period was marked by a dramatic increase in reliance on bank borrowing, with stock financing declining from two-fifths of total funds in 1934-36 to less than one-tenth in 1945-53, and loans and discounts increasing from less than one-tenth in 1934-36 to considerably over one-half in 1946-53 (Goldsmith, 1983, pp. 142-43).

During much of the postwar period, relationships among the government, banks, and large corporations have been maintained through a kind of administered interdependence (Suzuki, 1980). Since capital was in chronic short supply, the government was able to ration credit among preferred institutions. Government-bank ties were reinforced through the practice of "overloans," in which banks themselves borrowed heavily from the government Bank of Japan in order to gain access to capital, which was then lent to large firms. Out of this emerged "window guidance"-moral suasion over amounts loaned by the banks to the banks' customers resulting from the Bank of Japan's position of power. The capital shortage naturally shaped banks' relationships with their corporate clients, as firms interested in expanding were forced to maintain tight business relationships with their banks by "overborrowing"-that is, borrowing beyond the company's current needs and depositing the surplus in the banks as a kind of side payment known as "compensating balances." Although financial deregulation in the 1970s and 1980s has changed these relationships in certain respects, as discussed below, this long period of interaction has institutionalized a general pattern of cooperation among capital suppliers and large corporate capital users that has remained in modified form to the present day.

The importance of large financial institutions has come not only in providing capital but also in looking out for the wide range of business interests of their industrial clients. Japanese businessmen put great emphasis on the main bank relationship. Status as the number one lending institution for a company carries with it the expectation that the bank will not only provide a significant portion of the firm's capital but will also look after its interests in a variety of ways. The main bank sends a signal to other banks about the financial health of the company, a role that Horiuchi, Packer, and Fukuda (1988) have termed a "delegated monitor" function. The main bank also ensures that the company is able to gain loans from other banks as well-a process known as "pump priming," or yobi-mizu. In 1975, for example, the Sumitomo Bank and the Mitsubishi Bank agreed to extend loans of ¥2 billion (somewhat over $5 million at the time) to the largest manufacturing companies in the other's group, Mitsubishi Heavy Industries and Sumitomo Metal Industries, on a mutual basis. This was reported to be a way to circumvent regulations enacted by the Ministry of Finance the previous year placing limits on the amounts banks were able to lend to a single customer (Okumura, 1983).

Bank assistance extends as well to helping its clients find business customers. A Sumitomo Bank executive explained as follows: "Sumitomo Metal Industries does a lucrative business now selling sheet steel to the Matsushita companies, the Nissan companies, and Toyo Kogyo, among others. They enjoy this business because the bank provided a large part of the financing for these companies and acted as go-between to get this business for them. There are many, many arrangements such as this in the group" (quoted in Business Week, March 31, 1975).

Where the company does get involved in financial problems, the main bank is expected to come to its client's rescue. An example of this was provided by a manager formerly affiliated with Akai Electric, a major video and audio tape-deck manufacturer. Akai had during the early 1980s run into financial difficulties and was under financial reconstruction with bank support. It was Akai's main bank that took the lead in its reconstruction. This was Mitsubishi Bank, which owned 8 percent of Akai's shares and was the lender of 16 percent of its borrowed capital. As part of the assistance, Mitsubishi sent three people to Akai-the chief secretary to the president, the department manager in charge of international business operations, and the department manager for international finance-as well as extending additional loans to the company.[10]

In addition to their role as lenders, Japanese banks also maintain an additional source of influence over their client companies not enjoyed by U.S. commercial banks: the ability to take equity positions in other companies on their own account. Unlike banks in the United States, which are restricted by provisions of the Glass-Steagall Act, Japanese banks typically maintain holdings of several percent of most of their main client companies' stock.[11] The fact that banks have been able to both lend capital and hold equity positions has reinforced their central positions in Japanese capital markets, and they have aggressively expanded their client base while promoting internal coordination through joint councils and projects.

The capital market relationship is reciprocated from company to bank, as firms maintain a significant portion of their own capital in their banks in the form of deposits and equity shareholdings. Hamada and Horiuchi (1987) report that Japanese nonfinancial corporations held over 30 percent of their financial assets in the form of bank deposits during the period studied, 1954-83. Companies furthermore typically hold shares of the banks that lend to them, which they are able to use as collateral on their loans. The relationship between bank and client company extends even to employee accounts, as corporate customers often have employee wages automatically transferred to an account opened for each employee with the bank in lieu of cash payments. This practice has intensified recently with the emergence of firm banking- electronic data transmission systems between banks and their client firms.

As a result of these intertwined forces, there emerged during the postwar period what one set of observers aptly term a kind of "banking-industrial complex" in Japan, with transactions in capital taking place largely through close and longstanding business associations between banks and their clients rather than through impersonal capital markets: "At the risk of oversimplification, we may characterize the American financial system as a market-oriented system. The Japanese system had more administrative or organizational aspects to its capital allocation mechanism, and in some cases the line of demarcation between 'the company' and 'the market' was rather blurred" (Flaherty and Itami, 1984, p. 158).

Capital Markets and the Keiretsu

The maintenance of the central position of the group banks was ensured by the postwar economic reforms pushed by the U.S. occupation, which

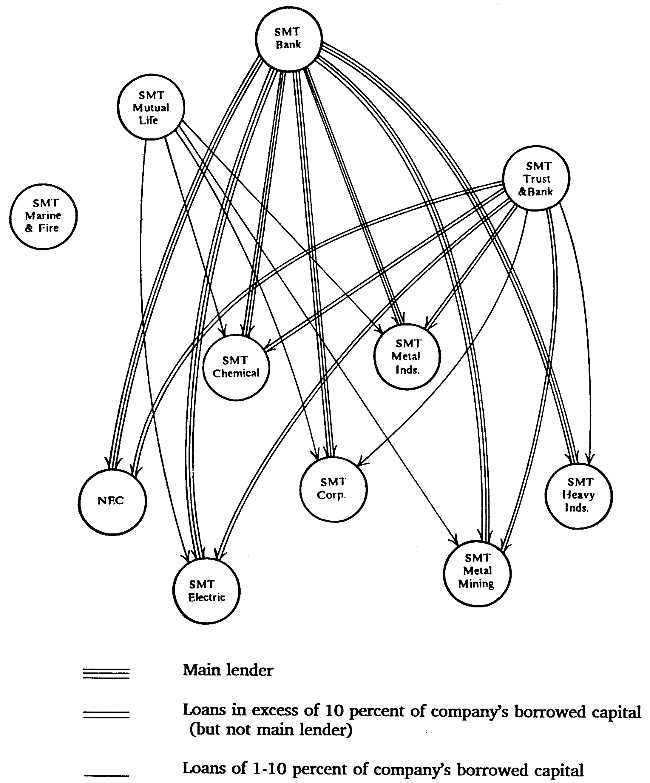

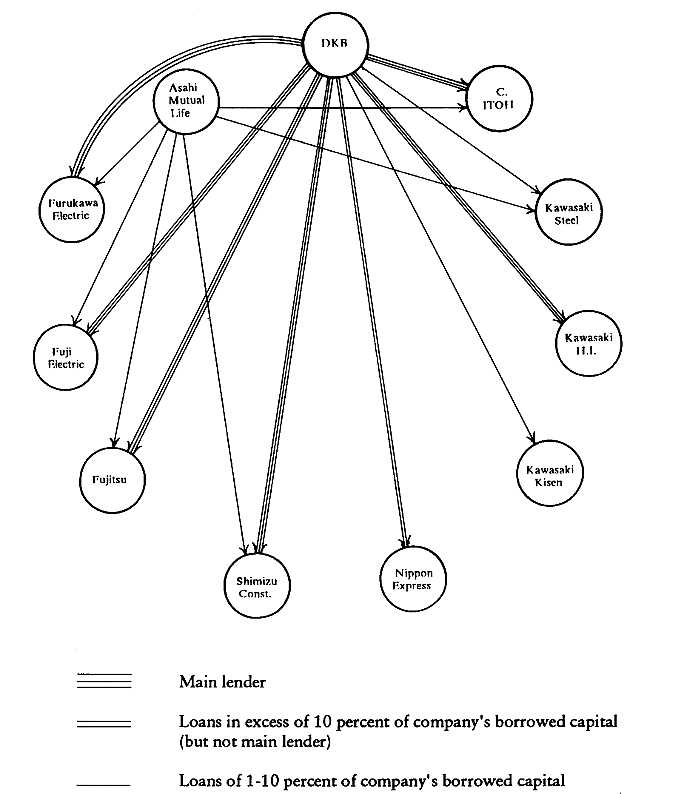

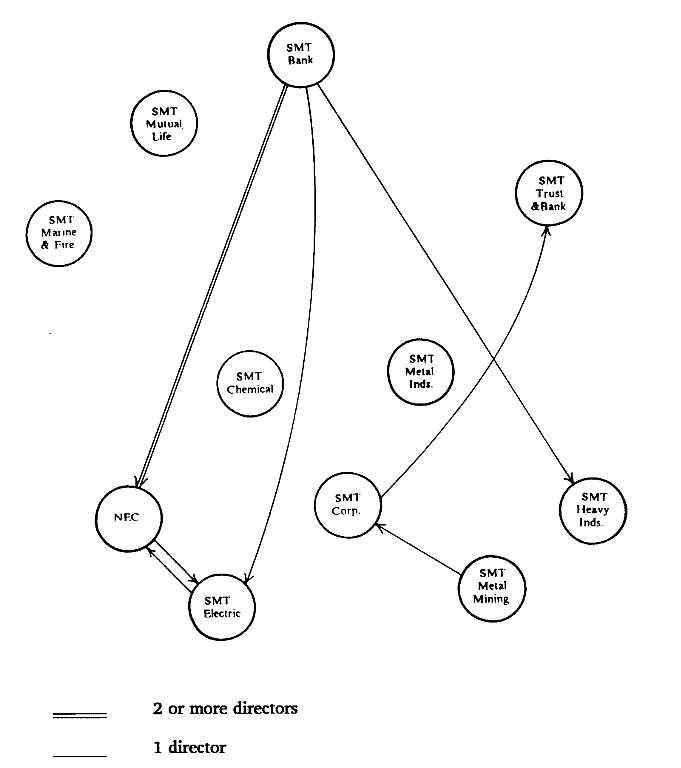

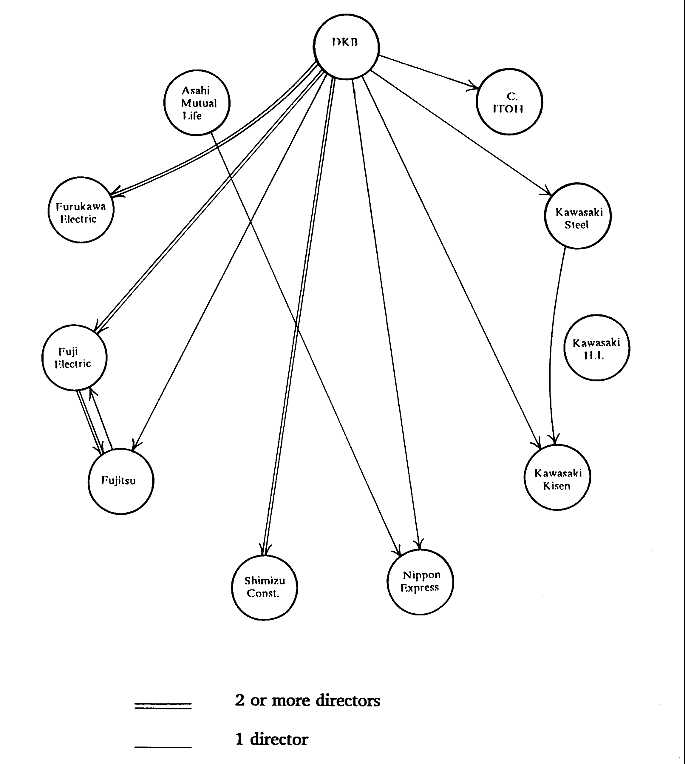

broke up the zaibatsu holding companies but not the zaibatsu banks. As a result and in conjunction with the Japanese government's policy of allocating scarce capital to the city banks through its own financial organs, these city banks reinforced their importance as the leading sources of capital for group companies and were in a position to give preference to their own long-standing clients. Groupings formed around these banks as companies were willing to forego a degree of independence in order to gain access to scarce-but-needed capital, particularly during the economic resurgence in the mid-1950s. Today we find that the large city banks associated with the six big intermarket keiretsu are the main banks for virtually all of their group companies, while other group financial institutions play an important secondary position. Figures 4.1 and 4.2 depict these relationships for the leading companies in two groups, Sumitomo and Dai-Ichi Kangyo Bank.

While the existence of close banking relationships is readily apparent in these figures, it is possible that strong banking ties exist among keiretsu firms and financial institutions in other groups as well. In order to evaluate this possibility, a transaction matrix was created for the two hundred industrial firms in our sample, based on the percentage of capital coming from firms' top-ten lenders broken down by group affiliation. These results are reported in Table 4.1 for the year 1986.

The boldface figures along the diagonal show the extent of internalization of borrowed capital to financial institutions in the same group. As we see here, intra-group capital proportions range from a low of 23.3 percent for Dai-Ichi Kangyo industrial firms to a high of 42.8 percent for Mitsubishi firms and 42.4 percent for Sumitomo firms. Most of the remaining debt capital for each group firm comes from "independent" financial institutions-an amalgamation of smaller commercial banks and insurance companies, as well as long-term credit banks. Capital linkages to financial institutions in other keiretsu account for a much smaller share of the total in each group. No single group is the source of more than 10 percent of the total capital borrowed by any other group, and in the case of Sumitomo group borrowing, the figure is zero in three cells (i.e., none of these ten companies count a Fuji-, Sanwa-, or Dai-Ichi Kangyo-affiliated financial institution among its top-ten creditors). It becomes quickly apparent from the transaction matrix that the hypothesis of substantial across-group ties in the loaned capital market does not hold for the shacho -kai firms in the sample.

The extent of bias toward affiliated financial institutions can be understood through a simple derivative measure, the preferential transaction ratio. This is calculated by dividing the share of same-group transactions

Fig. 4.1. Intragroup Borrowing Dependency of the Leading Companies in the

Sumitomo Group. Source: Data from Industrial Groupings in Japan (1982). Note: SMT = Sumitomo.

by the average for those in each of the other five groups. While internalization points to the absolute proportion of borrowing coming from one's own group, the preferential transaction ratio looks specifically at intra- versus intergroup relationships and the possibility not only that firms prefer to borrow from their own group but also that they prefer to use banks outside the other keiretsu (e.g., the Industrial Bank of Japan)

Fig. 4.2. Intragroup Borrowing Dependency of the Leading Companies in the Dai-Ichi

Kangyo Bank Group. Source: Data from Industrial Groupings in Japan (1982).

Note: DKB = Dai-Ichi Kangyo Bank; H.I. = Heavy Industries.

for their nongroup capital. In total, firms in the six big keiretsu are about 15.1 times more likely to borrow capital from financial institutions in their own group than from those in another group. What this ratio makes clear is that the identity of keiretsu affiliation is itself important in defining patterns of transactions.

Next we consider the role of the keiretsu in organizing Japanese

TABLE 4.1. TRANSACTION MATRIX FOR | ||||||

Affiliation of Industrial Borrower | ||||||

Affiliation | Mitsui | Mitsubishi | Sumitomo | Fuji | Sanwa | Dai-Ichi Kangyo Bank |

Mitsui (3) | 39.5 | 1.9 | 1.0 | 1.8 | 2.5 | 7.1 |

Mitsubishi (3) | 1.0 | 42.8 | 2.9 | 4.3 | 4.8 | 4.5 |

Sumitomo (3) | 3.0 | 3.5 | 42.4 | 5.3 | 1.6 | 4.2 |

Fuji (4) | 0.5 | 0.7 | 0.0 | 26.6 | 8.9 | 3.2 |

Sanwa (2) | 1.0 | 0.5 | 0.0 | 30.0 | 32.2 | 6.8 |

Dai-Ichi Kangyo Bank (2) | 5.8 | 4.0 | 0.0 | 8.1 | 4.9 | 23.3 |

Other Banks (29) | 49.2 | 46.5 | 53.8 | 51.0 | 45.0 | 50.9 |

Total | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

SOURCE : See Appendix A. Note: Figures represent percentages among the top-ten lenders only. Number of sample companies is given in parentheses. Owing to rounding, columns may not add up to 100%. | ||||||

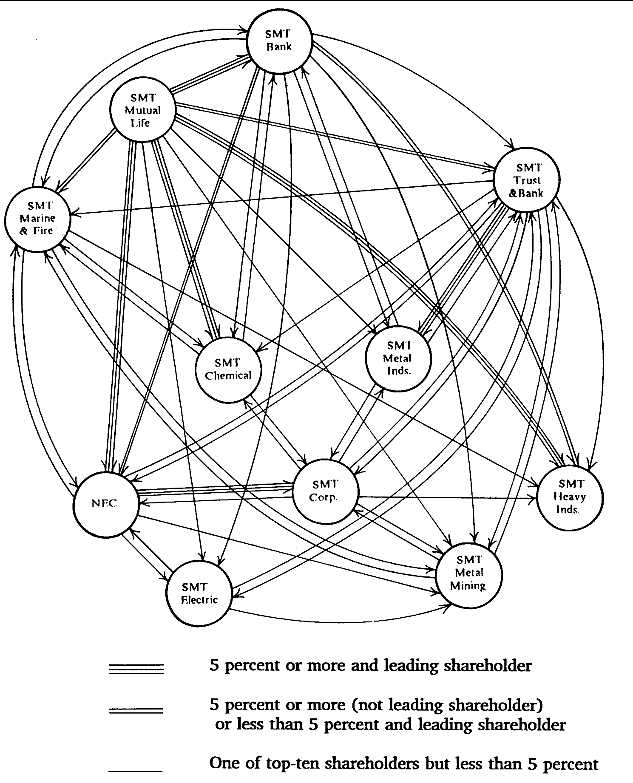

Fig. 4.3. Stuck Crossholdings of the Leading Companies in the Sumitomo Group

(Top-Ten Shareholdings Only). Source: Data from Industrial Groupings in Japan (1982). Note: SMT = Sumitomo.

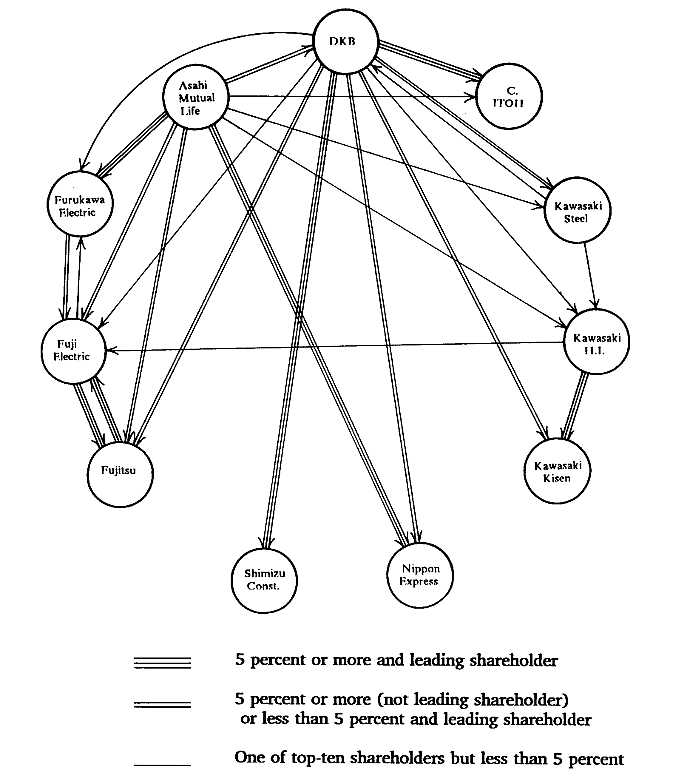

equity markets. Specific patterns of share crossholdings are shown in Figures 4.3 and 4.4 for the leading companies in the Sumitomo and Dai-Ichi Bank groups. The network of crossholdings among the eleven Sumitomo firms shown here is extremely dense, with 71 percent of the possible connections actually constituted.[12] At least four of the top-ten shareholders among each of these firms are other companies in the

Fig. 4.4. Stock Crossholdings of the Leading Companies in the Dai-Ichi Kangyo

Bank Group. Source: Data from Industrial Groupings in Japan (1982).

Note: DKB = Dai-Ichi Kangyo Bank; H.I. = Heavy Industries.

group. The pattern that emerges for the Dai-Ichi Kangyo group is substantially different. Historical connections across the group as a whole have been largely through a single firm, Dai-Ichi Kangyo Bank. The current group is the amalgamation of several smaller groups that had associations with the former Dai-Ichi and Nippon Kangyo banks. Asahi Mutual Life, Furukawa Electric, Fuji Electric, and Fujitsu were all part of the smaller prewar Furukawa zaibatsu and maintain within the larger Dai-Ichi Kangyo group a subset of close relationships, with five of the six

possible connections completed. Among the three firms associated with the Kawasaki zaibatsu-Kawasaki Steel, Kawasaki Heavy Industries, and Kawasaki Shipping-two of the three possible connections are completed. Overall density of the group is 40 percent.[13]

The leading eleven companies[14] within the other two zaibatsu groups, Mitsubishi and Mitsui, have densities of 69 percent and 58 percent, respectively, while the density in the Fuji group is 49 percent and that in Sanwa 45 percent. These findings conform to popular accounts of the cohesion of the various groups. Sumitomo is widely viewed to be, along with Mitsubishi, the most cohesive of the groups. Conversely, the three bank groups are all viewed as more loosely organized than their zaibatsu counterparts.

Table 4.2 shows the transaction matrix for shareholding among the financial and industrial firms in our sample in 1986. Internalization to own-group firms among companies' top-ten shareholders is over 25 percent for all six keiretsu and over 50 percent in the three zaibatsu groups. Shareholdings across keiretsu, in contrast, are generally small or nonexistent. Among shares issued by Sumitomo group companies, for example, less than 3 percent are held by Mitsui, Mitsubishi, Fuji, or Dai-Ichi Kangyo group firms. Equity control is, to a large extent, located among shareholders in the same group. Not surprisingly, preferential transaction ratios are also high. In total, companies in the six groups are 12.8 times more likely to have their shares held by other firms in the same group, a figure nearly as high as for bank borrowings.

It appears from these results that the keiretsu continue to be a major source of both debt and equity capital for their affiliated firms. As recently as 1986, these data demonstrate, shacho -kai member firms and particularly those in the ex-zaibatsu rarely cross boundaries to establish major equity or borrowing positions with firms in other groupings.

Continuity and Change in Japanese Corporate Finance

Over the past two decades, capital market liberalization in Japan has made available financial instruments not previously available to corporate borrowers. Firms are now free to raise investment funds through a variety of equity, bond, and hybrid mechanisms, and in both domestic and overseas markets. Many large Japanese companies have taken advantage of these opportunities, and the result has been a substantial decline in the proportion of external corporate capital coming from traditional sources such as long-term debt.

Observers now talk about the "dis-intermediation" of Japanese capi-

TABLE 4.2. TRANSACTION MATRIX FOR | ||||||

Affiliation of Company Issuing Shares | ||||||

Affiliation | Mitsui | Mitsubishi (15) | Sumitomo (13) | Fuji | Sanwa | Dai-Ichi Kangyo Bank (22) |

Mitsui (15) | 51.4 | 2.3 | 2.1 | 0.7 | 4.4 | 5.3 |

Mitsubishi (15) | 1.6 | 63.4 | 0.9 | 4.0 | 4.7 | 4.4 |

Sumitomo (13) | 1.6 | 2.2 | 63.9 | 3.7 | 3.9 | 2.8 |

Fuji (17) | 0.0 | 1.5 | 2.2 | 38.1 | 4.8 | 4.4 |

Sanwa (19) | 10.1 | 8.8 | 9.1 | 11.1 | 28.0 | 10.2 |

Dai-Ichi Kangyo Bank (22) | 1.3 | 3.1 | 0.9 | 10.4 | 12.8 | 31.6 |

Other Cos. (137) | 33.7 | 19.0 | 21.0 | 34.7 | 42.4 | 42.0 |

Total | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

SOURCE: See Appendix A. Note: Figures represent percentages among the top-ten shareholders only. Number of sample companies is given in parentheses. Owing to rounding, columns may not add up to 100%. | ||||||

tal markets with the rise of "direct" (securities-based) financing. More colloquially, the phrase ginko banare is sometimes heard, implying the weaning of companies from their banks. The assumption is that these changes represent the elimination of the traditional role of financial institutions as conduits through which capital flows from household savers to corporate borrowers and the rise of more marketlike patterns of corporate finance. Just how extensive are these changes? And to what extent do they represent fundamental and long-term shifts in the underlying character of relationships between financial and nonfinancial corporations in Japan?

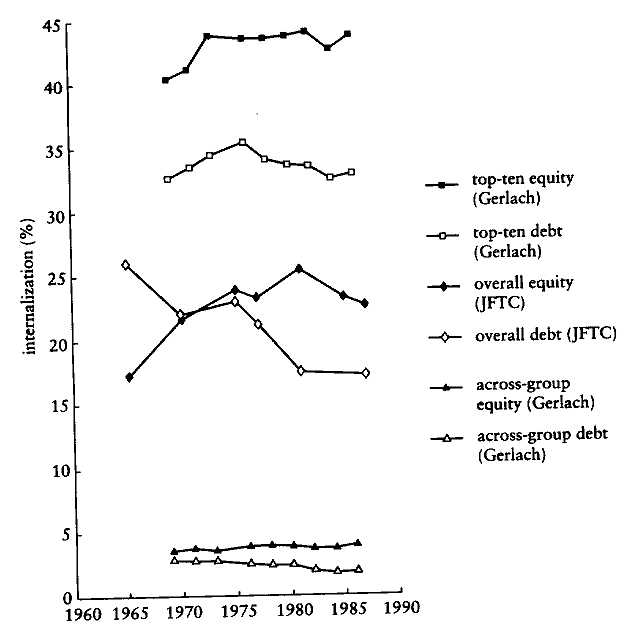

One way of measuring the effects of these changes is by looking at the relative share of external capital being provided by own-group financial institutions. Figure 4.5 shows time-lines for capital internalization among shacho -kai members based on data compiled by the Japan Federal Trade Commission and the data used in the present study. The JFTC studies have measured the extent of borrowing and shareholding since the late 1960s and show keiretsu relationships based on overall percentages of capital sourced within groups. The database used to compile the above figures is based on leading (top-ten) lenders and shareholders, and covers data from 1969 to 1986. Each of these sources, therefore, emphasizes somewhat different characteristics of the network. The JFTC data put financial sourcing in the context of firms' aggregate positions, and therefore include a large number of smaller lenders and shareholders. The database used for this study focuses only on major lending and shareholding positions (presumably those investors best able to form effective voting coalitions to influence corporate management) and has the advantage of including data on relationships across groupings.

Both measurement methods indicate that equity internalization is now substantially higher than debt internalization. The JFTC data report that this is part of a trend dating back at least to the mid-1960s. Since that time, firms have borrowed a declining share of their capital from financial institutions in their own group but relied on firms in their own group for an increasing proportion of equity capital. The two curves appear to have crossed sometime around 1970, the period at which our own sample data begin. The much higher internalization figures for both debt and equity in our sample when compared with the JFTC results reinforce the point that affiliated firms constitute a disproportionate share of leading capital positions. The percentages found in this sample also do not show a significant decline when compared with the 1970 period, nor do they indicate any increase in across-group

Fig. 4.5. Internalization of Debt and Equity over Time. Sources: Kosei Torihiki Iinkai survey data (various years);

for information on other data, see Appendix A. Note: Across-group figures are taken as a weighted average.

holdings during this period. Although the JFTC data suggest some decline in equity internalization since the early 1980s, the figures for 1988 are still higher than those fifteen years earlier.

These findings indicate that keiretsu affiliates continue to be an important source of external capital for Japanese firms. They also suggest that financial liberalization in Japan has not had the effect of increasing the proportion of external capital coming from financial institutions affiliated with other groups. What, then, is one to make of the changes occurring in Japan's financial structure?

The widespread view that Japanese corporate finance has moved from "indirect" to "direct" financing is based on the traditional perspective within financial economics that household savers channel capital to

corporations either directly, by entering the stock or bond market, or indirectly, by depositing it in banks that lend to companies. The reality in contemporary Japan is that even securities markets are mediated by large institutions linked through a complex set of strategic relationships with corporate users of capital. An actual revolution from indirect financing to direct financing would involve the discontinuation of the historically configured flow of money through indirect financing that tightly links corporations and financial institutions, and the advent of direct supply of savings (personal capital) to industry without passing through financial institutions.

That this has not been the case is evident in analyzing the actual pattern of the flow of funds rather than the mechanisms through which those funds travel. The ratio of individual shareholding in Japan has continued to decline and less than one-quarter of all shares in Japan are now held by individuals. Banks and insurance companies, in contrast, have continued to be net purchasers of securities (buying about 18 trillion shares and 16 trillion shares during the 1980s, respectively) and together now control nearly one-half of all publicly traded shares in Japan.[15] For this reason, when we examine the flow of capital through the Japanese economy, the vast majority continues to be mediated by financial institutions, as shown in Table 4.3. Although securities-based financing accounted for 44.2 percent of the total flow of funds through the corporate sector in 1987, all but a small fraction of this passed through financial institutions rather than being channeled directly from household savers or investment trusts into stocks and bonds. Together with credit-based financing that accounts for most of the remaining flow of funds, over 90 percent of total capital flows continue to be mediated by financial institutions into the late 1980s.

This gradual change in financing methods might have great significance if these financial institutions as purchasers of securities behaved quite differently than they do as financial lenders-for example, by becoming unstable stock market investors rather than stable lead banks. However, as empirical results in Chapter 3 demonstrated, equity ties among financial and nonfinancial companies continue to be structured in long-term relationships that reflect a complex set of strategic interests among the parties involved. These, therefore, continue to be administered rather than impersonal market transactions. Further indicating the continued role of keiretsu capital is the finding, reported in Figure 4.5, that the internalization of equity capital within the same group is now actually higher than for bank capital. Shifts toward equity capital

TABLE 4.3. "INDIRECT" FINANCING | |||

Flow of Funds | |||

"Indirect" Financing | |||

Year | Total | Securities | "Direct" |

1975 | 93.1% | 22.3% | 7.1% |

1980 | 86.1% | 25.9% | 8.5% |

1985 | 87.0% | 29.0% | 6.5% |

1987 | 90.7% | 37.5% | 6.7% |

SOURCE : Securities Market in Japan 1990, p. 3. Notes: "Indirect" financing refers to funds raised through financial institutions. "Direct" financing refers to funds raised through non-mediated securities investments, including those raised through invest-merit trusts. Foreign capital markets account for the remaining flow of funds in each year. These figures were -0.2% in 1975, 5.4% in 1980, 6.5% in 1985, and 2.6% in 1987. | |||

would therefore seem actually to be working toward one of the strengths of the intermarket groups.

This is not to say that the shift in the nature of capital financing is unimportant. With the decreasing proportion of total capital allocation channeled through the traditional prime rate system, the Ministry of Finance and the Bank of Japan are no longer able to exercise the same degree of control over financial markets that they once could. It is also true that, with the new reliance on securities-based finance, Japan's major securities companies are now more important in financial markets than in the past. Furthermore, even as banks and other financial institutions account for an increasing share of securities-based capital, the ability of highly profitable industrial firms to fund their investments through retained earnings has reduced their overall external capital dependency and shifted the balance of bargaining power with lending firms in their direction.

However, the overall effects of these changes on the internal cohesion of Japan's intermarket groups are not nearly as dramatic as they might at first appear. Even as they retire their own debt, large firms continue to rely on banks to provide loans for their affiliates. For example, Mit-

subishi Motors, which was spun off from Mitsubishi Heavy Industries in 1970 with the equity participation of Chrysler Motors, continues twenty years later to use the same financial institutions as its parent company. Among the top-ten lenders to Mitsubishi Heavy Industries, eight are also among Mitsubishi Motors' top-ten lenders, and both firms use the same main bank, Mitsubishi. Even for smaller companies, parent companies serve as an important source of bank capital by introducing and guaranteeing their bank borrowings. In an analysis of satellite firms affiliated with major electronics producers, for example, I found that 68 percent used the same main bank as their parent company (Gerlach, 1992b).

Japanese securities companies are themselves linked through long-term relationships with their industrial clients. Although not generally as closely identified with well-defined keiretsu as the city banks or as widely recognized, these affiliations are not unimportant. Among the Sumitomo group's twenty core companies, for example, all but four rely on Daiwa Securities as their lead underwriter as of 1989, and all but one of these companies has done so for the past two decades. Daiwa Securities is linked in turn into the Sumitomo group by virtue of the fact that its two leading shareholders and reference banks are Sumitomo Bank and Sumitomo Trust and Banking.[16]

In addition, the "securitization" of Japanese capital markets has actually been in the interests of Japan's commercial banks in at least one important respect. Since the mid-1980s, Japanese banks have been under new regulatory pressures, especially in order to meet BIS requirements for minimum capital ratios.[17] These requirements have forced the banks to raise new equity capital, and they have been among the most active participants in stock issues. During the six years from 1984 to 1990, Japan's twenty-three largest banks raised ¥13.5 trillion in equity capital, an amount that represented a substantial fraction of all new equity capital raised in Japan during this period (Wall Street Journal, March 18, 1991).[18] Moreover, the basic pattern of interlocking shareholding has continued, with nonfinancial firms utilizing approximately 30-40 percent of their own new capital to purchase bank equity issues and maintain their stable crossholdings (Nihon keizai shinbun, October 24, 1989). In this way, the demands for equity-based financing have served both nonfinancial and financial interests while limiting disruption to traditional ownership relationships.

In short, because of their central role as providers of both loan-based and securities-based capital, Japanese banks remain the main source of external capital for most major Japanese corporations. Even those firms

that have retired their debt and rely heavily on internal profits to fund investment activities continue to have these financial institutions as leading shareholders, granting them the attendant rights to vote shares and monitor management. Moreover, insofar as debt continues to be channeled to the affiliates of these corporations, the total dependency of vertical keiretsu chains of suppliers and distributors on these banks in most cases is still very high. Indeed, Japan's banks actually increased their loans in the 1980s at a rate that was higher than the growth rate of the economy as a whole, and by the end of the 1980s, most of the world's largest banks were Japanese.[19] This suggests a different interpretation of the changing nature of the keiretsu: what may be happening is not a breaking down of bank-led groupings so much as an expansion of these groupings across a broader spectrum of Japanese industry; their increasing organization within elaborate hierarchical structures around local centers of power (the parent companies); and their linking through securities-related instruments of finance and control.

THE FLOW OF DIRECTORS

Among the most studied areas of interorganizational relationships in the United States has been that of interlocking directorates-connections among firms in business networks through the sharing of executive position holders. Applying this same approach in order to induce alliance structures in Japan presents a number of interesting and different features that shed light on the nature of corporate control over the Japanese firm and the ways in which it is embedded in interfirm networks. These features may be summarized as follows: First, directorships in Japan are associated with a broader system of interfirm personnel flows known as shukko , or employee transfers. Instead of serving as part-time directors, executives moving from one firm to another typically take up full-time positions in the recipient firm. The pattern of movement of personnel between firms indicates that the dispatching process serves to reinforce specific relationships between firms rather than the more general interests the firm might have in monitoring its environment. Second, the dispatching of directors most often expresses a vertical relationship, with the flow of directors moving unidirectionally from one organization to another. Three vertical relationships predominate: government-company, parent company-satellite, and bank-client. Third, as a result of the first two features, outside directorships among

keiretsu firms are limited largely to other group firms, but the overall intragroup network is sparse in comparison to what we might expect from the dense patterns of equity crossholdings.

Interfirm Personnel Connections in Japan: Outside Directorships versus Employee Transfers

In the prewar zaibatsu, an important source of control by the honsha over its subsidiaries was through directors sent out to those firms. By 1945 Mitsui honsha held twenty-one directorships in its subsidiaries, Sumitomo fifty-one, and Mitsubishi eighty-five, or an average of about two to four directors per first-line subsidiary (Miyazaki, 1976). With the postwar democratization of large-scale enterprise in Japan came the belief that boards should represent interests other than those of capital and, in particular, of the families that controlled and benefited from the zaibatsu. Changes in the Commercial Code in 1950 allowed nonshareholders to become directors, and this has evolved into a system whereby directors are full-time executives of the firm with interests like those of management rather than those of representatives of external shareholders. Clark (1979) notes in his case study of a Japanese firm that

the board has much more the look of a senior management meeting than of the convocation of the representatives of the shareholders. Most of the directors have responsibility for running part of the company, and are not in an ideal position objectively to review the performance of a management which includes themselves and their senior and junior colleagues. . .. Becoming a director, therefore, was a precondition of future progress in the standard ranks, rather than the acquisition of a new role, entirely different from that of an employee. [Pp. 100, 108.]

Over 90 percent of the boards of large Japanese firms are now composed of full-time managers (Ballon et al., 1976; Bacon and Brown, 1978) and better than two-fifths of all firms have no outside directors. The result is a system in which the board of directors takes on largely ceremonial functions (see Chapter 7) instead of serving as a forum for the representation of owner interests.[20] The following comment by one board member was typical: "Not that much is discussed at the board meeting. It is after the meeting that we talk about various things."

But the predominance of full-time managers as directors is also significant because not all of them began their careers in the same company. A large portion have moved from one firm to another by mutual agree-

ment. Inohara (1972, p. 5) reports that an average of more than three hundred employees in each of the three large companies he studied (all had more than five thousand employees) had been sent to other firms. Most involved younger employees and were only temporary transfers. These typically lasted for two years, during which the dispatching firm guaranteed the employee's salary. But a smaller fraction of the total were employees in their early fifties who were unlikely to be promoted to the director level in their own firm before retirement. When upper-level executives are dispatched to other firms, it is usually on a permanent basis with the employee taking on an executive position in his new firm. Where these employees become officers or directors of the recipient firm, they are known as haken yakuin, or dispatched directors. As a result of transfers, about one-third of the directors of Japan's major corporations now come in from the outside, compared to the United States where outside directors constitute over two-thirds of the total.[21]

The distinctive feature of this form of directorship is that, in contrast to the U.S. model in which the director is truly "outside"-that is, the directorship is a part-time position and connections to another organization are maintained-the dispatched director in Japan becomes a full-time employee in the receiving firm. These generally represent longstanding and multistranded interorganizational linkages and serve the interests of management in two firms at once as part of an ongoing relationship between the firms. Nearly all dispatching firms-86 percent in one study (Kosei Torihiki Iinkai, 1983b)-are simultaneously among the recipient firm's top-ten shareholders. This relationship is further supported by the efforts dispatching firms make to maintain connections with their transfers. Inohara (1972, p. 18) reports that one company maintained a special consultation room open to transferees in its own office, continued to invite them to the company's "friendship organization" (koyo-kai ) and other activities, and sent them regular information about the company, as well as congratulatory and condolence messages.

Dispatched Directorships as an Expression of Vertical Interfirm Relationships

In addition to reinforcing ongoing relationships among firms, the dispatched directorship system in Japan is also distinctive in the predominant type of relationship which it expresses. This is a vertical one between two asymmetrically positioned firms, typically between one of

three sets of organizations: government-corporation, parent company-satellite, and bank-client. This contrasts sharply with the image in the United States of interlocks across horizontally positioned firms for the purposes of diffusing information or reinforcing broader community- or class-wide interests (Useem, 1984).

According to figures provided in Industrial Groupings in Japan (1982, p. 23), of the 2,980 outside directors moving to a firm that is listed on the Tokyo Stock Exchange, 30 percent came from government, 35 percent came from manufacturing concerns and from trading companies, and 35 percent came from banks. Outside directors coming from government are generally from one of the government ministries and organizations most closely associated with a firm's own business-the Ministry of International Trade and Industry (MITI) for manufacturing concerns, the Ministry of Finance (MoF), the Bank of Japan for financial institutions, and so on. The process of moving from government agency to corporate position is referred to as "descending from heaven" (amakudari ). These officials are required to retire formally from their government position, then spend a two-year grace period before being adopted into their new position. Informal connections with their old organization, of course, typically remain.

Directorship connections between firms are most likely to involve parent companies and their satellites and banks and their clients. Within the large vertical keiretsu, representative directors are usually dispatched from the parent manufacturer to its subcontractors. Toyota Motors, for example, sends an average of three to six representative directors to each of its first-line satellites, as do Nissan, Hitachi, Matsushita, and other large parent industrial concerns (from data in Industrial Groupings in Japan, 1982). Banks are less likely to send more than one director to a company, unless the company is undergoing restructuring with bank assistance. They do, however, send directors to a wide range of companies and are the firms most likely to dispatch directors to large companies. Nearly half of all outside directors among these companies come from their group bank (Kosei Torihiki Iinkai, 1983 b, p. 12). As a result of the vertical relationship implied in these directorship interlocks, it is the largest firms in the Japanese economy that are overall most likely to be the dispatchers. The Oriental Economist (December, 1982) found that the 182 shacho -kai member companies at the time sent over one-half of the dispatched directors among the 1,600 firms listed on the Tokyo Stock Exchange.

The Keiretsu and Directorship Networks

The distinctive features of directorship connections outlined above have resulted in group directorship networks with two main structural features. First, the fact that directors typically become full-time employees in the recipient firm and reinforce ongoing relationships between firms rather than more general interests in the wider business community has made the identity of sender and receiver a particularly critical issue. Since ongoing relationships are more likely to be with other firms in the same group, outside directorship connections are heavily internalized and there is a strong bias toward one's own group. At the same time, the hierarchical relationship implied by directorship connections in Japan has resulted in relatively few directorship connections among large firms in favor of connections vertically from larger to smaller firms. Within the intermarket groups, which are composed almost entirely of larger firms, this has meant sparse patterns of connections in comparison with the dense patterns found in equity interlocks.[22]

One source, Nihon kigyo shudan bunseki (1977, vol. 1, pp. 124-26), provides a detailed list of outside directorships for the extended Sumitomo group that indicates both original positions of directors and their positions in the recipient firm. An analysis of these directorships indicates that of the total of 160 directorships among Sumitomo companies, 122, or 76 percent, were dispatched from a shacho -kai member firm to a satellite firm in the group-sometimes in the position of president or chairman of the satellite-while only 38, or 24 percent, moved from one shacho -kai member to another.[23] Specific patterns of interlocks are shown for the Sumitomo and Dai-Ichi Kangyo groups, in Figures 4.6 and 4.7. Intragroup networks in the Sumitomo group are particularly sparse, while linkages within the Dai-Ichi Kangyo group are primarily through the bank.

Although directorship interlocks are infrequent among large firms, Table 4.4 makes evident that, when outside directors are brought in, they are most likely to come from another firm in the same group. Altogether, over one-half of outside directors come in from other companies in the firm's own group. Of the remainder, nearly all are amakudari directors from government. In only five cases overall, and only one among the three zaibatsu groups, do outside directors come from a company in another group. For this reason, the preferential transaction ratio is very high, averaging 21.9 times among those firms that have outside directors. In short, outside directorships are infrequent among the largest

Fig. 4.6. Dispatched Directors of the Leading Companies in the Sumitomo Group.

Source: Data from Industrial Groupings in Japan (1982). Note: SMT = Sumitomo.

firms, but where they exist they are most likely to involve other firms in the same group.

INTERMEDIATE PRODUCT MARKETS

No doubt the most controversial issue in understanding the role of keiretsu organization in the Japanese economy is its impact on product market trade. Given the strong preferential patterns demonstrated ear-

Fig. 4.7. Dispatched Directors of the Leading Companies in the Dai-Ichi Kangyo Bank Group.

Source: Data from Industrial Groupings in Japan (1982).

Note: DKB = Dai-Ichi Kangyo Bank; H.I. = Heavy Industries.

lier in networks of borrowed capital, corporate ownership, and directorships, it should not be surprising if the keiretsu are also involved in structuring linkages within intermediate product markets. As we see below, however, internalization tends to be lower in product trade than in other relationships and varies substantially according to the type of company involved. Nevertheless, the overall pattern is clearly not one of trading neutrality. In this section, we consider the extent of keiretsu structuring of product trade through direct purchases and sales (e.g., a

TABLE 4.4. TRANSACTION MATRIX FOR DISPATCHED DIRECTORS, 1980 | ||||||

Affiliation of Company Receiving Director(s) | ||||||

Affiliation | Mitsui | Mitsubishi (15) | Sumitomo | Fuji | Samoa | Dai-Ichi Kangyo Bank (16) |

Mitsui (15) | 48.0 | 0.0 | 0.0 | 7.7 | 0.0 | 0.0 |

Mitsubishi (15) | 0.0 | 60.4 | 0.0 | 0.0 | 0.0 | 3.6 |

Sumitomo (13) | 0.0 | 6.7 | 67.1 | 2.6 | 0.0 | 0.0 |

Fuji (17) | 0.0 | 0.0 | 0.0 | 25.9 | 0.0 | 0.0 |

Sanwa (19) | 0.0 | 0.0 | 0.0 | 7.7 | 36.2 | 0.8 |

Dai-Ichi Kangyo Bank (22) | 0.0 | 2.2 | 0.0 | 4.1 | 23.6 | 38.7 |

Other Cos. (137) | 52.0 | 30.7 | 11.5 | 46.4 | 40.3 | 53.7 |

Govt. Orgns. | 0.0 | 0.0 | 21.4 | 6.1 | 0.0 | 1.0 |

Total | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

SOURCE : See Appendix A. Note: Number of sample companies is given in parentheses. Owing m rounding, columns may not add up m 100%. | ||||||

steel company's purchase of a mining company's coal), and in the next section we expand the analysis to include collaborative group projects among affiliated companies.[24]

The main actor in the organization of product market relationships of both kinds has been the group trading companies. The sogo shosha are to the keiretsu trading network what banks are to its capital networks- the most centrally positioned firms, with direct linkages to most other companies in the group. For the majority of intermediate product manufacturers in a keiretsu, they are the leading overall supplier and customer. Moreover, they are important as an organizer of small- and large-scale group projects.

The sogo shosha have been critical in the historical development of the Japanese economy. By 1900 Mitsui Bussan alone handled about one-third of Japan's foreign trade. As was the case with banks, the emergence of trading companies was closely tied to that of the zaibatsu themselves:

The general trading companies developed best when they were part of a zaibatsu. Those that were started independently of the zaibatsu either did not succeed or remained small. The zaibatsu was a system that provided them with ample capital and security as well as with room for initiative. And the name of the zaibatsu assured them also of qualified personnel because of the prestige and power the zaibatsu name involved. [Hirschmeier and Yui, 1975, p. 192.]